- Report Index

- Did Japan’s Corporate Governance Reform Work?

- Illuminating Tomorrow

-

2026.02

Did Japan’s Corporate Governance Reform Work?

- Evidence from Firms Appointing a Majority of Independent Outside Directors -

Yoshio Kawatani

- Executive Summary

-

- This report aims to quantitatively examine how Japan’s corporate governance reforms, implemented since 2015, have affected corporate profitability as measured by Return on Equity (ROE). While empirical studies on the effectiveness of these reforms remain limited, this report reassesses their substantive impact and outlines expectations for future governance reforms.

- Using a broad event-study framework, the analysis defines the event as the appointment of independent outside directors to a majority of the board. Rather than focusing on the formally required threshold of “at least one-third independent outside directors,” which carries a strong compliance-driven aspect, the analysis concentrates on majority appointments that better reflect firms’ autonomous governance decisions. The sample consists of 54 firms that remained listed between fiscal years 2015 and 2024, experienced the event during this period, have available data for three years before and after the event, and had room for ROE improvement.

- Comparing average ROE for the three-year pre-event and post-event periods, the analysis confirms a statistically significant increase in ROE following the event. This suggests that, for firms with potential for improvement, appointing a majority of independent outside directors is associated with enhanced profitability.

- A DuPont decomposition reveals that the improvement in ROE is driven by increases in profit margins and total asset turnover. Both mean-difference tests and multiple regression analysis confirm these effects, while no significant contribution from financial leverage is observed.

- These findings suggest that governance reforms contributed to improved profitability not through increased leverage or temporary shareholder payouts, but through substantive managerial decisions such as pricing strategies, cost structures, business portfolio restructuring, and more efficient asset utilization. The results also provide partial counterevidence to critiques that increased board independence necessarily promotes short-termism.

- That said, the analysis does not imply that appointing independent outside directors automatically guarantees governance reform outcomes. The effectiveness of such reforms depends on the appropriate selection and active utilization of independent directors. As discussions on revisions to the Corporate Governance Code and the Companies Act progress, it is hoped that further accumulation of empirical evidence will support governance reforms that are truly effective rather than merely formal.

1. Introduction: Purpose and Motivation

This report aims to quantitatively assess the impact of Japan’s corporate governance reforms—initiated during the Abe administration and symbolized by the introduction of the Corporate Governance Code in 2015—on corporate profitability.

Evaluating the quantitative effects of corporate governance reform has long been a challenge in Japan. While a number of prior studies exist, materials presented by the Financial Services Agency at the “27th Follow-up Council on the Stewardship Code and Corporate Governance Code” in May 2022 noted that empirical studies focusing on the post-reform period remain limited and that their findings are mixed. Subsequent research continues (Note 1), but the prevailing view is that although ROE and ROA have improved since 2013, this improvement has been driven primarily by higher profit margins rather than expanded capital investment or M&A activity. Within the scope of this study, no clear evidence is found that corporate governance reforms have directly promoted growth-oriented investment, and the current consensus is that the increased profits have been allocated mainly to debt reduction, internal reserves, and shareholder returns. Clear evidence that governance reforms directly stimulated growth investment remains scarce.

Although the Corporate Governance Code was revised twice at three-year intervals between 2015 and 2021, criticism persisted that reforms driven by the Code were overly formalistic. In response, policy attention gradually shifted toward enhancing the substance of corporate governance, culminating in the publication of an Action Program aimed at promoting more effective governance practices in April 2023.

Since the 2021 revision, no further amendments to the Corporate Governance Code have been implemented. However, growing concerns have recently emerged that corporate investment has remained subdued and that firms may be accumulating excessive cash and cash equivalents. Against this backdrop, discussions are underway regarding potential revisions to the Code that would require firms to more clearly assess, explain, and justify their capital allocation decisions. Further revisions to the Code are therefore expected in the first half of 2026, making a reassessment of the quantitative effects of past reforms both timely and meaningful.The remainder of this report is structured as follows. Section 2 explains the analytical methodology. Sections 3 and 4 present the results. Section 5 outlines implications, and Section 6 concludes with remaining challenges and expectations for future governance reforms (Note 2).

2. Methodology

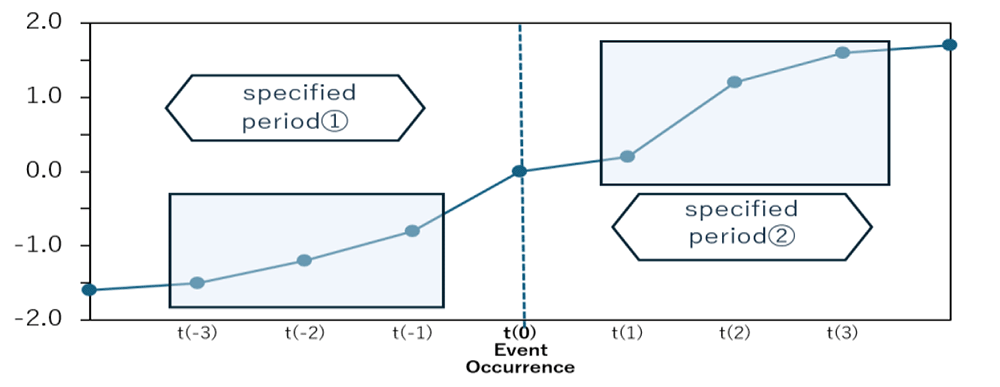

This report employs a broad event-study framework (Note 3) that examines changes in corporate performance indicators in the pre-event and post-event periods of a defined institutional or managerial event. As illustrated in Figure 1, the analysis measures whether statistically significant changes occur between two specified periods surrounding the event.

