- Report Index

- World Economic Outlook (November 2025)

- Economic Trends

-

2025.11

World Economic Outlook (November 2025)

Yoshiki Shinke, Seiji Katsurahata, Osamu Tanaka, Toru Nishihama

1. Japan Economy

Current state of the economy: Negative growth driven by a sharp decline in housing investment.

Real GDP (Quarter-on-Quarter Annualized Rate, Contribution)

Source: Cabinet Office.

Real GDP growth in 2025 Q3 (July–September) showed an annualized quarter-on-quarter decline of –1.8%, marking the first contraction in six quarters. The primary driver of the negative growth was housing investment, which alone pushed down the annualized growth rate by –1.4 percentage points.

Due to the legal revisions implemented in April 2025, the costs of new housing construction and large-scale renovations increased, administrative burdens rose, and construction periods became longer. Many developers, seeking to avoid these burdens, brought forward construction starts ahead of the revisions, resulting in a surge in housing starts in March. Subsequently, however, the payback from this front-loaded demand caused housing starts to record a historically large decline in Q2 (April–June). With a time lag, this decline fed into housing investment, which dropped sharply by –9.4% quarter-on-quarter in Q3.

However, the fall in housing investment is likely temporary, and part of the export decline reflects a payback from strong gains in Q2. Thus, the weakness in Q3 does not guarantee excessive pessimism. On average with prior positive quarters, the economy remains on a modest upward trend. Despite tariff hikes, the U.S. economy has stayed resilient, helping Japan avoid the sharp export slowdown that had been feared. So far, no signs of a broader downturn have emerged.

Economic outlook: The economy is set to improve in FY2026.

Japan's Economic Outlook (Yearly)

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office, Ministry of Economy, Trade and Industry, Ministry of Internal Affairs and Communications.

Nonetheless, uncertainty persists regarding the export outlook. While the U.S. economy remains firm, a gradual slowdown is under way. As the pass-through of higher tariffs progresses and labor market conditions soften, consumption—particularly among lower-income households—is expected to face increasing downward pressure. Japanese automakers have so far avoided sales declines in the U.S. by lowering export prices to offset tariffs, but with the tariff rate now fixed at 15%, price increases appear inevitable, likely weighing on U.S. sales volumes. Exports therefore remain likely to decline in 2025 Q4. Although GDP growth should return to positive territory—supported by a stabilization in housing investment and an increase in capital spending—the rebound will likely be modest relative to the Q3 downturn, with growth forecast at +0.4% on an annualized basis. In the absence of a strong growth driver, the Japanese economy is expected to see only a mild recovery in the second half of the fiscal year.

In FY2026, the economy is projected to continue a gradual recovery. While the negative effects of U.S. tariff hikes will linger, earlier interest rate cuts will increasingly support economic activity with a lag. Tax reductions will also contribute to the U.S. recovery. As the U.S. economy stabilizes, Japanese exports are expected to bottom out, helping to stem the deterioration in corporate earnings. An improved profit environment and reduced uncertainty should support a moderate increase in capital investment.

Another positive factor will be the stabilization of real wages. Wage negotiations in spring 2026 are expected to deliver an average wage increase of 5.20% (Ministry of Health, Labor and Welfare basis), marking the third consecutive year of 5%-range gains. Contributing factors include: (1) deepening labor shortages, (2) continued high inflation and efforts to offset declines in real wages, and (3) strong corporate earnings. As cost-push pressures ease and inflation moderates, real wages are projected to return to positive territory. This should help stabilize private consumption, although the increase in real income is expected to be modest, limiting the strength of consumption growth.

2. US Economy

Current state of the economy: Economic slowdown and labor market softening due to increasing uncertainty

In the United States, amidst growing policy uncertainty surrounding Trump 2.0, a partial government shutdown occurred for 43 days from October 1 to November 12. This surpassed the previous record of 35 days set during the first Trump administration. Financial markets remained relatively stable during this period, but the publication and compilation of economic indicators was suspended. Available data indicates a gradual economic slowdown, a softening labor market, and persistent inflationary pressures.

Regarding private economic statistics for October, ISM Report on Business, which measures business sentiment, showed that the manufacturing index fell below 50 at 48.7 (49.1 the previous month). Meanwhile, the non-manufacturing index rose to 52.4 (50.0 the previous month), collectively indicating a gradual economic slowdown. Since the inauguration of Trump 2.0, the manufacturing sector has continued to shrink. In contrast, the non-manufacturing sector has continued to expand, supporting U.S. economic growth. The Employment Index from the same statistics showed a slowdown in the pace of employment contraction. Furthermore, the ADP Nonfarm Private Employment Index turned positive compared to the previous month, suggesting the labor market may be able to avoid further weakening.

