- Report Index

- World Economic Outlook (August 2025)

- Economic Trends

-

2025.8

World Economic Outlook (August 2025)

Yoshiki Shinke, Seiji Katsurahata, Osamu Tanaka, Toru Nishihama

1. Japan Economy

Current state of the economy: Adverse Effects of the Trump Tariffs Have Yet to Materialize

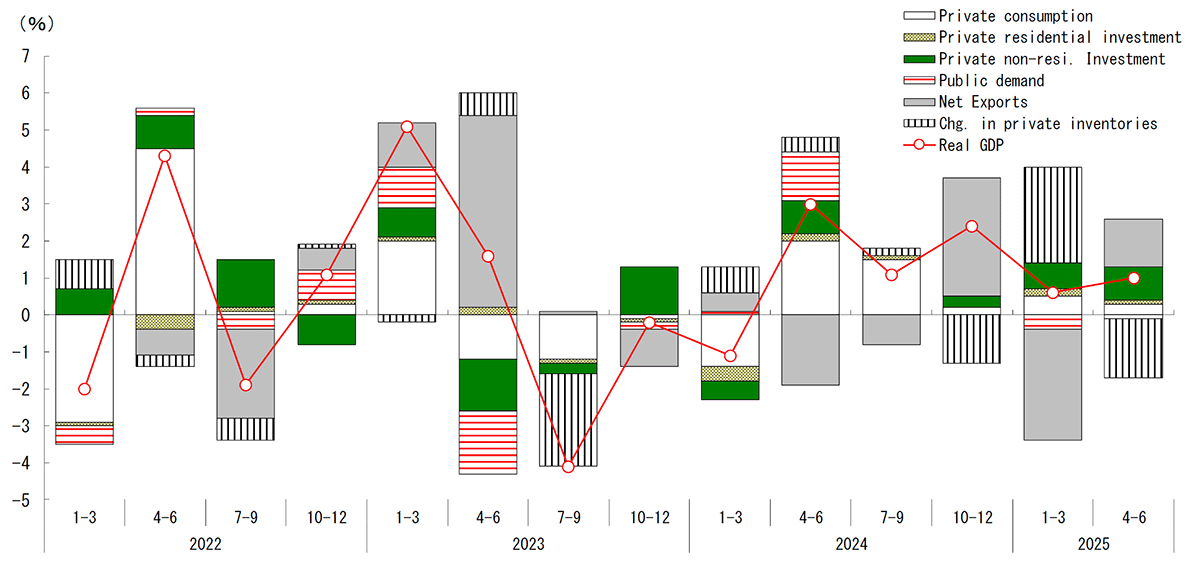

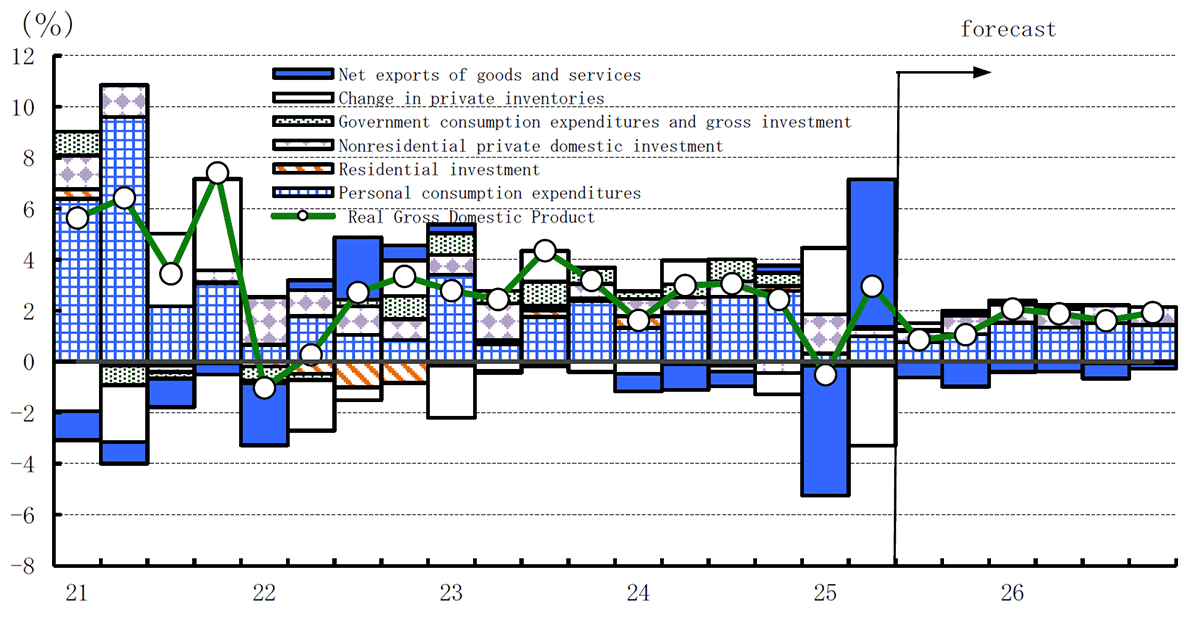

Real GDP(Quarter-on-Quarter Annualized Rate, Contribution)

Source: Cabinet Office.

Japan's real GDP grew at an annualized 1.0% quarter-on-quarter in the April-June quarter of 2025, marking a fifth consecutive quarter of expansion. The main contributors were exports and capital expenditure - both previously viewed as highly exposed to the so-called “Trump tariffs.”

Exports rose a robust 2.0% qoq, helped by an anticipated downturn in shipments to the United States failing to materialize. This resilience reflects not only the stronger-than-expected performance of the U.S. economy, but also a deliberate effort by Japanese automakers to limit tariff pass-through by cutting export prices to the U.S., which helped contain local retail price increases and stabilize volumes despite higher duties.

Despite heightened uncertainty and fears of a pullback, capital expenditure remained firm, rising 1.3% qoq. National accounts data indicate that caution has so far been limited. Solid corporate earnings, together with sustained spending on digitalization and automation, labor-saving equipment, and R&D, continue to underpin capex growth.

