- Report Index

- TISFD: Where Social Risk Disclosure Meets Corporate Value

- DLRI Report

-

2025.8

TISFD: Where Social Risk Disclosure Meets Corporate Value

Kaori Shiraishi

Beyond E: Expanding the ESG Focus to Social Disclosure

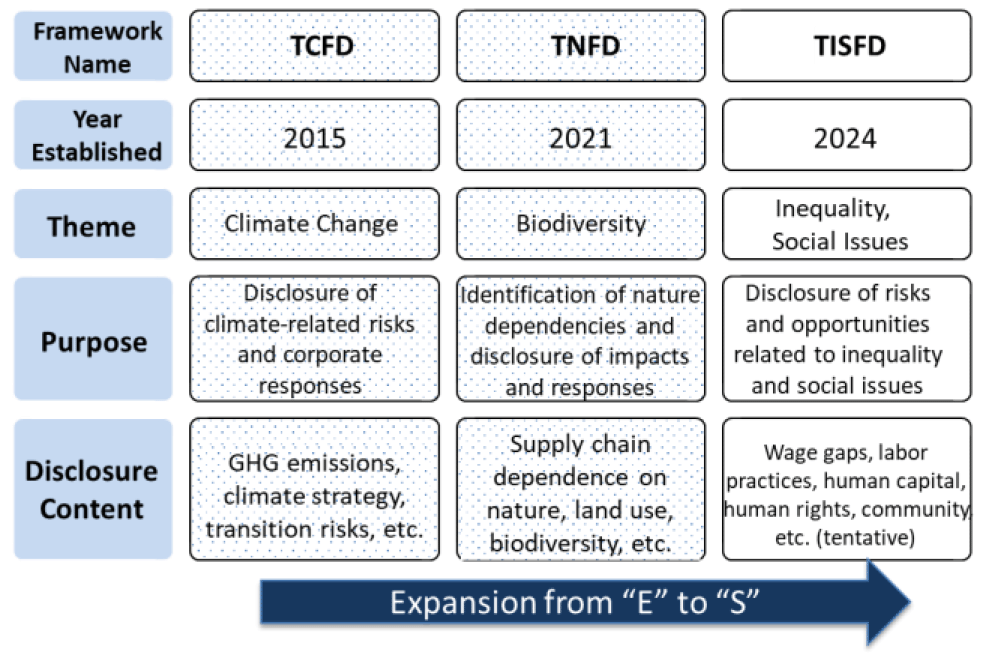

Non-financial disclosures are undergoing a pivotal transformation. While international standards have historically prioritized environmental issues -anchored by frameworks such as the TCFD (Taskforce on Climate-related Financial Disclosure)

and TNFD (Taskforce on Nature-related Financial Disclosure)— recent years have seen a notable expansion of focus from environmental ("E") to social ("S") dimensions within ESG (Figure 1).

Figure 1. ESG Expansion: from "E" to "S"

Source: Compiled by Dai-ichi Life Research Institute based on various sources

Figure 1. ESG Expansion: from "E" to "S"

Source: Compiled by Dai-ichi Life Research Institute based on various sources

A key milestone in this shift is the launch of the Taskforce on Inequality and Social- related Financial Disclosures (TISFD) in September 2024. Established in collaboration with the OECD (Organisation for Economic Co-operation and Development), UNDP(United Nations Development Programme), and other global institutions, the TISFD introduces a comprehensive framework for companies and financial institutions to assess and disclose their impacts, dependencies, risks, and opportunities related to people.

The scope of the TISFD encompasses the impact on employees, workers, communities and consumers. These impacts frequently manifest as issues related to labor conditions and human rights, which can escalate into significant corporate social risks-such as wage disparities, discrimination, or rights violations.

While these risks were traditionally considered part of corporate social responsibility or philanthropic efforts, they are now increasingly recognized as material business risks with direct implications for long-term corporate value and operational continuity. In this evolving landscape, "people-centered sustainability" is emerging as a core element of corporate management.

Why Are Social Risks Gaining Prominence Now?

The launch of the TISFD reflects a growing global consensus that social risks are fundamental challenges to corporate management. Three key developments help explain this shift:

1. The Pandemic Exposed Deep-rooted Social Inequalities

The disproportionate burden borne by essential workers, harsh labor conditions at the end of global supply chains, and the vulnerability of precarious workers brought the intersection of business, human rights, and labor practices into the global spotlight.