Turning to inflation, the core CPI's upward momentum rose to an annualized +3.0% over the past six months (+2.7% in the previous month) and continued to grow at a high annualized rate of +3.6% over the past three months (+3.6% in the previous month), indicating that inflationary pressures remain strong. However, the 10-year breakeven inflation rate (calculated as the difference between the 10-year Treasury yield and the 10-year Treasury Inflation-Protected Securities yield), an indicator of financial market inflation expectations, remained stable through November 18, indicating continued expectations that the impact of tariffs on prices will be temporary.

At its October FOMC meeting, the Federal Reserve decided to lower interest rates for the second consecutive meeting and announced it would end its balance sheet reduction measures on December 1. Ten members voted to lower the federal funds rate target range by 25 basis points to 3.75%–4.00%. However, Governor Milan believed a 50 basis point cut was appropriate, while Kansas City Fed President Schmidt opposed the 25 basis point cut, believing the range should be left unchanged.

Chairman Powell pointed out that "inflation remains somewhat elevated, but the labor market is gradually cooling," explaining, "Given the shifting risk balance in the form of increased risks to the labor market, we judged it appropriate to take another step toward a more neutral policy stance, and we decided to lower the rate as a risk management measure." However, regarding future monetary policy, Chairman Powell emphasized that there was "significant division of views" among FOMC members regarding the policy path. He explained that with upside risks to inflation and downside risks to the labor market, and there are differing opinions on what should be done and how quickly. He then stated that further rate cuts at the next FOMC meeting in December are not a given, emphasizing that views are divided: "Some members believe it is time to maintain a cautious stance, while others favor further rate cuts."

ADP US nonfarm private employment (MoM)

Source: ADP

US core CPI

Source: US Department of Labor

Economic outlook: US economy expected to remain strong in 2026

Trump 2.0's trade policy primarily involves the imposition of reciprocal and product-specific tariffs. While major trade wars have largely been avoided, and trade negotiations have progressed and agreements have been reached with various countries. Trade agreements were reached with the UK in May, Vietnam, Indonesia, the Philippines, Japan, the EU, and South Korea in July, Cambodia and Thailand in October, and Switzerland, Liechtenstein, Argentina, Ecuador, El Salvador, and Guatemala in November. These agreements are structured to limit U.S. tariff increases while requiring partner countries to eliminate tariffs on U.S. imports, increase imports of agricultural products, energy, and aircraft, and increase investment in the U.S., resulting in largely unilateral benefits for the U.S. These agreements are expected to boost U.S. economic growth and, in addition to tariffs, are likely to increase inflationary pressures.

At the end of October, the United States and China agreed to a one-year postponement of strengthened export restrictions and the scheduled tariff increases on rare earths. Specifically, (1) the United States will reduce reciprocal tariffs by 10% and lower tariffs imposed as a measure against synthetic drugs (fentanyl) to 10%. (2) China will suspend for one year the tightening of export restrictions on rare earth-related items that it had recently announced. (3) The United States will suspend for one year the implementation of the "50% rule," which prohibits transactions with subsidiaries of embargoed Chinese companies in which they hold a 50% or greater stake. Following this agreement, concerns about rising inflation and technology regulations have temporarily eased, gradually easing uncertainty. However, there is a risk of tariff increases if the Trump administration determines that countries and regions are not fully implementing trade agreements, in addition to plans to impose tariffs on pharmaceuticals, semiconductors, and other products.

Real GDP growth is expected to slow to an annualized around +1% in Q4 2025 due to the effects of the partial government shutdown, the rise in real interest rates, and rising prices, all of which have been restraining economic activity. However, growth is likely to accelerate again in Q1 2026, boosted by the full reopening of government agencies and the effects of tax cuts.

Personal consumption in 2026, despite being impacted by rising prices, is expected to remain robust, supported by tax cuts and increases in asset balances such as stocks and real estate. Capital investment growth is also likely to accelerate due to the effects of tax cuts, expanded IT demand, the easing of uncertainty resulting from the trade agreement, and increased direct investment. Furthermore, exports of agricultural products and energy are expected to expand as a result of the trade agreement. As a result, the U.S. economy is likely to grow above its potential rate (+1.8%).

Inflation is likely to rise moderately as the impact of tariffs gradually becomes apparent, despite a continued decline in housing-related demand. In this environment, the Federal Reserve is expected to become more cautious about lowering interest rates in 2026.