Figure 1 Conceptual Framework of the Analysis (Broad Event-Study Framework)

(Source) Dai-ichi Life Research Institute

For the performance metric, this study uses each firm’s ROE for every fiscal year (Note 4). The event is defined as the point at which independent outside directors account for a majority of the board, and the event year is identified as the fiscal year in which this condition is first met.

ROE is adopted as the performance indicator because it is widely regarded as an important metric by both corporations and investors, and it is also emphasized in initiatives by the Tokyo Stock Exchange (Note 5).

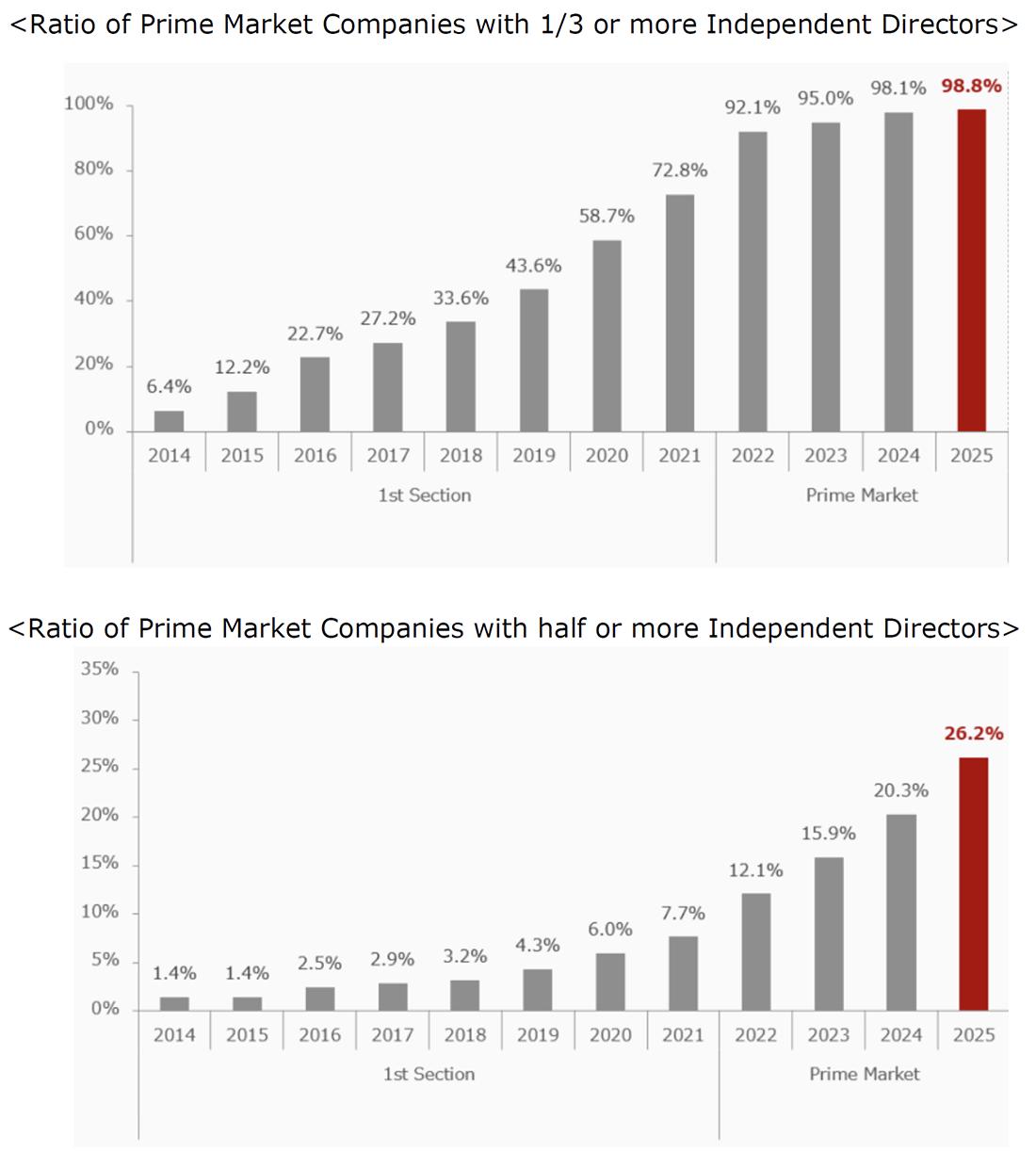

As for the event definition, the analysis focuses on the proportion of outside directors appointed by firms. This is because the effective use of independent outside directors has been one of the central pillars of Japan’s corporate governance reforms, and, as shown in Figure 2, the share of such directors has increased markedly among Prime Market firms since 2015. For this reason, the increase in the proportion of independent outside directors can be regarded as a symbolic development of the corporate governance reform.