In sum, despite the implementation of higher U.S. tariffs, there are currently no clear, immediate signs of dynamics that would directly trigger an economic downturn. While the April announcement of the tariffs initially stoked fears of a sharp slowdown, a combination of tempered messaging from President Trump, the unexpectedly resilient U.S. economy, and Japanese firms' curbs on price pass-through has left Japan's domestic performance exceeding earlier projections.

Economic outlook: The effects of the Trump tariffs will become apparent going forward.

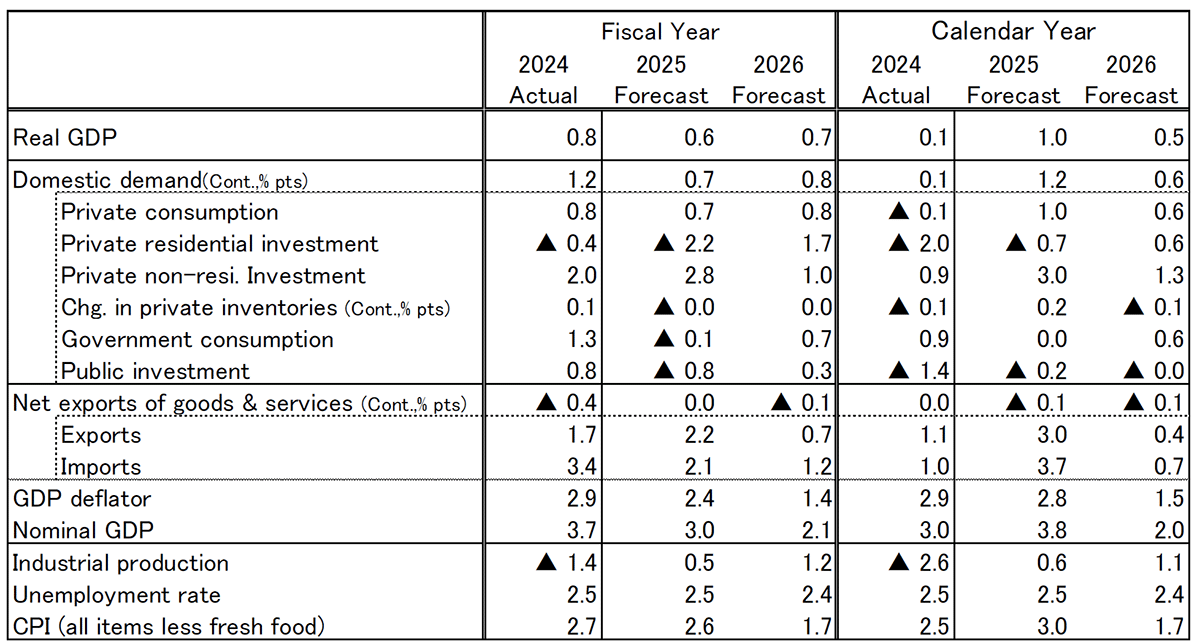

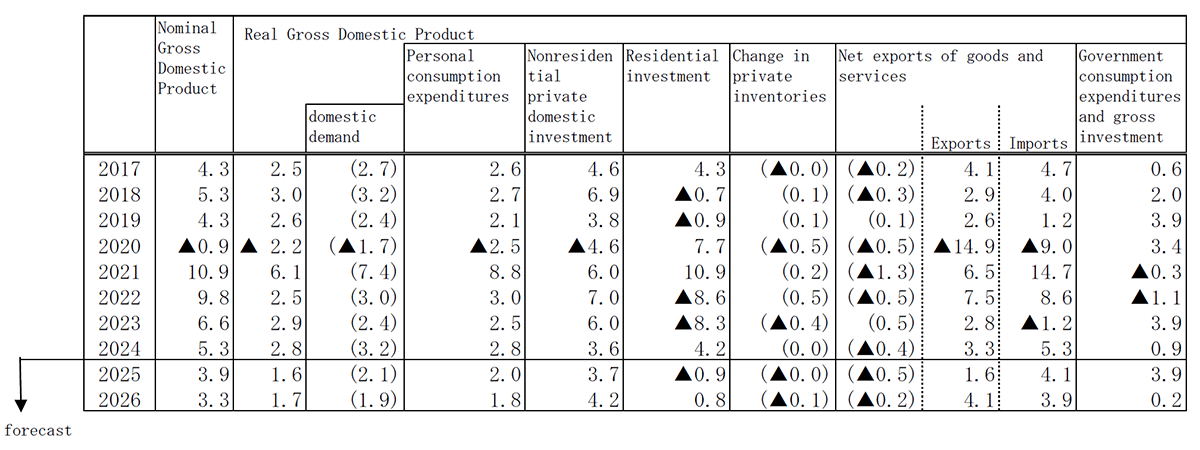

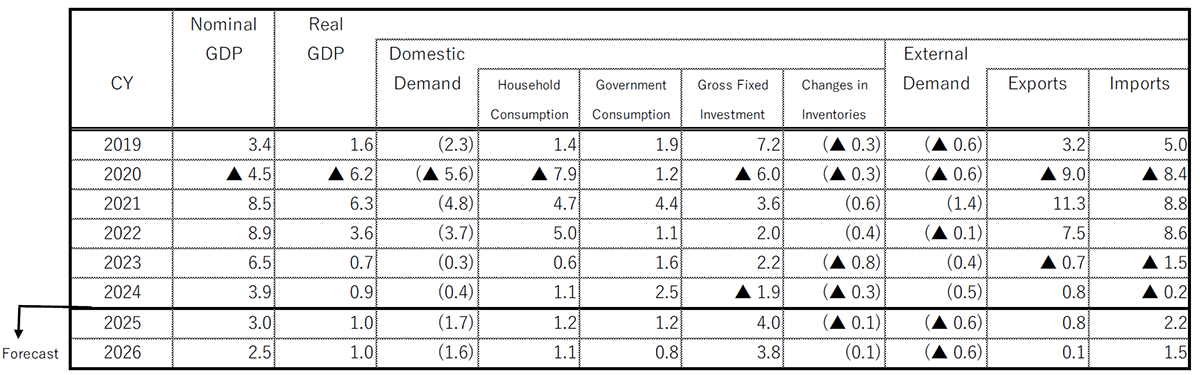

Japan's Economic Outlook(Yearly)

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office, Ministry of Economy, Trade and Industry,Ministry of Internal Affairs and Communications.