US economic outlook (YoY, %)

Source: US Department of Commerce,Our forecast

Note: Contribution is in parentheses

U.S. real GDP growth (SAAR)

Source: US Department of Commerce. Forecast is our own.

3. European Economy

Current state of the economy: Reassurance spreads amid tariff agreement and fiscal shift

Over recent years, the eurozone economy has remained stuck in low growth below 1%, falling short of its potential growth rate. Following Russia's invasion of Ukraine, energy prices have remained elevated in Germany and Italy, both heavily reliant on Russian fossil fuels, eroding industrial competitiveness and corporate vitality. Global trade frictions and intensifying competition from emerging market firms, particularly in China, are also weighing heavily on these two countries, both manufacturing powerhouses with high export dependency. France, too, continues to face an unstable economic environment, burdened by fiscal concerns and ongoing political turmoil. Despite the persistent economic weakness in these core countries, the eurozone has maintained a slow but steady growth trajectory. This resilience stems largely from the robust performance of Spain, Portugal, Greece, and Ireland, which entered EU fiscal support programmes during the European debt crisis of the early 2010s. These nations undertook structural reforms during their recovery from the crisis, while increased immigration, robust tourism demand, and economic activity by multinational corporations have contributed to their improved economic conditions.

Entering 2025, the economy grew significantly in the January-March quarter due to a surge in exports ahead of US tariff hikes. This was followed by a slowdown in the April-June and July-September quarters, partly due to a reactionary effect, though it has maintained a moderate recovery trajectory. While the impact of tariff hikes on exporting companies is unavoidable, the avoidance of punitive high tariffs and retaliatory tit-for-tat measures, coupled with reduced uncertainty surrounding US-EU tariff negotiations and the resumption of previously postponed economic activities, has bolstered the expansion. Furthermore, Germany, which has long pursued restrictive fiscal policies, has revised its ‘debt brake’ – which mandated balanced budgets – and created a special fund for infrastructure investment, defense spending, and climate change measures, steering towards bold fiscal expansion. This move has been well received.

Eurozone consumer prices are cooling from historically high inflation, driven by the fading impact of energy and food price hikes. Signs of moderation are also spreading to service prices, which have remained stubbornly high, including wage growth peaking out. Reflecting receding inflationary pressures, the European Central Bank (ECB) has been cutting interest rates since mid-last year. The lower bound policy rate (deposit facility rate) currently stands at 2%, reaching the ECB's estimated neutral rate (the policy rate that neither overheats nor restrains the economy). With signs of economic recovery spreading, the ECB has held off on further rate cuts since July.

Real GDP for Major Euroarea Countries

Source: Eurostat, Dai-ichi Life Research Institute

Harmonised Index of Consumer Prices in Euroarea

Source: Eurostat, Dai-ichi Life Research Institute

Economic outlook: Recovery accelerates as fiscal expansion takes effect

Germany's historic shift in fiscal policy saw some measures incorporated into the 2025 supplementary budget, though most will fully take effect from 2026 onwards. Other EU nations, responding to shifts in Europe's security environment, are also steering towards increased defense spending. To support member states in raising defense budgets, the EU will temporarily exempt defense expenditure from its fiscal rules and provide member states with fiscal funding through the issuance of EU bonds. Some view the spillover effects on other demand as limited since most of the rise in defense spending is expected to lead to increased orders for defense goods from outside the EU, primarily from the United States. Rising long-term interest rates, driven by concerns over fiscal deterioration, may also dampen private sector demand. However, this plan anticipates increased orders from within the EU, meaning the overall economic stimulus effect is likely to prevail.

Alongside this expansion in fiscal spending, centered on defense expenditure, the eurozone recovery is expected to accelerate from 2026. This acceleration will be supported by the restoration of household purchasing power through inflation moderation and wage increases, alongside the materialisation of previous interest rate cut effects. Furthermore, no significant deterioration is anticipated in the economic environment surrounding Southern Europe and Ireland, which have underpinned the expansion thus far. Notably, new lending under the European Recovery Fund, which provides the fiscal resources needed for recovery from the COVID-19 crisis, primarily to Southern and Eastern European countries, is set to be phased out during 2026. With much of the lending envelope still unutilised, increased last-minute take-up before the closure of new applications is also likely to bolster economic expansion in 2026.

The eurozone's growth rate for 2026 is forecast to slow slightly to +1.2% from +1.3% in 2025. This deceleration is influenced by the stronger annual growth rate in 2025, driven by the surge in exports during the January-March quarter ahead of tariff increases. Ireland, which exports significant pharmaceuticals to the US, is projected to achieve growth of around 10% in 2025 – the highest among advanced economies – driven by substantial pre-tariff export surges. Excluding these special factors, net growth is anticipated to accelerate in 2026. Risks to the economic scenario include financial market turbulence stemming from political turmoil in France, the persistence of Germany's structural challenges, a resurgence of trade friction with the US over the implementation of tariff agreements, and heightened geopolitical tensions in Ukraine and the Middle East.