Figure 2

(Source) Extract from Tokyo Stock Exchange disclosure materials

Rather than using the one-third threshold—now met by nearly all Prime Market firms and explicitly required by the Corporate Governance Code (Note 6)—the majority threshold is considered more suitable, as it reflects firms’ autonomous governance decisions and remains less prevalent.

The population from which such firms were screened consists of companies that remained continuously listed on the Prime Market (formerly the First Section of the Tokyo Stock Exchange) from fiscal year 2015 through fiscal year 2024.

In this analysis, the measurement window is defined as the three-year pre-event period and the three-year post-event period following the event. For each firm, the average ROE over the three years prior to the event and the average ROE over the three years after the event are calculated. A statistical test is then conducted to determine whether there is a significant change in the three-year average ROE between the pre-event and post-event periods—that is, whether an increase in ROE can be statistically confirmed.

When a statistically significant improvement in ROE is observed, a DuPont decomposition (Note 7) is applied to examine through which structural channels ROE increased. Specifically, the analysis decomposes ROE into its constituent components—profit margin, total asset turnover, and financial leverage—and evaluates changes in each component using both mean-difference tests comparing pre- and post-event three-year averages and multiple regression analysis.

All data required for this analysis—including each firm’s proportion of independent outside directors, ROE, and the financial variables necessary for the DuPont decomposition (sales, total assets, and shareholders’ equity)—are obtained from Bloomberg.

In conducting the analysis, it is assumed that firms with relatively high ROE prior to the event are less likely to place managerial emphasis on further ROE improvement and, consequently, less likely to experience subsequent increases in ROE. Accordingly, the statistical analysis is restricted ex ante to firms whose average ROE over the three-year pre-event period was below 15 percent, a threshold intended to capture firms with substantial potential for ROE improvement. As a result of this screening, the final sample used for effect verification is reduced to 54 firms.

While the number of firms that have appointed a majority of independent outside directors is currently estimated to be around 400, the initial pool of firms that remained continuously listed between fiscal years 2015 and 2024 and for which the necessary data were available comprised 1,593 firms. Further restricting the sample to firms for which the event occurred within the observation period and for which a full seven-year dataset—covering three years before the event, the event year, and three years after the event—could be obtained resulted in the final analytical sample.

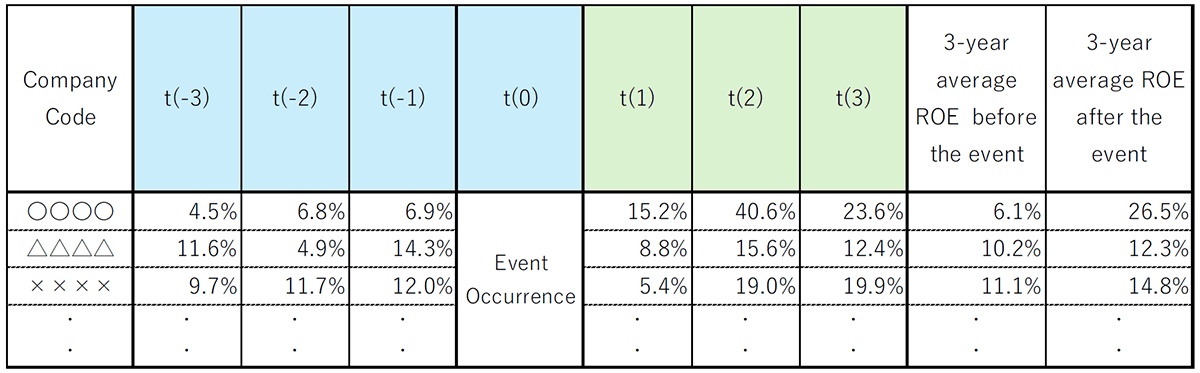

For reference, Figure 3 presents a portion of the dataset constructed for this analysis, illustrating the structure of the data sheet used, including ROE values (Note 8).

Figure 3 Part of the datasheet used for this analysis (regarding ROE)