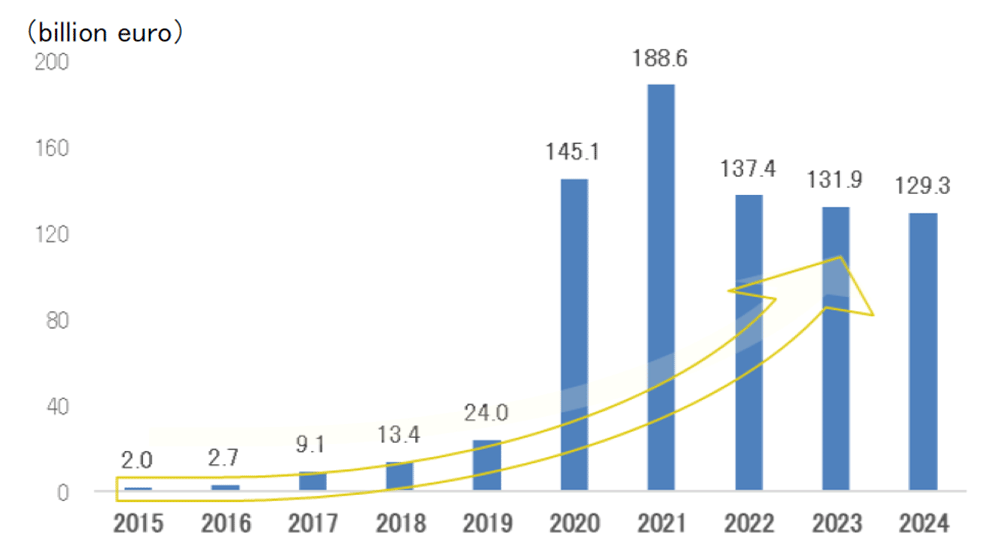

In response, investor interest in social issues surged. This shift is evident in the dramatic rise in social bond issuance between 2019 and 2020, as shown in Figure 2.

Figure 2. Social Bond Issuance Trends (2015-2024)

Source: Compiled by Dai-ichi Life Research Institute based on the Luxembourg Stock Exchange "LGX Datahub"

Figure 2. Social Bond Issuance Trends (2015-2024)

Source: Compiled by Dai-ichi Life Research Institute based on the Luxembourg Stock Exchange "LGX Datahub"

2. Evolving Investor Expectations Amid ESG-Driven Strategies

While environmental factors have historically dominated ESG considerations, some investors are increasingly recognizing that social factors -such as gender equity, labor rights, and workplace practices-can impact a company's financial performance and long-term valuation.

As Figure 2 shows, social bond issuance surged in 2020 and has remained at elevated levels since then, signaling that social risks are becoming firmly established as a key theme in capital markets.

3. Strengthening Legal Obligations Related to Human Rights

The EU's Corporate Sustainability Due Diligence Directive (CSDDD), which came into effect in 2024, mandates that companies identify, prevent, and mitigate human rights abuses throughout their entire supply chains.

In this context, the TISFD is not merely another disclosure framework, but a manifestation of the broader shift in how corporate value is understood and evaluated.

What the TISFD Expects from Companies

The TISFD aims to establish a global standard for visualizing companies' and financial institutions' impacts, dependencies, risks, and opportunities related to people. Its 2024 paper, "People in Scope", warns that "extreme levels of inequality pose a significant risk to market actors, as they can cause the breakdown of social cohesion, slow down the growth of human capital, and endanger financial stability."