With the acceleration of the economic recovery confirmed and the achievement of medium-term price stability coming into view, the ECB is highly likely to maintain its wait-and-see stance. While the ECB currently retains room to resume rate cuts, citing high uncertainty, it is expected to begin revising its forward guidance in 2026, with an eye towards a future shift towards rate hikes.

Outlook of the Euroarea Economy (YoY, %)

Note: Figures in brackets are contributions to real GDP growth.

Source: Dai-ichi Life Research Institute

4. China and Emerging Asian Economies

Current state of the economy: A surge of last-minute shipments ahead of the full implementation of the Trump tariffs is providing support to Asian economies.

In spite of the concerns over excess supply stemming from China’s overcapacity continue to persist, economic expansion driven by the supply side remains intact. Meanwhile, in China, the prolonged real estate downturn and the sluggish recovery of employment, especially among younger generations, have strengthened households’ propensity to save, leaving private consumption lackluster. Furthermore, weak real-estate demand has constrained fixed-capital investment, resulting in broadly subdued domestic demand.

The Trump administration’s tariff policy targeted China, and initially there were concerns that the onset of a trade war would negatively affect external demand. However, following subsequent trade negotiations, the U.S. and China avoided the worst-case scenario by removing retaliatory tariffs and suspending additional tariffs and export restrictions. In addition, with worsening U.S.–China relations in mind, Chinese authorities have been actively boosting exports to destinations other than the U.S., offsetting downward pressure on exports to the U.S.

In financial markets, although the renminbi has remained firm against the U.S. dollar, the CFETS RMB Index, a currency basket, remains at a relatively undervalued level, continuing to support current export performance. While the Chinese government has strengthened policy measures to stimulate domestic demand since the second half of last year, signs of peaking out of stimulus have recently begun to appear. Even so, economic growth reached +5.2% through September of this year, maintaining an expansion above the government’s target of “around 5%”.

Regarding Asian emerging economies, the Trump administration initially imposed high reciprocal tariffs on countries that had benefited from the U.S.–China trade conflict by expanding exports to the U.S. through indirect exports from China. However, following trade negotiations with U.S., reciprocal tariffs on major ASEAN economies were set at around 19–20%, avoiding the differences in tariff rates adversely affect export competitiveness. Prior to the full implementation of Trump’s tariffs, rush shipments to the U.S. and increased roundabout trade of Chinese goods also provided support to external demand, helping to boost economic activity.

In recent years, Asian emerging economies experienced inflation driven largely by elevated commodity prices and frequent abnormal weather events that raised prices of daily necessities such as food. However, as these pressures have eased, inflation in many countries has stabilized. With uncertainty surrounding external demand rising, central banks across the region have turned to rate cuts to support domestic demand, helping sustain economic momentum.