(Source) Compiled by Dai-ichi Life Research Institute

3. Did ROE Improve After the Event?

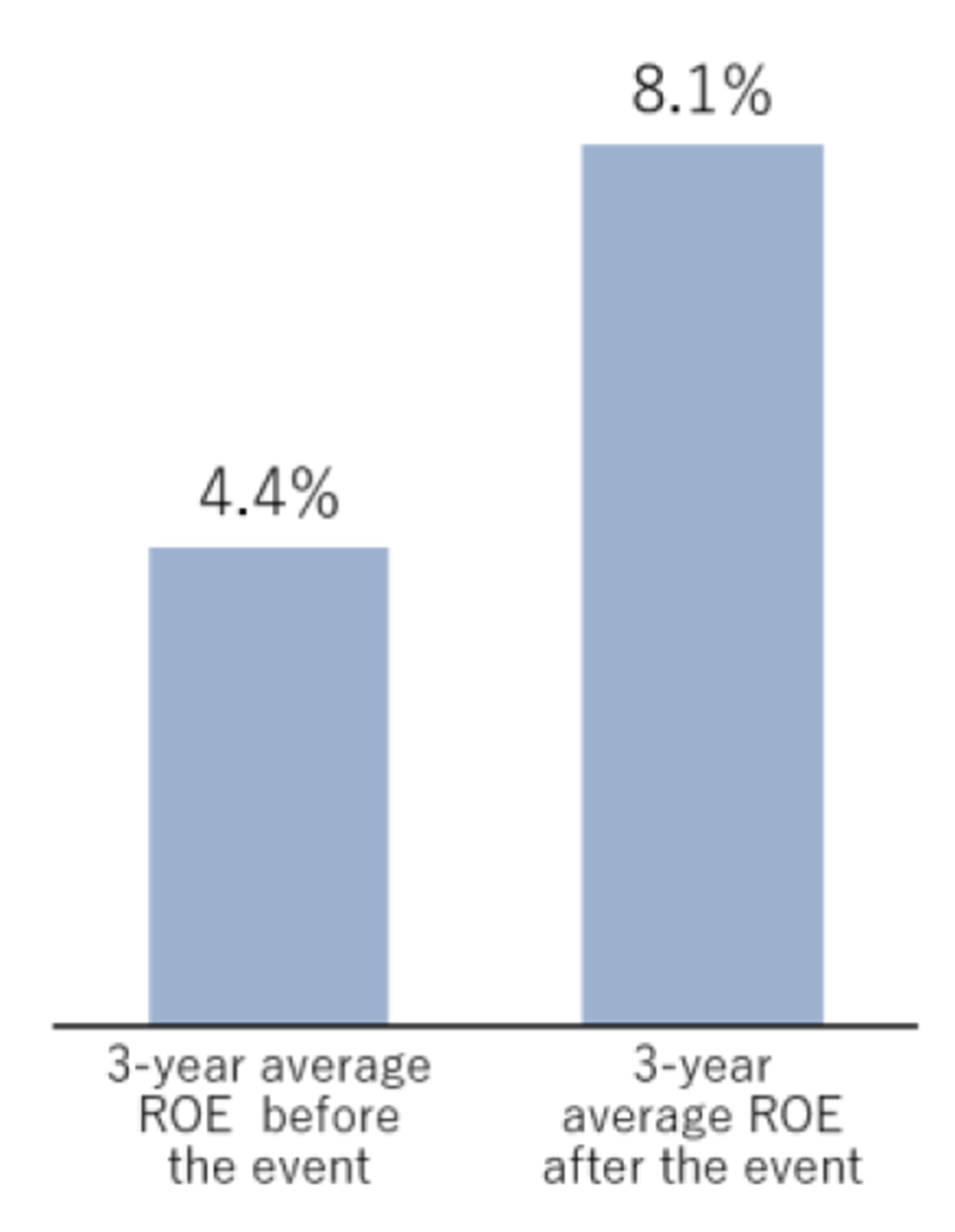

For the 54 firms in the sample, average ROE over the pre-event and post-event three-year periods was compared. While the graph presented in Figure 4 visually suggests that ROE tends to increase following the occurrence of the event, a visual inspection alone is not sufficient to determine whether this difference is statistically meaningful.

Figure 4 Change in the three-year average ROE between the pre-event and post-event periods

