- Report Index

- Japan Economic Outlook (May 2026)

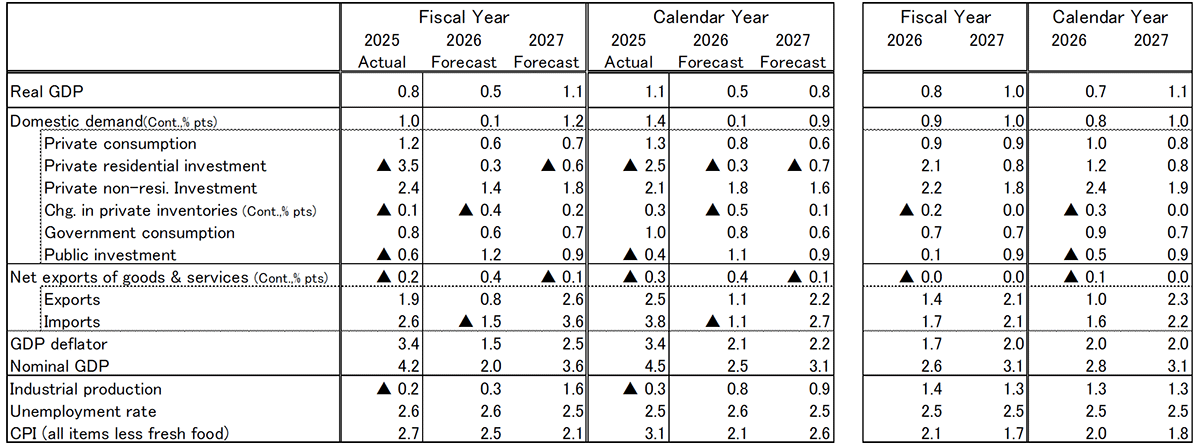

Real GDP growth is forecast at +0.5% in FY2026 (March forecast: +0.8%) and +1.1% in FY2027 (previously +1.0%). On a calendar-year basis, growth is projected at +0.5% in 2026 (previously +0.7%) and +0.8% in 2027 (previously +1.1%). The FY2026 growth forecast has been revised downward, reflecting persistently high crude oil prices amid escalating tensions surrounding Iran, the partial materialization of adverse effects from supply constraints and sourcing difficulties in petroleum-related products, and expected downward pressure on private consumption through higher energy and food prices.

With regard to developments in the Middle East, the forecast assumes that tensions will ease by the summer of 2026, as both the United States and Iran are likely to seek to avoid a prolonged conflict. Under the main scenario, disruptions surrounding the de facto blockade of the Strait of Hormuz are expected to ease, allowing supply uncertainty to subside and limiting disruptions caused by sourcing difficulties to a temporary phenomenon. At the same time, even if the de facto blockade of the Strait of Hormuz is lifted and supply constraints begin to ease, crude oil prices may not quickly return to pre-crisis levels. This reflects the likelihood that caution over renewed tensions will persist, insurance premiums will remain elevated, and normalization of supply facilities and logistics networks in Middle Eastern countries will take time. In this forecast, Dubai crude oil prices are assumed to be around USD 80 per barrel at end-2026 and around USD 70 per barrel at end-2027. A possible reduction in the consumption tax rate on food products has not been incorporated into the outlook, as details remain unclear at present regarding whether it will be implemented, when it would take effect, and how it would be financed.