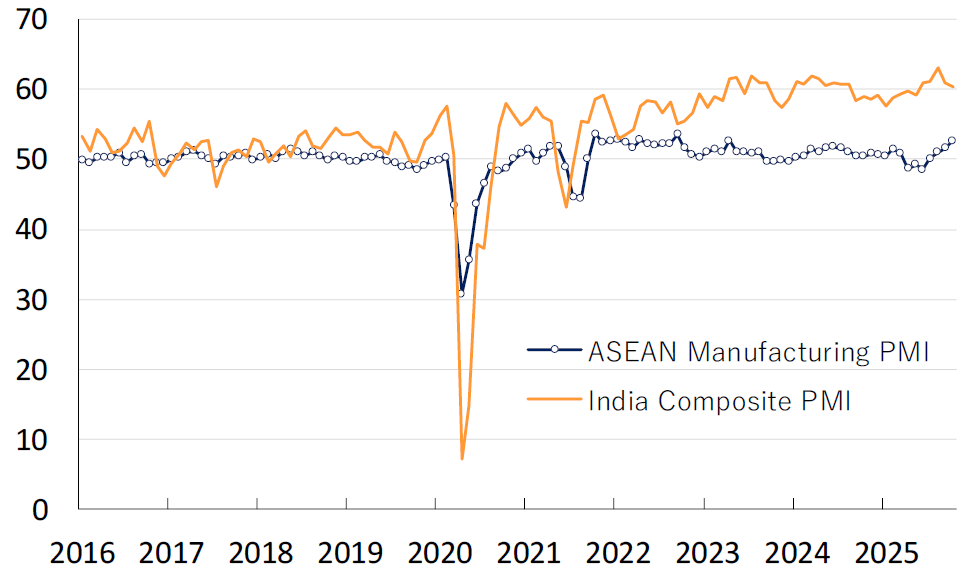

Meanwhile, the U.S. sharply raised reciprocal tariffs on India to 50%, citing India’s increased imports of Russian crude oil. Nevertheless, Indian economy is relatively less dependent on exports to the U.S. on the macroeconomic front. In addition, the Indian government has strengthened measures to stimulate domestic demand, such as reducing the Goods and Services Tax (GST). The policy is promoting lower inflation, helping underpin economic conditions. As a result, the impact of “Trump tariffs” on economic activity remains limited at this point.

RartingDog China Mfg. and Services PMI

Source: S&P Global

S&P India Comp. PMI and ASEAN Mfg. PMI

Source: S&P Global

Economic outlook: While U.S.–China tensions subside, China will continue to expand supply, and Asian countries will face the spillover effects.

Following the U.S.–China summit, both countries showed signs of compromise. China postponed for one year the implementation of its strengthened export controls on rare earths, while the United States not only removed retaliatory tariffs but also agreed to cooperate on measures against fentanyl, reducing the additional tariffs related to fentanyl issues. Furthermore, the U.S. suspended for one year the addition of Chinese firms to its export-control list and halted the collection of port-entry fees on Chinese vessels; in reciprocity, China suspended for one year its special port fees on U.S.-related vessels. Both sides also agreed to suspend for one year the additional tariff (24%). As a result of these measures, the tariffs imposed on China under the 2nd Trump administration will stand at 20%, roughly in line with the rates applied to major ASEAN economies.

China has offset declining exports to the U.S. by expanding shipments to other countries and regions, but the economic incentives for such transshipment through third countries, like ASEAN countries, will decline significantly. Therefore, China is expected to further accelerate exports across all destinations going forward. On the other hand, the effects of domestic-demand stimulus measures introduced by Chinese authorities have largely run their course, raising concerns about a potential payback phase. At the Fourth Plenary Session held in October, the importance of expanding domestic demand under the 15th Five-Year Plan was acknowledged, but no concrete measures were presented. As a result, uncertainty surrounding the outlook for domestic demand remains, and policy support may stay limited. In 2026, Chinese economy is expected to continue being driven primarily by supply-side strength, while demand prospects will remain difficult to forecast.

The easing of U.S.–China tensions is expected to provide a tailwind for Asian emerging economies, which have comparatively high dependence on external demand, by supporting an expansion in global trade. However, the tariffs the U.S. will impose on China and Asian emerging economies under the 2nd Trump administration will be roughly at the same level, reducing China’s incentives for transshipment. Moreover, the U.S. has included a “poison pill clause” in trade agreements with ASEAN countries, that allows for unilateral termination, increasing the likelihood that Asian emerging economies will become a stage for proxy conflicts in U.S.–China friction. In addition, a payback phase is expected after the earlier rush in exports to the U.S., and the indirect pushing up from China’s transshipment activity will become less reliable. At the same time, the risk that China’s expanded exports will result in an “export of deflation” to the region is rising, likely worsening the business environment for manufacturing.

Although the U.S. has imposed high tariffs on India, the two countries continue trade negotiations. On the other hand, the Indian government has implemented measures to stimulate domestic demand, such as cuts to the Goods and Services Tax (GST). These measures are beginning to show signs of easing inflation and boosting private consumption. As a result, domestic demand is expected to support India’s economy in the short term. Inflation across Asian emerging economies has also stabilized, and central banks are increasingly pursuing monetary easing to underpin economic conditions, supporting domestic demand including private consumption. While uncertainty in external demand persists, Asian countries are expected to further accelerate efforts to bolster their economies through domestic-demand stimulus. Nonetheless, differences in each country’s economic structure will influence their respective economic outlooks.

Economic Growth Rates in China, India, NIES, and ASEAN5 Countries

Source: CEIC data. The light blue areas indicate our forecasts. For India, data are based on the fiscal year (From April to March).

Original in Japanese:

https://www.dlri.co.jp/report/macro/546323.html

Disclaimer:

This report has been prepared for general information purposes only and is not intended to solicit investment. It is based on information that, at the time of preparation, was deemed credible by Daiichi Life Research Institute, but it accepts no responsibility for its accuracy or completeness. Forecasts are subject to change without notice. In addition, the information provided may not always be consistent with the investment policies, etc. of Daiichi Life or its affiliates.