(Source) Compiled by Dai-ichi Life Research Institute based on Bloomberg data

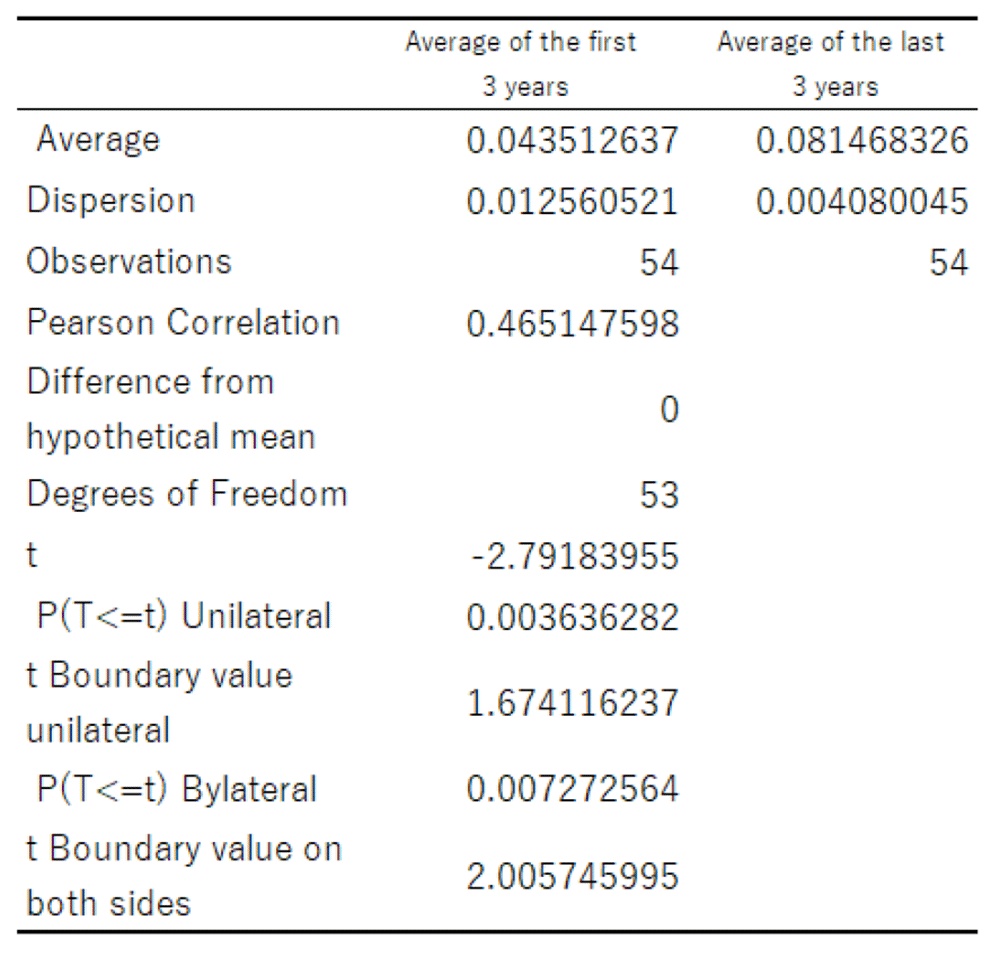

Accordingly, a t-test (Note 9) was conducted to statistically examine whether the difference between the pre-event and post-event three-year average ROE is significant. The results of this test are reported in Figure 5.

Figure 5 T-test results for the difference between pre-event and post-event three-year average ROE for 54 companies

(Source) Compiled by Dai-ichi Life Research Institute based on Bloomberg data

The results of the t-test indicate that the one-sided p-value is 0.003636, confirming that the difference between the pre-event and post-event three-year average ROE is statistically significant at the 1 percent level. In other words, for firms that were considered to have room for improvement in profitability and that experienced the event of appointing a majority of independent outside directors, the three-year average ROE after the event is statistically higher than the three-year average ROE before the event.

This finding implies that, among firms with room for ROE improvement, the appointment of a majority of independent outside directors is associated with a subsequent increase in ROE. That is, for firms in which the event of majority-independent board composition occurred, a tendency toward higher ROE in the post-event period can be statistically confirmed (Note 11).

4. Through Which Channels Did ROE Improve? - DuPont Decomposition Analysis

In this chapter, in order to examine through which mechanisms the increase in ROE identified in the previous chapter occurred, ROE is decomposed using the DuPont framework into its constituent components—profit margin, total asset turnover, and financial leverage—and each component is analyzed in turn.