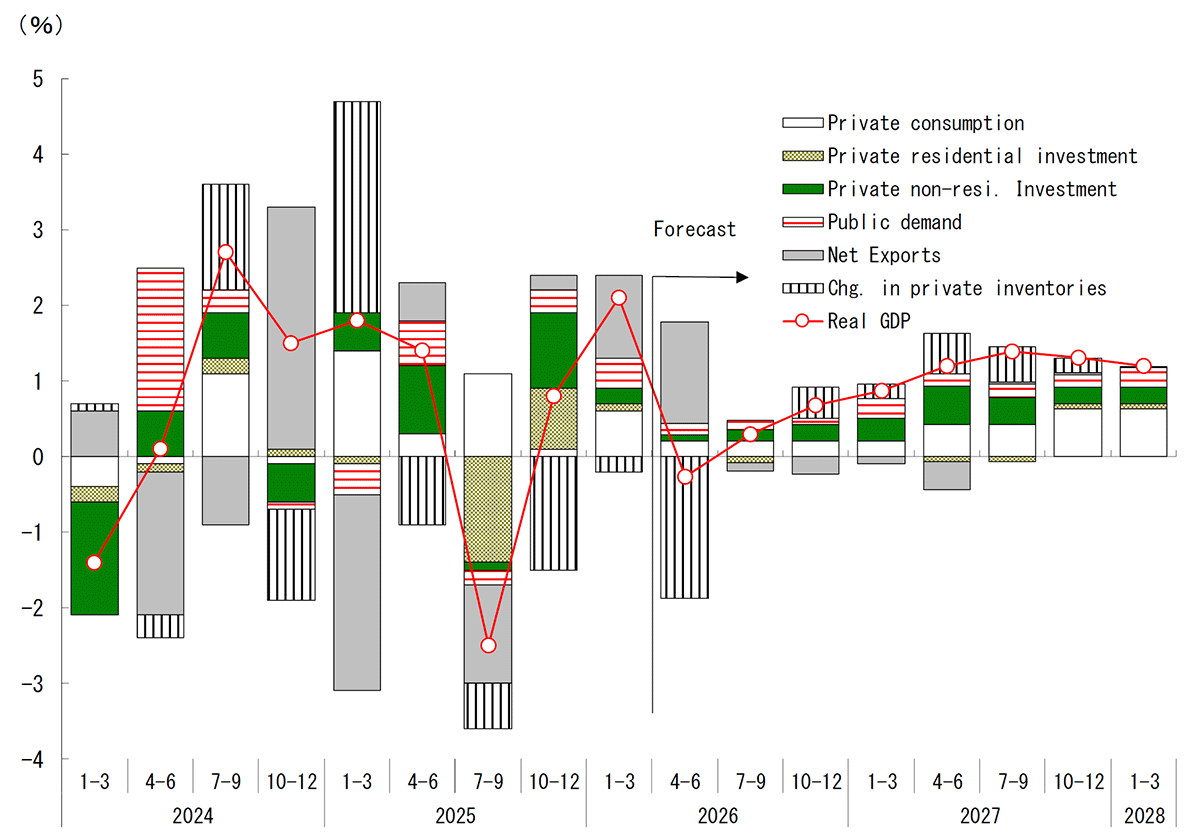

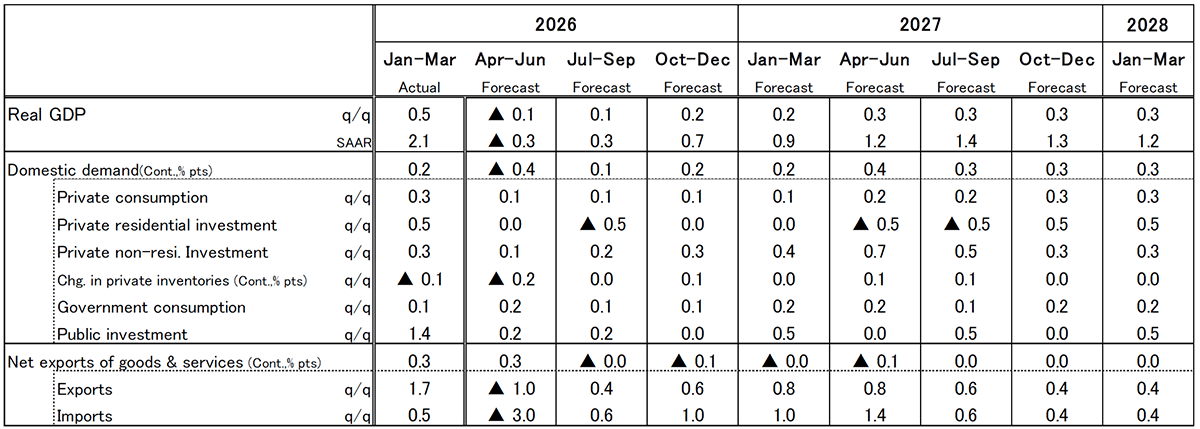

Real GDP growth in Q1 2026 (January–March) came in at +2.1% on a quarter-on-quarter annualized basis, marking the second consecutive quarter of positive growth. Private consumption and business investment continued to increase, while exports also posted strong growth. Both domestic and external demand remained resilient, resulting in growth above the potential growth rate. The data suggest that, prior to the full impact of escalating Iran-related tensions, Japan’s economy had maintained a moderate recovery trend.

Looking ahead, however, downward pressure on the economy is likely to intensify as the effects of worsening geopolitical tensions involving Iran become more pronounced. The primary concern is the adverse impact of supply constraints and sourcing difficulties. In periods of supply uncertainty, firms tend to secure and build up inventories earlier than usual to ensure business continuity, which may further tighten supply-demand conditions. Recently, sourcing difficulties—including delivery delays and order restrictions—have begun to emerge in sectors such as petrochemicals and construction materials. Going forward, these developments could constrain economic activity through delays in production and shipments, as well as postponements or interruptions in construction work. Exports are also likely to face downward pressure. Exports to the Middle East are expected to remain weak for the time being, while supply constraints could weigh on production activity both in Japan and abroad. Against this backdrop, real GDP growth in Q2 2026 (April–June) is forecast to turn slightly negative, at –0.3% annualized quarter-on-quarter.

