- Report Index

- Japan Economic Outlook (September 2025)

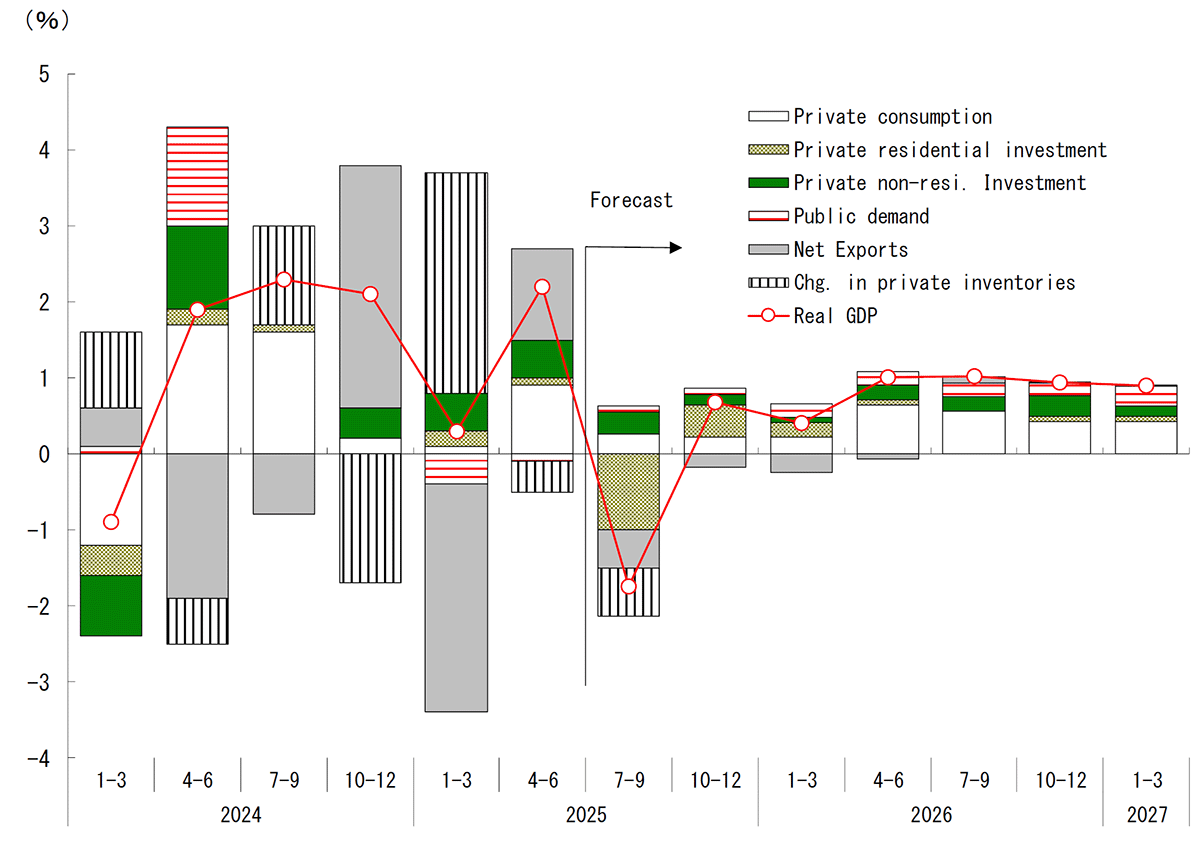

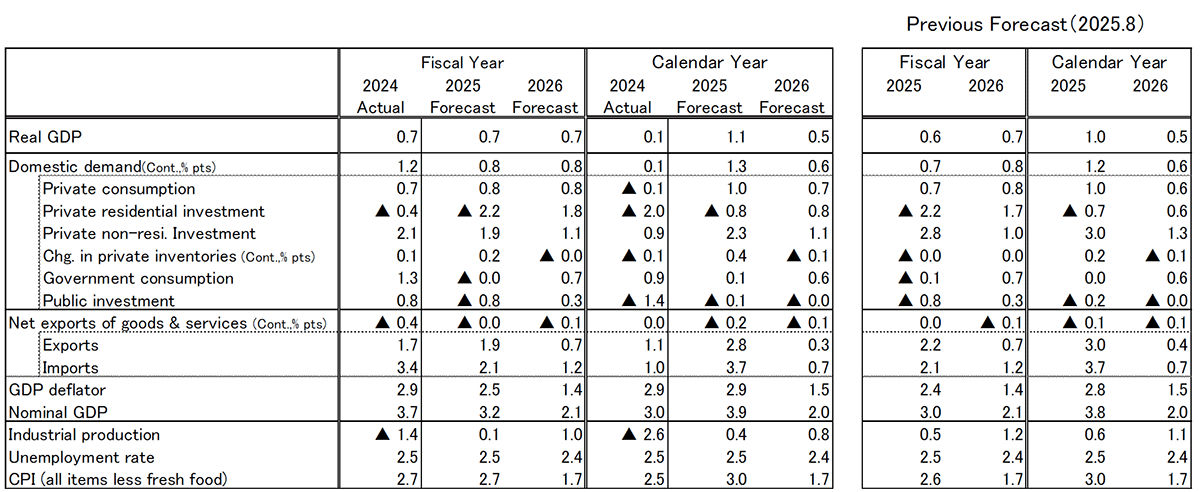

We now forecast real GDP growth of +0.7% in FY2025 (August forecast: +0.6%) and +0.7% in FY2026 (unchanged at +0.7%). On a calendar-year basis, the projections are +1.1% for 2025 (previously +1.0%) and +0.5% for 2026 (unchanged at +0.5%). The growth forecasts for both fiscal 2025 and calendar year 2025 have been slightly revised upward, mainly due to the upward revision of the April-June quarter growth rate in the second preliminary estimate.