(1) Mean-Difference Tests

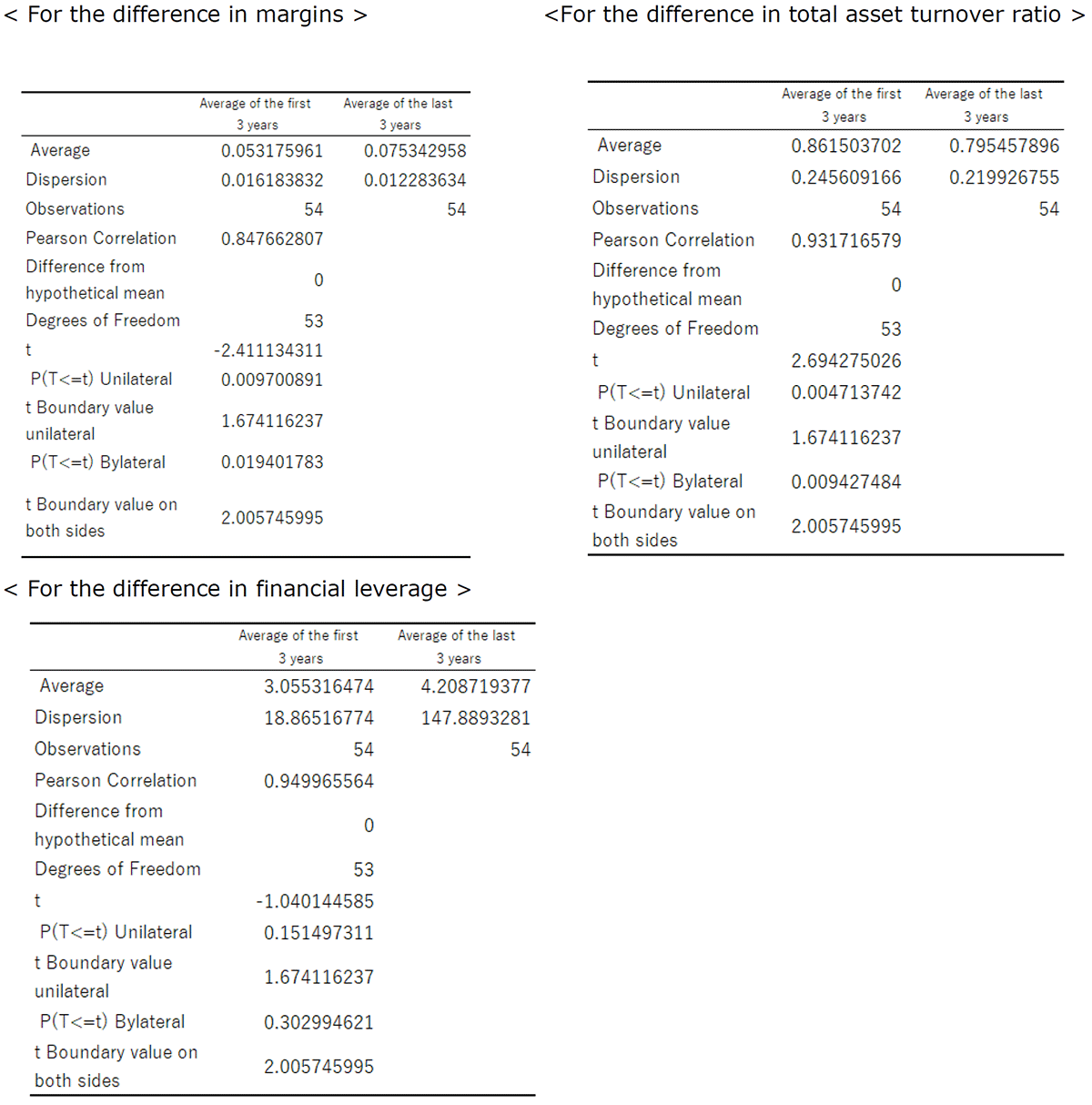

For each of the 54 firms in the sample, annual data on sales, total assets, and shareholders’ equity (net assets) were collected for each fiscal year from 2015 through 2024. Based on these data, the values of profit margin, total asset turnover, and financial leverage were calculated for each year in the three-year pre-event period and post-event period, and a data sheet analogous to that shown in Figure 3 was constructed.

As with ROE, t-tests were then conducted to examine whether statistically significant differences exist between the pre-event and post-event periods for each of these components. The results of these tests are presented in Figure 6.

Figure 6 T-test results for the difference between three-year average margin, total asset turnover, and financial leverage pre-event and post-event periods for 54 companies

(Source) Compiled by Dai-ichi Life Research Institute based on Bloomberg data

Based on the magnitude of the one-sided p-values reported in Figure 6, and focusing on within-firm differences in three-year average values before and after the event, statistically significant improvements at the 1 percent level are observed for both profit margins and total asset turnover in the post-event period. In contrast, no statistically significant change is detected for financial leverage.

(2) Multiple Regression Analysis

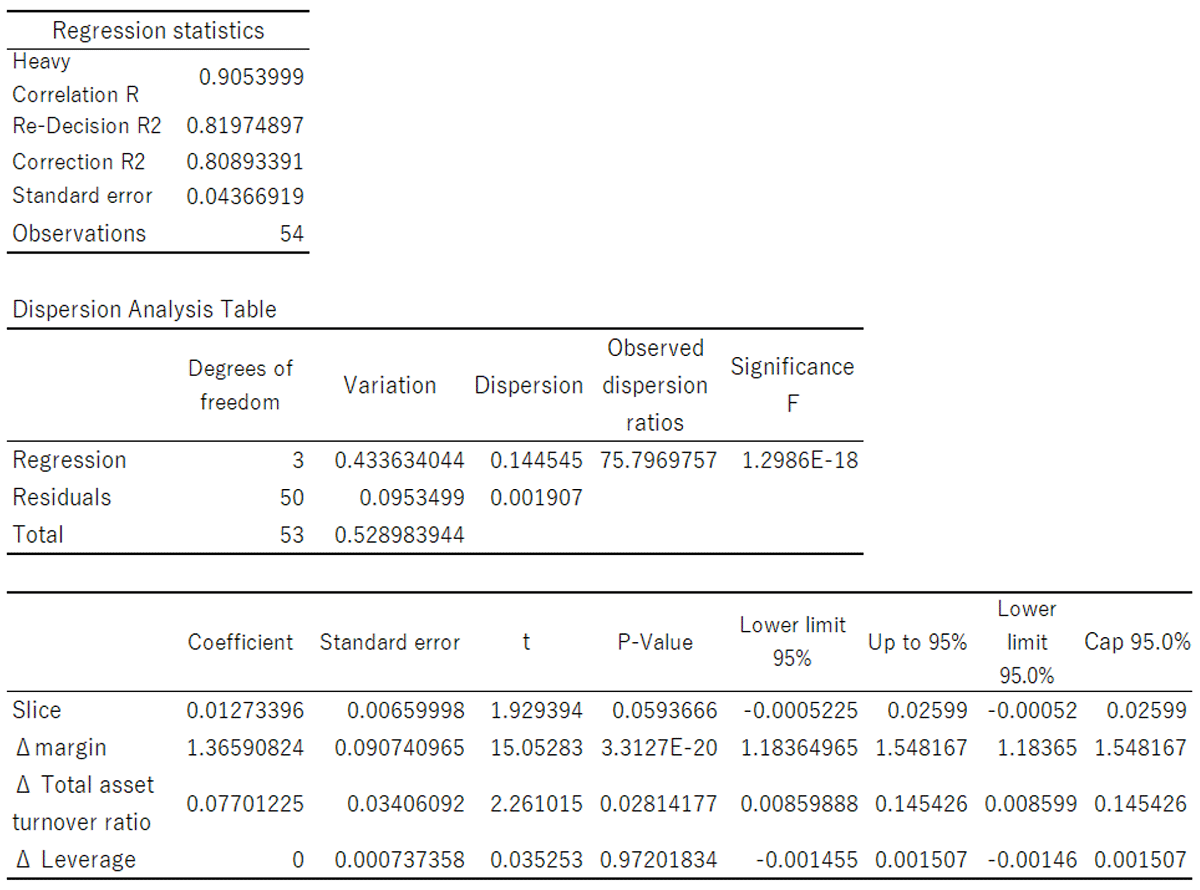

Building on the statistically significant changes in three-year average profit margins and total asset turnover identified in the previous subsection, a multiple regression analysis (Note 12) is conducted. In this analysis, the dependent variable is defined as the difference between the post-event and pre-event three-year average ROE for the 54 firms in the sample. The explanatory variables are defined as the corresponding differences in the three-year average values of profit margin, total asset turnover, and financial leverage for the same firms.