Although the economy is expected to stagnate in the near term, there is no need to conclude that the recovery scenario itself has collapsed. At present, concerns over declining imports and constrained supply are being compounded by firms’ precautionary inventory accumulation in anticipation of future supply shortages, contributing to distribution bottlenecks and sourcing difficulties. If the outlook for supply normalization becomes clearer as the situation surrounding the Strait of Hormuz moves toward resolution, the view that inventories and alternative sourcing can cover near-term needs is likely to spread. Supply uncertainty and related disruptions would then subside. In this case, the decline in Q2 would be temporary, and growth would likely return to positive territory from Q3 2026 onward.

Even if the adverse effects of supply constraints ease, the impact on prices and the associated drag on the economy are likely to persist for some time. Resource prices remaining above pre-crisis levels will weigh on corporate profits, while higher inflation stemming from pass-through to food prices and electricity and gas charges will exert downward pressure on private consumption. In the previous forecast, private consumption in FY2026 was expected to become more stable, supported by moderating inflation and a recovery in real wages. However, the outlook for consumption has been revised downward to reflect the negative impact of stronger-than-expected inflation.

That said, corporate profits are currently at historically high levels, suggesting that firms have a solid degree of resilience to the shock. Even amid rising costs, firms’ positive stance toward business investment is expected to remain intact, particularly in areas such as digitalization and labor-saving investment. Private consumption is also unlikely to stall, despite the unavoidable negative impact of higher prices, supported by continued strong wage growth, government subsidies for energy prices, and a resilient labor market. If stock prices remain elevated, wealth effects should also provide some support. Exports are expected to be underpinned by the resilience of the U.S. economy. As a resource-exporting country, the United States is less adversely affected by the terms-of-trade impact of higher oil prices than resource-importing economies, which should also support external demand. Although downside risks to the European and Asian economies remain a concern, exports as a whole are unlikely to decline sharply. As a result, the economy is expected to continue a moderate recovery in the second half of FY2026, albeit without strong momentum.

In FY2027, the recovery is expected to gain momentum gradually as the adverse effects of high oil prices fade. As the drag from Middle East tensions eases, the global economy is expected to recover, supporting a pickup in exports. Corporate profits should also improve as cost pressures from elevated oil prices diminish, reinforcing firms’ willingness to invest. In addition, as upward pressure on energy and food prices weakens and inflation peaks out, private consumption is expected to increase moderately. With both domestic and external demand improving, real GDP growth in FY2027 is forecast to recover to +1.1% year-on-year, from +0.5% in FY2026.

The key risk factor is a prolonged deterioration in Middle East conditions. The main scenario assumes that negotiations between Iran and the United States will reach an agreement, improving conditions surrounding the Strait of Hormuz and easing supply uncertainty. However, the outlook for negotiations remains uncertain, and prolonged tensions cannot be ruled out. In such a case, firms would become increasingly concerned about the limits of relying on inventories and alternative sourcing to cope with supply constraints. If firms accelerate inventory accumulation, disruptions could intensify further and upward pressure on prices would likely strengthen. Production activity and construction work could remain depressed for an extended period, while exports could face larger downside risks. If such a scenario materializes, FY2026 growth could turn negative, raising the risk of a recession.

The core consumer price index (CPI, excluding fresh food) is forecast to rise by +2.5% in FY2026 (March forecast: +2.1%) and +2.1% in FY2027 (previously +1.7%), representing an upward revision from the previous forecast. Although food price inflation has recently moderated and inflation would normally be expected to decline gradually, upward pressure on prices in FY2026 will persist. This reflects elevated resource prices amid geopolitical tensions, pass-through from higher naphtha prices to packaging materials, logistics costs, and processed food prices, as well as lagged increases in electricity and gas charges. Firms’ more proactive stance toward price pass-through compared with the past will also contribute to higher inflation. From the summer of 2026 onward, the government is expected to implement subsidies for electricity and gas charges, which should provide some restraint on inflation. However, these measures are unlikely to fully offset the upward pressure from higher resource prices. Inflation is therefore likely to rise in the second half of FY2026, led mainly by electricity and gas charges and food prices excluding fresh food. In FY2027, these inflationary pressures are expected to gradually dissipate. On a quarterly basis, inflation is likely to peak in Q1 2027 and moderate thereafter.

Japan’s Economic Outlook (Yearly)

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office, Ministry of Economy, Trade and Industry, Ministry of Internal Affairs and Communications.

Forecast of Real GDP (Quarter-on-Quarter Annualized Rate, Contribution)

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office.

Japan’s Economic Outlook (Quarterly)

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office.

Original in Japanese:

https://www.dlri.co.jp/report/macro/607272.html

Disclaimer:

This report has been prepared for general information purposes only and is not intended to solicit investment. It is based on information that, at the time of preparation, was deemed credible by Daiichi Life Research Institute, but it accepts no responsibility for its accuracy or completeness. Forecasts are subject to change without notice. In addition, the information provided may not always be consistent with the investment policies, etc. of Daiichi Life or its affiliates.