The adverse effects of the tariff hikes are, however, likely to surface more clearly ahead. Until now, Japanese automakers appear to have kept local prices unchanged while awaiting a finalized tariff rate. With a broad agreement now in place, they are likely to revisit pricing and may move to raise prices. If so, U.S. sales volumes would fall, weighing on export volumes. Conversely, if manufacturers keep prices low to sustain U.S. sales, the hit to export volumes would be smaller, but profit margins would be squeezed, risking weaker domestic capex and wage restraint. In addition to softer exports, residential investment is expected to drop sharply as payback from front-loaded demand ahead of legal changes. We therefore expect negative q/q growth in July-September.

Personal consumption is likely to remain subdued for the time being. With food prices surprising on the upside, disinflation is likely to proceed more slowly than expected in our previous forecast. As a result, the timing for real wage growth to turn positive is likely to be pushed back to late 2025. With consumption unlikely to provide much support, the negative effects of the tariff hikes should gradually become more apparent, leaving the economy in a stop-and-go pattern in the second half of 2025.

We expect a moderate pickup in FY2026. In the U.S., rate cuts are likely to resume in September 2025 amid slowing growth and a softer labor market, providing support to activity in 2026 with a lag. Tax cuts should also lift the U.S. economy. As U.S. growth stabilizes, Japan's exports are also expected to recover, helping to stem the deterioration in corporate earnings. At the 2026 spring wage negotiations, the pace of wage hikes is likely to slow versus 2025 due to weaker FY2025 earnings, but structural labor shortages should still support some wage gains. Alongside slower inflation, real wages are expected to trend moderately higher.

2. US Economy

Current state of the economy: Economic slowdown and labor market softening due to increasing uncertainty

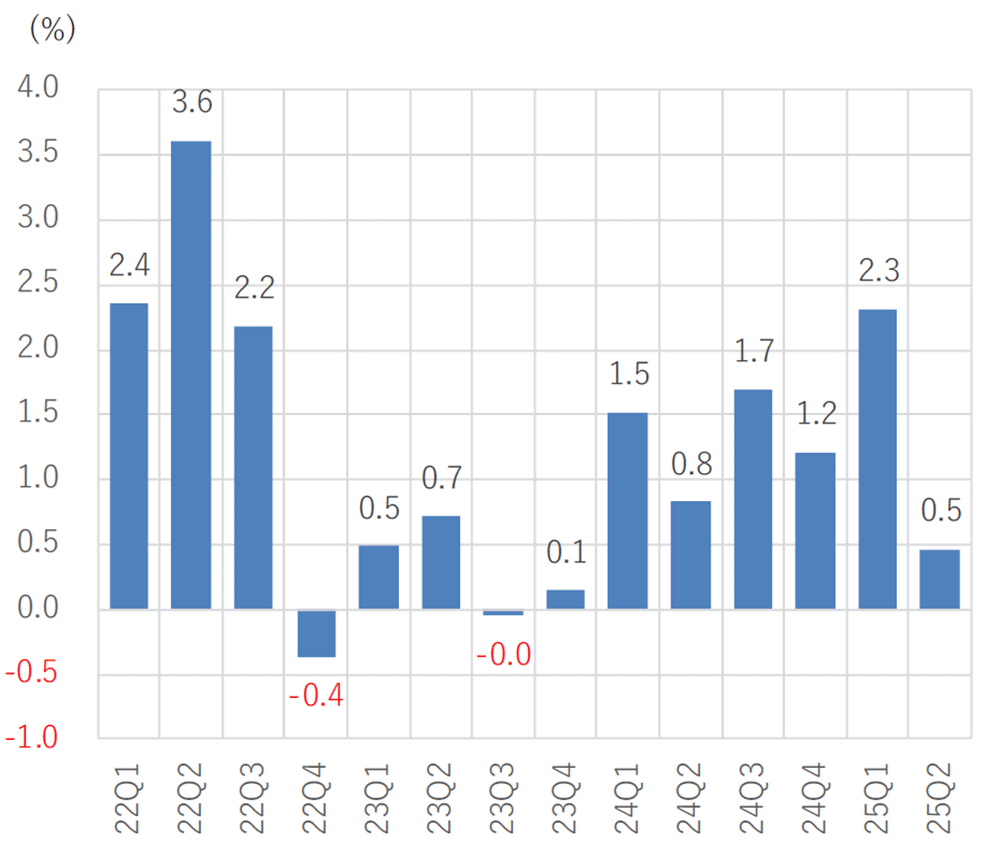

In the U.S., the economy is slowing, and the labor market is softening amid growing uncertainty over Trump 2.0 policies, while inflation is hesitant to fall. Real GDP growth (initial estimate) for 2Q 2025 was +3.0% annualized (-0.5% in 1Q 2025), demonstrating strong growth. However, the first half of 2025 saw significant fluctuations, with imports increasing sharply in 1Q 2025 due to Trump tariffs, followed by a sharp decline in 2Q 2025. Real GDP growth slowed to +1.2% annualized in the first half of the year, indicating an economic slowdown.