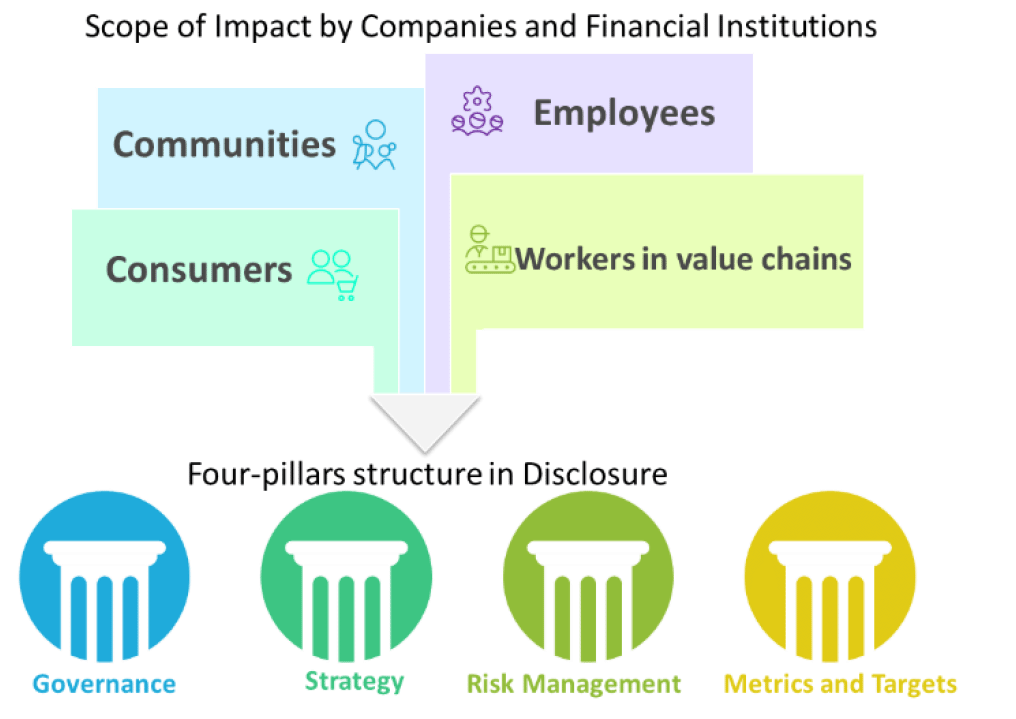

A distinguishing feature of the TISFD is its broad definition of "people" impacted by corporate activities, extending beyond employees to include workers in value chain, communities, and consumers (Figure 3). This is a significant departure from traditional human capital disclosure, which has primarily focused on employees.

TISFD-aligned disclosures are expected to follow the four-pillar structure used in the TCFD and TNFD frameworks: Governance, Strategy, Risk Management, and Metrics & Targets.

Among the four pillars, Metrics & Targets is expected to play an increasingly central role. Indicators such as gender pay gaps and human rights due diligence are likely to become critical metrics for evaluating corporate value.

Figure 3. Scope of Impact and 4 Pillars in Disclosure

Source: Compiled by Dai-ichi Life Research Institute using Napkin AI, based on TISFD "People in Scope" (2024) and "Proposed Technical Scope" (2025)

Figure 3. Scope of Impact and 4 Pillars in Disclosure

Source: Compiled by Dai-ichi Life Research Institute using Napkin AI, based on TISFD "People in Scope" (2024) and "Proposed Technical Scope" (2025)

TISFD as a New Benchmark for Corporate Value

The TISFD framework is scheduled to release a beta version by the end of 2025 and a final version by the end of 2026. As with the TCFD and TNFD, companies that take early action are likely to gain advantages in terms of disclosure credibility and enhanced corporate value.

As an initial step, companies should begin by identifying and visualizing their social risks, clearly articulating how their business activities impact various stakeholders. At the same time, they should proactively establish systems to gather and manage data on key indicators -such as gender pay disparities and the status of human rights due diligence -in preparation for potential future mandatory disclosures.

In today's corporate landscape, financial metrics alone are no longer sufficient to capture a company's true value. The quality of a company's relationships with "people"-its employees, workers in value chain, communities, and consumers-is becoming a core determinant of sustainable growth. The TISFD provides a new benchmark to help companies measure, manage, and communicate these people-centered values to society.

Ultimately, what matters most is the mindset of corporate leadership: whether the TISFD is regarded merely as a compliance burden or embraced as a strategic investment in long-term, people-driven value creation. This mindset will likely shape a company's future competitiveness and sustainability.

Original in Japanese:

https://www.dlri.co.jp/report/dlri/499607.html

Disclaimer:

This report has been prepared for general information purposes only and is not intended to solicit investment. It is based on information that, at the time of preparation, was deemed credible by Daiichi Life Research Institute, but it accepts no responsibility for its accuracy or completeness.