The results of this multiple regression analysis are presented in Figure 7.

Figure 7 Multiple regression analysis results for the differences in ROE, profit margins, total asset turnover, and financial leverage between the pre-event and post-event three-year periods for 54 companies

(Source) Compiled by Dai-ichi Life Research Institute based on Bloomberg data

The estimated model is:

ΔROE = 1.3659ΔMargin + 0.0770ΔAsset Turnover + 0.000003ΔLeverage + 0.0127

(Δ denotes the difference between post-event and pre-event three-year averages.)

Based on the magnitude of the p-values, profit margin is statistically highly significant and is shown to be strongly associated with changes in ROE. Total asset turnover is also statistically significant, whereas financial leverage is not. The coefficient of determination (R-squared) is 0.8197, indicating a high level of explanatory power, and suggesting that variations in ROE can be largely explained by variations in the components derived from the DuPont decomposition (Note 13).

Taken together, the results of the mean-difference tests in the previous subsection and the multiple regression analysis in this subsection indicate that improvements in ROE are associated with improvements in profit margins and total asset turnover, both of which exhibit statistically significant relationships in the two analyses. By contrast, no contribution from financial leverage is identified.

5. Implications

The analysis conducted in this report indicates that, among firms with scope for improvement in profitability, the appointment of a majority of independent outside directors is associated with a tendency toward higher ROE in the post-event period. This improvement in ROE is achieved through enhancements in profit margins and total asset turnover, rather than through the manipulation of financial leverage. In other words, the observed improvement in ROE does not appear to result from temporary adjustments such as increased borrowing or expanded shareholder payouts, but rather from substantive managerial decisions that raise profitability—namely, improvements in pricing strategies, cost structures, and reforms of business portfolios.

The confirmed improvement in total asset turnover further suggests the possibility that more effective utilization of assets and a reassessment of business portfolios progressed following the event (Note 14). These findings therefore provide indirect, albeit not definitive, partial evidence countering critiques that corporate governance reforms implemented through the utilization of independent outside directors necessarily lead to short-term–oriented management.

The increased utilization of independent outside directors, which has become particularly pronounced since the initiation of Japan’s corporate governance reforms in 2015, is thus shown to be meaningful for firms with potential for profitability improvement. The results of this analysis suggest that the significance of such governance reforms cannot be readily dismissed.

6. Conclusion

While the analysis presented in this report clarifies that, among firms with room for improvement in profitability, the event of appointing a majority of independent directors is associated with improvements in ROE and identifies the channels through which such ROE improvements occur, it does not directly establish the causal effects of corporate governance reform itself. It should also be noted that the analysis focuses on short- to medium-term performance changes over the three-year pre-event and post-event periods and does not evaluate the impact on long-term corporate value over horizons such as five or ten years.

Moreover, this report does not suggest that, for firms with potential for ROE improvement, simply appointing a majority of independent outside directors will automatically lead to higher profit margins and, consequently, improved ROE. The 54 firms examined in this analysis presumably made autonomous and proactive decisions to appoint a majority of independent outside directors. In doing so, they are likely to have selected individuals suited to the specific challenges facing their respective firms and to have devoted effort to ensuring that independent outside directors could effectively fulfill their roles. The appropriate selection of qualified independent outside directors and their effective utilization should therefore be regarded as essential preconditions.

The mechanisms through which the ROE improvements observed in this analysis—achieved via enhancements in profit margins and total asset turnover—emerged as a result of firms’ responses at the time of governance reform implementation remain an important subject for future research. Addressing this issue will require not only statistical analyses of the type conducted in this report, but also studies incorporating detailed case analyses of firms that represent successful examples. As such research accumulates, it is hoped that Japanese firms, which are increasingly expected to achieve higher levels of sustainable growth, will be able to implement truly effective corporate governance reforms, allowing society at large to benefit from their outcomes.

Finally, as noted at the outset, revisions to the Corporate Governance Code are anticipated this year, and the direction of the next revision to the Companies Act is also expected to become clearer. In examining institutional arrangements from both regulatory (“hard law”) and non-regulatory (“soft law”) perspectives, it is desirable that reforms be grounded in objective and empirical research so as to lead to genuinely effective institutional design. Without disregarding past achievements, it is hoped that policy design will advance through the integration of insights from a wide range of experts, thereby supporting corporate reform efforts.

[Notes]

- Recent studies include research suggesting that corporate governance reform has accelerated the unwinding of cross-shareholdings among firms (Miyajima and Saito, 2023).

- The analysis conducted in this report examines the relationship between corporate governance reform and corporate performance, and it should be noted that it does not identify causal relationships. Within this context, while much of the existing literature focuses on macro-level trends, this report is distinguished by its emphasis on firms’ autonomous governance decisions.