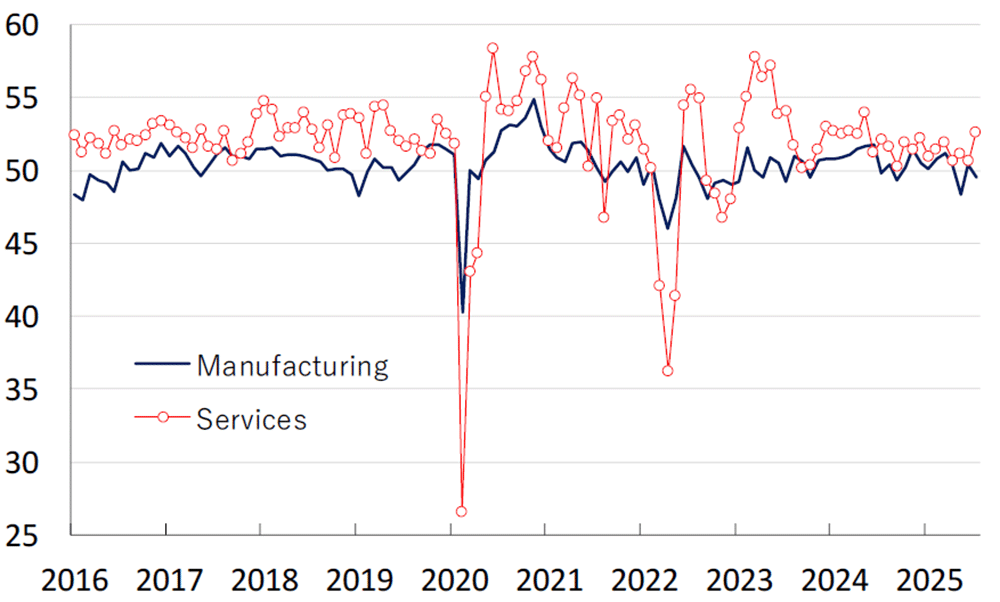

As for the economic outlook from the start of July, ISM Report on Business, which measures business sentiment, recorded a reading of 48.0 (49.0 in the previous month) for the manufacturing sector, remaining below the 50 mark, the dividing line between expansion and contraction, for the fifth consecutive month. Meanwhile, the non-manufacturing index rose to 50.1 (50.8 in the previous month), above the 50 mark, which separates expansion from contraction. Business activity Index remained stable at 52.6, indicating a gradual expansion of the non-manufacturing sector. Since the inauguration of Trump 2.0, the manufacturing sector has continued to contract, while the non-manufacturing sector has continued to expand, supporting U.S. economic growth.

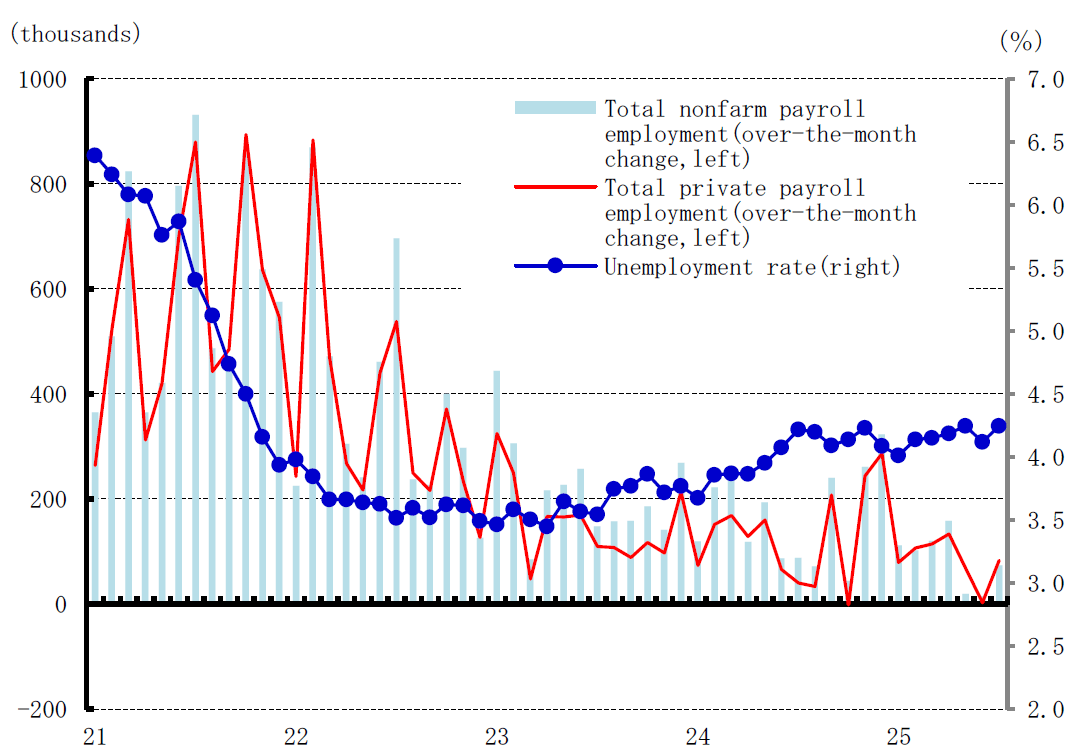

Meanwhile, in the labor market, non-farm payrolls increased by 73,000 from the previous month in July (up 14,000 from the previous month). While the government sector fell by 10,000 from the previous month (up 11,000 from the previous month), the private sector accelerated, increasing by 83,000 from the previous month (up 3,000). However, the number of nonfarm payroll employees for May and June was revised down significantly to a combined decrease of 258,000 (down 109,000 for state and local teachers and down 139,000 for the private sector), and the trend toward a gradual increase was affected by restrained hiring by companies and bad weather. Meanwhile, the unemployment rate in July was 4.2% (4.1% the previous month), gradually rising from the bottom of 3.4% in April 2023, but still remains at a low level. The labor market is generally considered to be softening gradually.