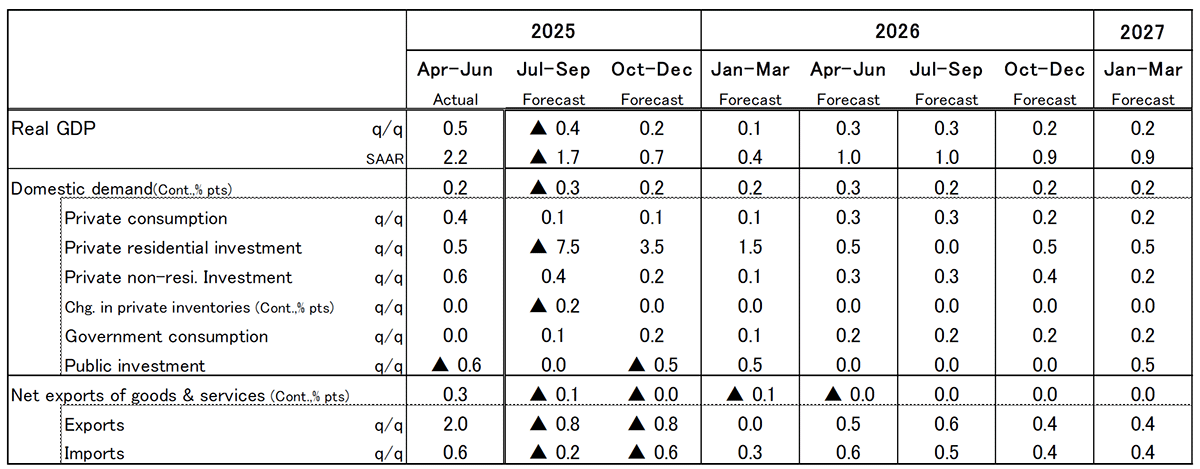

Japan's real GDP growth rate for the April-June quarter of 2025 posted a strong annualized gain of +2.2% from the previous quarter. This was supported by resilient exports and business investment, which had been considered vulnerable to the adverse effects of the Trump tariffs. First, the U.S. economy has proven more resilient than expected. Second, in automobile exports to the U.S., firms cut export prices sharply and avoided raising local retail prices, which helped prevent a drop in export volumes despite higher tariffs. Although there were concerns that greater uncertainty would lead firms to postpone capex, such restraint has so far been limited. No movements directly leading to a severe economic slump have been observed at this time.

However, the negative effects of the tariff hikes are highly likely to emerge going forward. Although the Japan-U.S. negotiations have resulted in a decision to lower the U.S. tariff rate, the imposition of a still-high 15% tariff remains unchanged, meaning the downward pressure on the Japanese economy will still be considerable. Until now, Japanese automakers appear to have kept local prices unchanged while awaiting a finalized tariff rate. With a broad agreement now in place, they are likely to revisit pricing and may move to raise prices. If so, U.S. sales volumes would fall, weighing on export volumes. Conversely, if manufacturers keep prices low to sustain U.S. sales, the hit to export volumes would be smaller, but profit margins would be squeezed, risking weaker domestic capex and wage restraint. In addition to softer exports, residential investment is expected to drop sharply as payback from front-loaded demand ahead of legal changes. As a result, the GDP growth rate for the July-September quarter is forecast to turn negative (with an annualized quarter-on-quarter rate of -1.7% expected).

Personal consumption in Japan is expected to remain broadly stagnant. Although personal consumption grew relatively strongly in the April-June quarter with a quarter-on-quarter increase of +0.4%, the sustainability of this momentum is questionable given the persistent high level of prices. With food prices still rising significantly, the timing for real wages to turn positive is likely to be delayed until the end of 2025, and household consumption is not expected to play a role in supporting economic growth. Against this backdrop, as the negative effects of tariff increases gradually materialize, the business sector is forecast to slow down, resulting in the Japanese economy in the latter half of 2025 remaining in a state of stagnation with intermittent progress and setbacks.

We expect a moderate pickup in FY2026. In the U.S., rate cuts are likely to resume in September 2025 amid slowing growth and a softer labor market, providing support to activity in 2026 with a lag. Tax cuts should also lift the U.S. economy. As U.S. growth stabilizes, Japan's exports are also expected to recover, helping to stem the deterioration in corporate earnings. At the 2026 spring wage negotiations, the pace of wage hikes is likely to slow versus 2025 due to weaker FY2025 earnings, but structural labor shortages should still support some wage gains. Alongside slower inflation, real wages are expected to trend moderately higher.

Forecast of Real GDP (Quarter-on-Quarter Annualized Rate, Contribution)

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office.

Japan's Economic Outlook(Yearly)

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office, Ministry of Economy, Trade and Industry, Ministry of Internal Affairs and Communications.

Japan's Economic Outlook(Quarterly)

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office.

Original in Japanese:

https://www.dlri.co.jp/report/macro/512516.html

Disclaimer:

This report has been prepared for general information purposes only and is not intended to solicit investment. It is based on information that, at the time of preparation, was deemed credible by Daiichi Life Research Institute, but it accepts no responsibility for its accuracy or completeness. Forecasts are subject to change without notice. In addition, the information provided may not always be consistent with the investment policies, etc. of Daiichi Life or its affiliates.