- In a narrow sense, an event study is a methodology used to examine the impact of specific events—such as mergers or corporate scandals—on stock prices or firm value by analyzing abnormal returns around the event window. In contrast, the broad event-study framework employed in this report refers to an event-based analysis that examines medium-term changes in accounting-based performance indicators, taking specific institutional or managerial events as the point of departure.

- During the period covered by this analysis, no institutional changes in accounting standards occurred that would affect the calculation of ROE for listed firms in Japan. While individual firms may have voluntarily adopted IFRS, such changes represent firm-specific factors. As the majority of firms in the sample continued to apply either Japanese accounting standards or IFRS consistently, the potential impact on the analytical results is considered to be limited.

- At the end of March 2023, the Tokyo Stock Exchange issued a request entitled “Actions Toward the Realization of Management that Is Conscious of Capital Cost and Stock Price” to companies listed on the Prime and Standard Markets, and has since continued to call for various related initiatives. Within this framework, ROE is emphasized as a key indicator of management that is attentive to capital costs.

- Under Principle 4-8 of the current Corporate Governance Code, companies listed on the Prime Market are required to appoint independent outside directors constituting at least one-third of the board. This principle was strengthened in the 2021 revision, replacing the previous requirement of appointing “at least multiple” independent outside directors.

-

DuPont decomposition refers to the breakdown of ROE into the following three financial components:

ROE = Margin (Profit / Sales) × Total Asset Turnover (Sales / Total Assets) × Leverage (Total Assets / Shareholders’ Equity) - While Figure 3 presents the data sheet constructed for ROE, similar data sheets were also created for profit margin, total asset turnover, and financial leverage.

- A statistical test is a method used to assess whether observed differences or changes in data are likely to have arisen by chance. The t-test is a representative statistical test that focuses on differences in the means of two sample groups to determine whether such differences are statistically meaningful. It is also applicable when sample sizes are small and the variance of the underlying population cannot be reliably estimated.

- A p-value represents the probability that the observed difference would occur under the assumption that no true difference exists. A smaller p-value indicates that the observed difference is less likely to be attributable to chance. When one value is hypothesized to be greater than the other, a one-sided p-value is used; when the direction of the difference is unknown, a two-sided p-value is applied.

- Although not reported in detail here, no increase in post-event three-year average ROE of the type identified in this analysis was observed for firms whose pre-event three-year average ROE was 15 percent or higher.

- Multiple regression analysis is an analytical method that examines how well a dependent variable—in this case, the difference in ROE—can be explained by multiple explanatory variables, namely differences in profit margin, total asset turnover, and financial leverage. It also provides indicators of the relative importance of each explanatory variable. It should be noted that the results presented here are limited to firms with room for ROE improvement and do not necessarily apply to all firms in general.

- Although the components of the DuPont decomposition may exhibit some degree of correlation, this analysis finds no evidence of multicollinearity at a level that would affect the main conclusions—that is, a situation in which two or more explanatory variables are highly correlated with one another.

- The observed improvement in total asset turnover may also reflect reductions in non-core assets, including the unwinding of cross-shareholdings.

[References]

- Miyajima Hideaki・Saitou Takumi (2023) “Corporate Governance Reform and the Sale of Policy-Held Shares: Determinants and Economic Consequences” The Research Institute of Economy, Trade and Industry

- Arikawa Yasuhiro・Miyajima Hideaki・Saitou Takumi (2025) “Overview of the Evolution of Corporate Governance: The impact of reforms and the future of Japanese firms” The Research Institute of Economy, Trade and Industry

- Financial Services Agency “Secretariat Materials” Follow-up Meeting on the Stewardship Code and the Corporate Governance Code 27th Meeting (https://www.fsa.go.jp/singi/follow-up/siryou/20220516/02.pdf)

- Yoshio Kawatani (2022) “How to Leverage Outside Directors(1)~Increased Appointment of Outside Directors and Their Utilization in the Nomination and Compensation Committee~” (https://www.dlri.co.jp/report/ld/205864.html)

- Yoshio Kawatani (2022) “How to Leverage Outside Directors(2) ~ Regarding the Appointment of an Outside Director as Chairman of the Board of Directors~” (https://www.dlri.co.jp/report/ld/205867.html)

- Yoshio Kawatani (2022) “How to Leverage Outside Directors(3)~Challenges from the Perspective of Outside Directors~” (https://www.dlri.co.jp/report/ld/205870.html)

- Yoshio Kawatani (2024) “Changes Following the Creation of the Prime Market(2)~From the perspective of the appointment status of outside directors~” (https://www.dlri.co.jp/report/ld/330590.html)

- Yoshio Kawatani (2025) “Current Status and Future Outlook of Appointing Outside Directors as Board Chairpersons~Based on a comparison between August 2025 and July 2022~” (https://www.dlri.co.jp/report/ld/500946.html)

- Yoshio Kawatani (2025) “What Japanese Companies Need to Improve Their ROE~Considerations Based on the Long-Term Dupont Decomposition Since the 1980s~” (https://www.dlri.co.jp/report/ld/551238.html)

Original in Japanese:

https://www.dlri.co.jp/report/ld/575399.html

Disclaimer:

This report has been prepared for general information purposes only and is not intended to solicit investment. It is based on information that, at the time of preparation, was deemed credible by Daiichi Life Research Institute, but it accepts no responsibility for its accuracy or completeness.