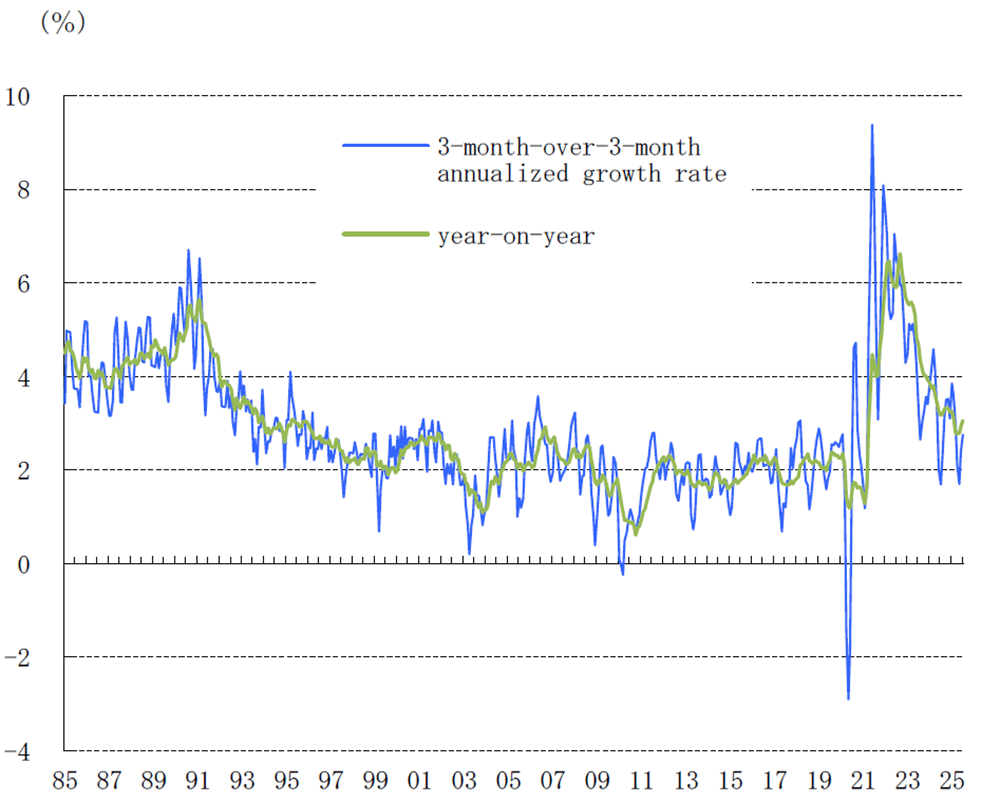

In terms of inflation, core CPI for July was up 2.8% annualized from three months earlier (up 2.4% the previous month), indicating a slight strengthening of short-term inflationary pressures, rising 3.1% year-on-year (up 2.9% the previous month). At the FOMC meeting held on July 29 and 30, 2025, the Federal Reserve Board (FRB) decided by a majority vote to keep its policy interest rate unchanged for the fifth consecutive meeting and maintain the federal funds rate target range at 4.25% to 4.50%. The board also decided to continue its balance sheet reduction measures. Regarding the decision to keep the policy interest rate unchanged, FRB Governor Waller and FRB Vice Chairman Bowman both voted against, believing a 25 basis point rate cut would be appropriate. This is the first time in approximately 32 years, since December 1993, that multiple FRB Governors have voted against a decision. FRB Chairman Powell explained the background to the decision to keep the policy interest rate unchanged, saying, "The majority of meeting participants judged that it was appropriate to maintain a moderate monetary tightening policy, given that inflation is exceeding the Fed's target."

US labor situation

Source: US Department of Labor

US core CPI

Source: US Department of Labor

Economic Outlook: US economy will slow down, but a recession will be avoided

In the Trump 2.0 tariff policy, in February, a 25% tariff was imposed on certain imports from Canada and Mexico, and a 10% tariff was imposed on imports from China. In March, an additional 10% tariff was imposed on China (totaling 20%), and a 25% tariff was imposed on steel and aluminum imports. In April, a 10% reciprocal tariff and a 25% tariff on automobile imports were imposed, and an additional 125% tariff was imposed on imports from China. In May, a 25% tariff on auto parts was imposed. In June, steel and aluminum import tariffs were raised to 50%. In August, a 50% copper tariff was imposed, and additional reciprocal tariffs began on the 7th.

In trade negotiations, the United States and the United Kingdom reached a trade agreement in May that included tariff reductions and increased imports, while the United States and China also agreed to a 115% tariff reduction and a 90-day suspension of the 24% reciprocal tariff surcharge until August 12th. In July, trade agreements were reached with Vietnam, Indonesia, the Philippines, Japan, the EU, and South Korea. These agreements allowed the United States to curb tariff surcharges, while allowing the other countries to unilaterally benefit from the agreement by eliminating tariffs on imported products from the United States, increasing imports of agricultural products, energy, aircraft, and other products from the United States, and increasing investment in the United States. Uncertainty is gradually easing following an agreement in August between the United States and China to again suspend reciprocal tariff surcharges and export restrictions on rare earths and other products for 90 days (until November 10th). While there is a strong possibility that negotiations between the US and China will not progress and a 24% tariff will be imposed, the delay in the timing and the possibility of indirect exports via countries that have avoided the significant additional tariffs will likely prevent abnormal price hikes and supply disruptions. However, there is a risk of tariff increases if the Trump administration determines that countries and regions are not fully implementing trade agreements, in addition to plans to impose tariffs on pharmaceuticals, semiconductors, and timber.

In the second half of the year, we can expect an expansion in capital investment and an increase in exports of agricultural products and energy, backed by the easing of uncertainty due to trade agreements. However, the rise in real interest rates and rising prices are likely to act as a restraint on economic activity. While increases in personal consumption, such as stocks and real estate, will likely boost growth, slowing employment and income growth and rising prices will likely result in the US economy slowing to growth below its potential. Inflation is likely to rise gradually as the impact of tariffs gradually becomes apparent. In this environment, the Federal Reserve is expected to implement interest rate cuts of 25 basis points at each of its September and December FOMC meetings to avoid a further economic slowdown and labor market softening. However, if the labor market worsens, such as with a significant rise in the unemployment rate, the rate cuts will likely be larger.

US economic outlook (YoY、%)

Source: US Department of Commerce, Our forecast

Note: Contribution is in parentheses

U. S. real GDP growth (SAAR)

Source: US Department of Commerce. Forecast is our own.

3. Eurozone Economy

Current state of the economy: Fiscal turnaround raises expectations of recovery

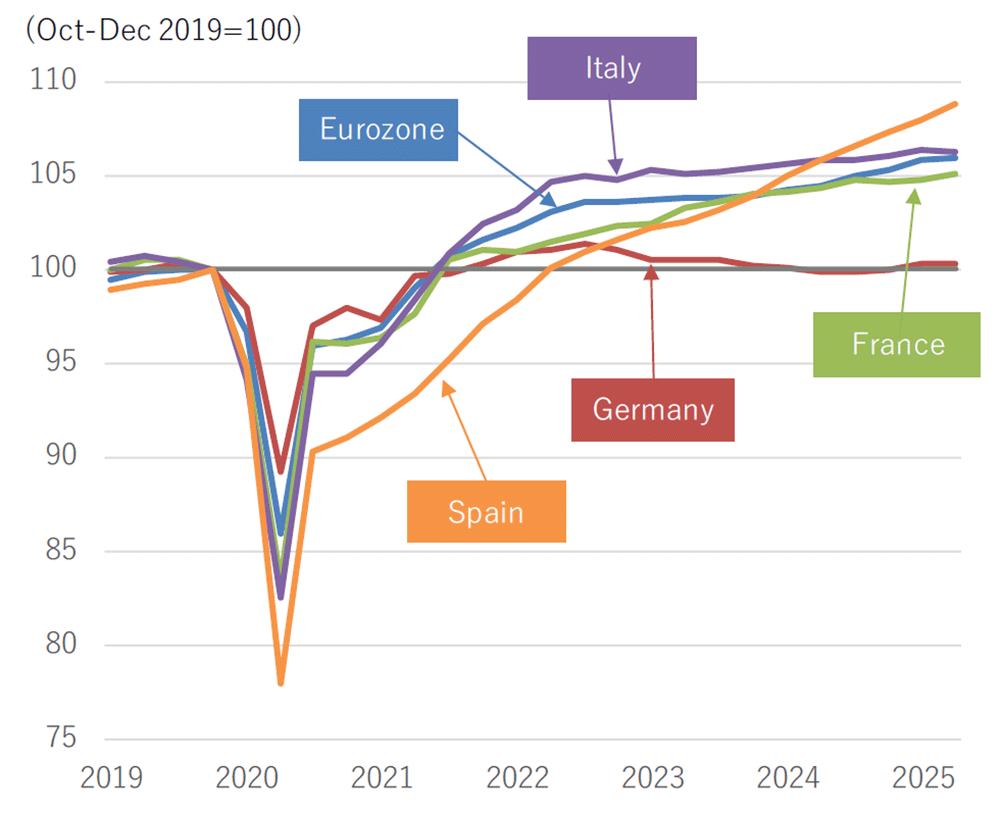

Over the past few years, the Eurozone economy has been sluggish, with core countries such as Germany and France dragging down growth despite steady economic expansion in southern European countries such as Spain and Italy. Spain continues to enjoy high growth thanks to population growth due to immigration and an increase in foreign tourists. Italy's economic recovery is being supported by funding from the European Recovery Fund. Germany's economic stagnation is due to the high energy prices resulting from the cessation of imports of Russian energy resources, which has led to a loss of export competitiveness, as well as the long-standing restrictive fiscal policies that have become a hindrance. In France, fiscal uncertainty and political risks are weighing on economic activity.

In the January-March quarter, the eurozone economy outperformed expectations due to a surge in exports ahead of the US tariff hike and Ireland's high growth, which was driven by the economic activities of multinational companies. Although the economy slowed down in the April-June period as a reaction to this, it managed to maintain positive growth. Until now, uncertainty surrounding tariff negotiations has been a drag on economic activity, but the United States and the European Union (EU) reached a broad agreement on tariff rates and other issues at the end of July. The United States will impose a flat 15% tariff on imports from the EU, including its mainstays of automobiles and pharmaceuticals, while the United States and the EU will mutually eliminate tariffs on items such as aircraft and certain pharmaceuticals. The EU has also committed to expanding imports of U.S. energy and military equipment and increasing investment in the United States. While punitive high tariffs and retaliatory measures have been avoided, the impact on European exporters is unavoidable.

Meanwhile, Germany amended its constitutional provision requiring fiscal balance (debt brake) and shifted to a significant expansion of spending on infrastructure and defense. The EU also decided to temporarily suspend fiscal discipline for member states and provide fiscal support to rebuild the defense capabilities of European countries and strengthen support for Ukraine. Expectations for economic recovery are rising due to these changes in fiscal management.

In response to the easing of inflationary pressures, the European Central Bank (ECB) has continued to cut interest rates since June last year. The lower limit of the policy interest rate (deposit facility rate) is currently 2%, reaching the level of the ECB's neutral interest rate (the policy interest rate that neither overheats nor suppresses the economy). The ECB decided not to cut rates further in July in order to assess the effects of previous rate cuts and the outcome of tariff negotiations.

Eurozone Real GDP Growth (annualised QoQ)

Source: Eurostat, Dai-ichi Life Research Institute

Real GDP in Major Eurozone Countries

Source: Eurostat, Dai-ichi Life Research Institute

Economic outlook: Quick return to recovery track after tariff shocks

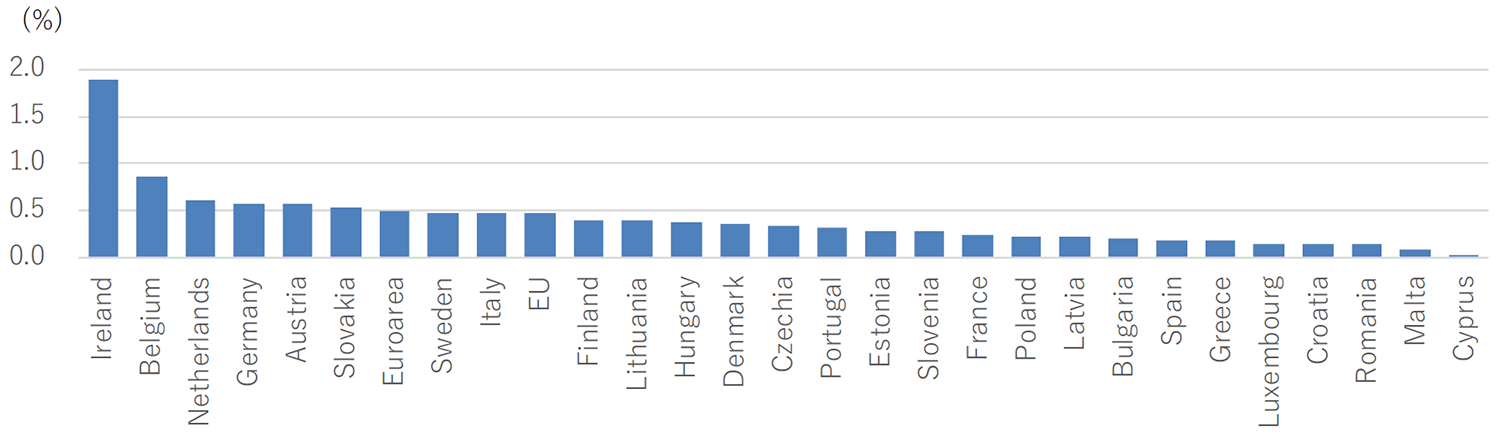

The US tariff increases will weigh on the economies of Ireland, Belgium, the Netherlands, Germany, and other countries that are highly dependent on exports to the US. However, uncertainty surrounding tariff negotiations will recede, allowing postponed economic activity to resume. With high tariffs on key exports such as automobiles and pharmaceuticals avoided, a severe economic downturn is likely to be averted. While a downturn in the July-September quarter is unavoidable due to the backlash from pre-tariff hike rush exports and the actual tariff increases, the eurozone economy is expected to return to a recovery trajectory thereafter, supported by improvements in household real purchasing power from inflation stabilisation and accelerated wage increases, the full effects of previous monetary easing measures, and shifts in fiscal policy.

The catalysts for economic recovery will be Germany's fiscal policy shift and increased defense spending across Europe. The fact that Germany, which has previously adhered strictly to austerity measures, now has fiscal leeway marks a major turning point in fiscal management. Some of this will be incorporated into this year's supplementary budget, and growth is expected to be confirmed by the end of the year. While the multiplier effect of increased defense spending is limited, and there is a risk that rising long-term interest rates due to concerns about fiscal deterioration will suppress private sector demand (crowding out), the overall effect on economic recovery is expected to outweigh these factors.

The annual growth rate for the eurozone in 2025 is expected to remain at +1.0% due to the impact of tariff increases. In 2026, fiscal spending expansion will support an acceleration in quarterly growth, but the low growth in the second half of 2025 will lower the starting point for 2026, keeping the annual growth rate at +1.0%, the same as the previous year.

Tariff Burden on EU Member States from US Tariff Increases (as a % of GDP, 2024)

Source: Eurostat, Dai-ichi Life Research Institute

Outlook of the Euroarea Economy (YoY, %)

Note: Figures in brackets are contributions to real GDP growth.

Source: Dai-ichi Life Research Institute

4. China and Emerging Asian Economies

Current state of economy– U.S.-China relations have passed their worst point, on the other hand, “rush demand" is supporting exports in many countries.

In the Chinese economy, the tariff policy of the U.S. Trump administration was explicitly aimed at China, raising concerns over its adverse effects. Following the U.S. imposition of reciprocal tariffs in April, China retaliated, which subsequently escalated into a trade war, in which both sides imposed high tariffs on each other. However, after subsequent negotiations, the U.S. and China agreed to withdraw retaliatory tariffs, suspend the imposition of additional tariffs and export restrictions, and continue dialogue. As a result, at present, Chinese exports to the United States remain subject to a combined 30% tariff - 20% in additional tariffs aimed at addressing fentanyl-related concerns, along with the 10% reciprocal tariff. Consequently, while U.S.-China relations are seen as having passed their worst phase, Chinese exports to the U.S. continue to decline significantly under the weight of the Trump tariffs.

Meanwhile, at the National People's Congress, the Chinese authorities, mindful of the deterioration in U.S.-China relations, indicated a policy shift toward expanding exports to countries and regions other than the U.S.. Supported by measures practically RMB depreciation through the currency basket (CFETS RMB index), China's exports have remained resilient. In addition, since the latter half of last year, the government has strengthened policy support aimed at stimulating domestic demand, which, combined with the export performance, has resulted in an economic growth rate of +5.3% in the first half of this year—exceeding the government's target of “around 5%” set at the National People's Congress.

The U.S. indicated its intention to impose uniformly high reciprocal tariffs on emerging Asian economies that had benefited from the "fish in the troubled water" of expanding exports to the U.S. amid the recent years of U.S.-China friction. U.S. initially imposed reciprocal tariffs, but soon after decided to maintain the uniform portion (10%) while postponing the implementation of the additional tariffs and conducting bilateral negotiations. As a result, in the first half of this year, a surge in last-minute shipments ahead of the full enforcement of the Trump tariffs has boosted exports.

In addition, in recent years, emerging Asian economies have faced food inflation caused by high commodity prices and abnormal weather, but more recently, prices have shown signs of stabilizing. In the financial markets as well, the depreciation of various currencies against the stronger U.S. dollar has been a factor hindering monetary easing. However, growing uncertainty surrounding the Trump administration's policy management has encouraged a weaker U.S. dollar, the hurdle for monetary easing has been lowered for central banks across the region.

Although these developments have improved the environment for private consumption, uncertainty surrounding the Trump tariffs continues to weigh on capital investment and labor markets, leaving domestic demand - including household consumption - lacking in momentum in many countries. Therefore, it can be assessed that in the first half of this year, the economies of emerging Asian countries, particularly those structurally dependent on external demand, have been supported primarily by the last-minute surge in exports ahead of the full-scale implementation of the Trump tariffs.

S&P China Mfg. and Services PMI

Source: S&P Global

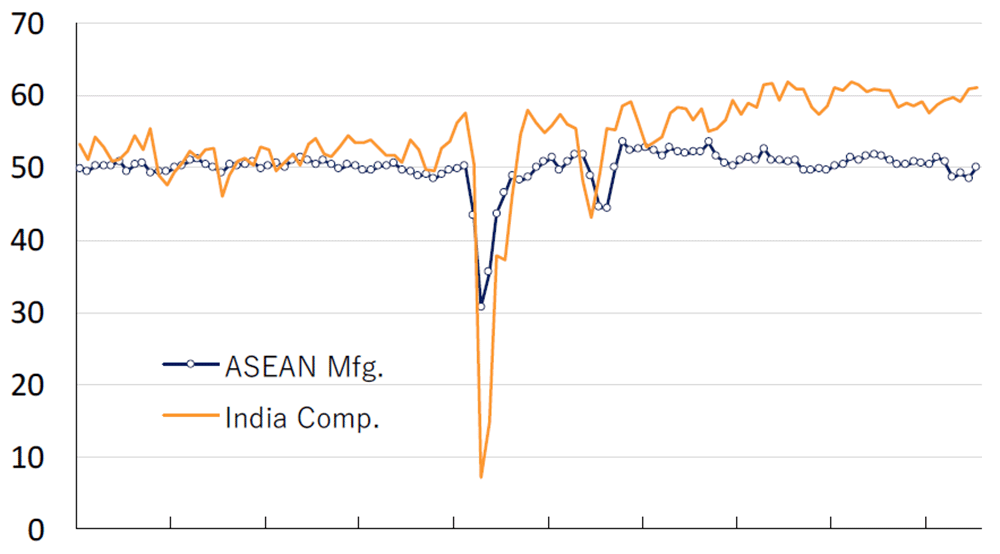

S&P India Comp. PMI and ASEAN Mfg. PMI

Source: S&P Global

Economic Outlook: Concerns remain over the spillover effects of the Trump tariffs, but domestic demand could potentially support economic activity.

Regarding the outlook for the Chinese economy, the U.S. has once again postponed the implementation of the additional reciprocal tariffs for 90 days, thereby avoiding a scenario in which the environment surrounding exports to the U.S. would further deteriorate until as late as mid-November. This is expected to gradually mitigate the adverse effects of the Trump tariffs. On the other hand, while the recent moves to practically RMB depreciation have temporarily eased, the BRICS countries - viewed as emerging market leaders - have strengthened their cohesion in response to U.S. tariff policies, and other emerging economies are showing signs of aligning with BRICS. Furthermore, China itself has been actively deepening relations with emerging countries in Asia, Latin America, and Africa as alternative export destinations, which is expected to help offset declines in exports to the U.S. through expanded trade with countries outside the U.S..

Meanwhile, since the latter half of last year, Chinese authorities have supported domestic demand by promoting replacement of durable consumer goods and investment in equipment through subsidy policies, which has bolstered domestic demand in the first half of the year. However, going forward, there is concern that demand front-loading may weigh on domestic demand. Structural issues that currently suppress domestic demand, such as the real estate downturn and employment insecurity among younger generations, have not been fundamentally addressed, and downward pressure on domestic demand is likely to persist. Nevertheless, economic growth in the first half of the year exceeded government targets, and with supply-side strength supported by excess production capacity, the economy has remained resilient, suggesting that the full-year growth target of around 5% is likely to be achieved.

The U.S. has agreed to set reciprocal tariff rates for emerging Asian economies at around 20%, which is expected to mitigate some of the initially feared adverse effects. However, the U.S. appears to have reached an agreement with some Asian countries to impose additional tariffs on goods exported to the U.S., with China's rerouted exports in mind. For countries that have significantly expanded their exports to the U.S. against the backdrop of intensifying U.S.-China trade friction, this development could signal a potential shift in that trend. Additionally, the U.S. has indicated plans to impose additional tariffs on India due to imports of Russian crude oil. Although India's economy is relatively less export-dependent, any such tariffs would inevitably exert some downward pressure on growth.

Meanwhile, inflation in emerging Asian countries has stabilized, and central banks are stepping up monetary easing to support economic activity amid concerns that the Trump tariffs could suppress external demand. This is expected to support domestic demand, including private consumption and private investment. In addition, India's Modi administration has also indicated plans to support the economy through fiscal measures such as lowering the Goods and Services Tax (GST) from October. Therefore, while there remains a risk that global trade contraction triggered by the Trump tariffs could weigh on emerging market economies, domestic demand is expected to help support overall economic activity.

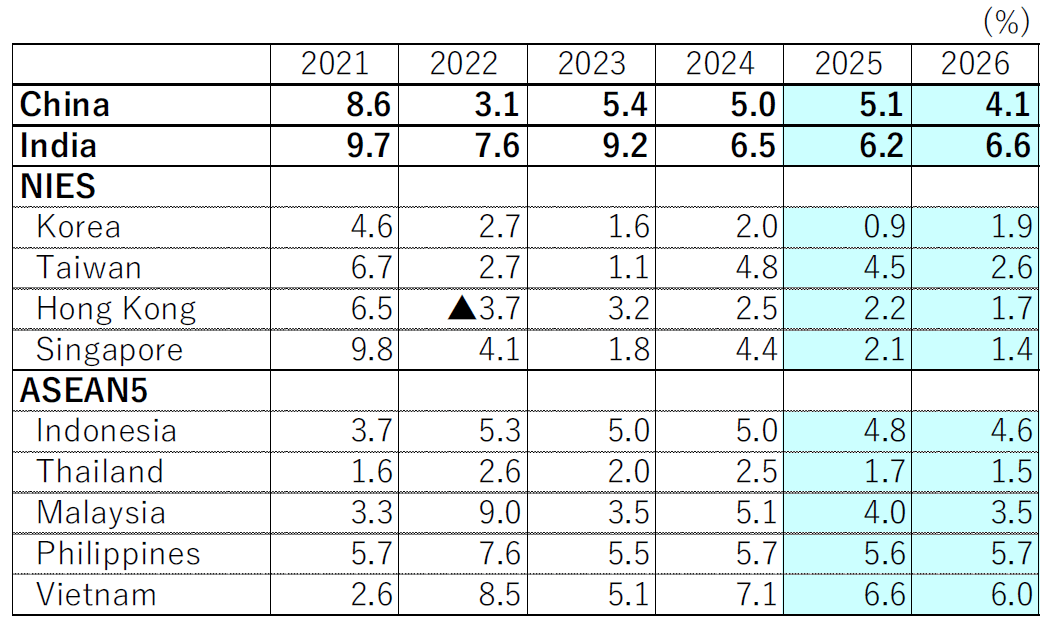

Economic Growth Rates in China, India, NIES, and ASEAN5 Countries

Source: CEIC data. The light blue areas indicate our forecasts. For India, data are based on the fiscal year (From April to March).

Original in Japanese

Disclaimer:

This report has been prepared for general information purposes only and is not intended to solicit investment. It is based on information that, at the time of preparation, was deemed credible by Daiichi Life Research Institute, but it accepts no responsibility for its accuracy or completeness. Forecasts are subject to change without notice. In addition, the information provided may not always be consistent with the investment policies, etc. of Daiichi Life or its affiliates.