- Report Index

- Japan Economic Outlook (December 2024)

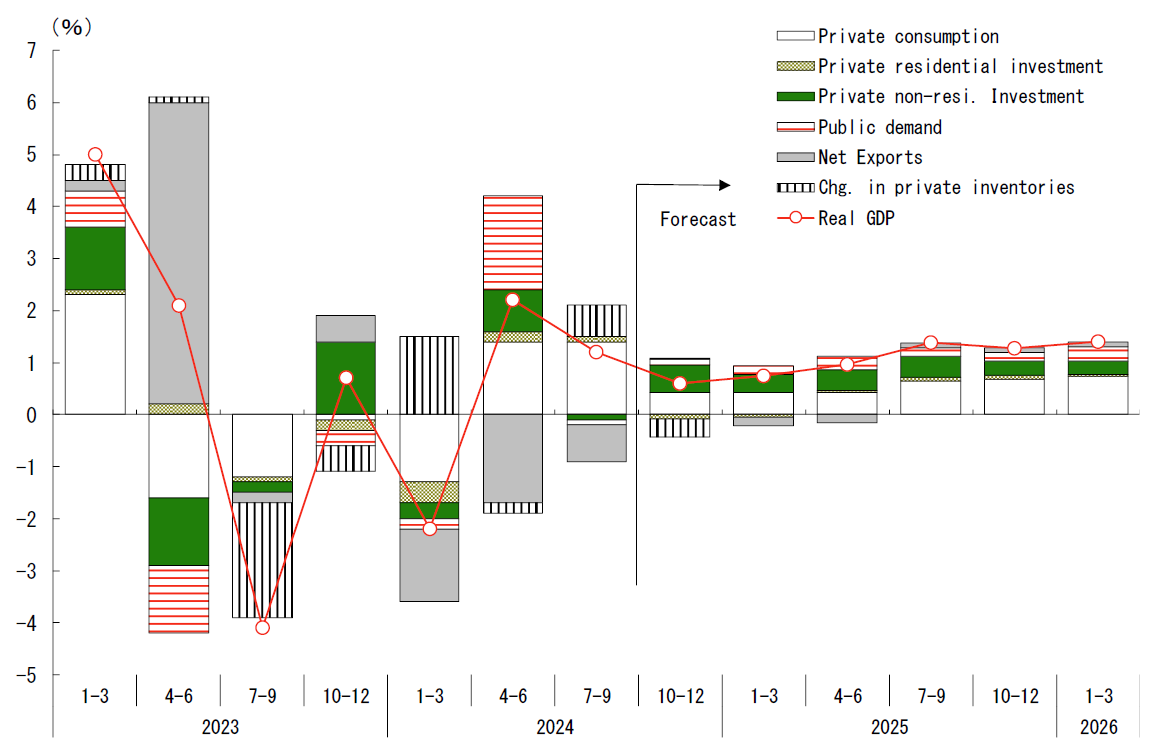

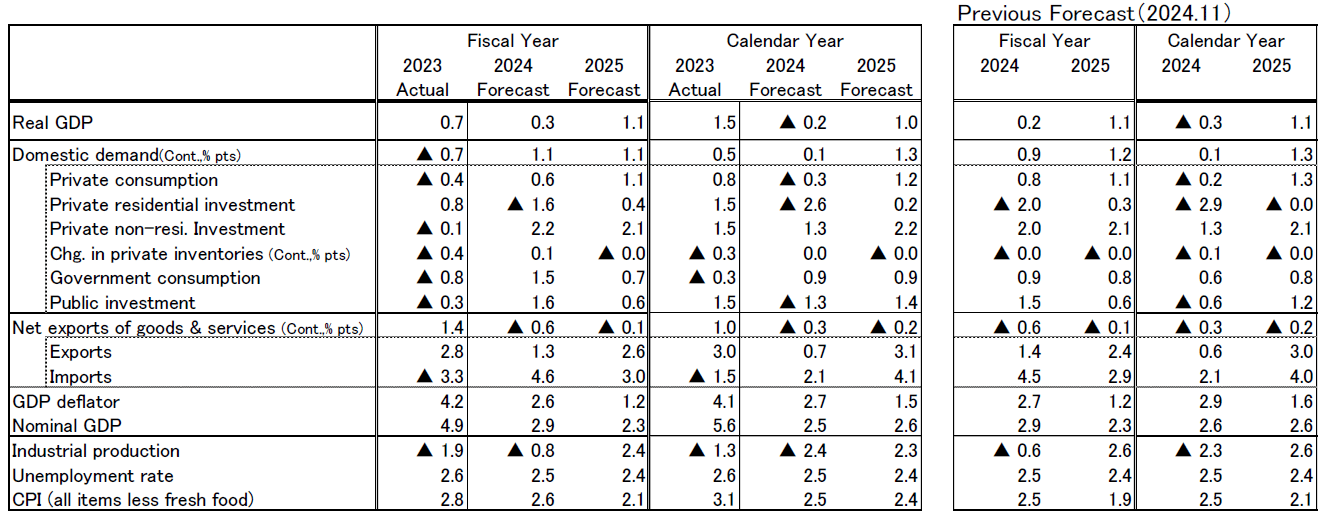

We expect the Japanese real economy to grow at +0.3% YoY in FY2024, +1.1% in FY2025. On a calendar-year basis, real GDP growth is projected to be -0.2% in 2024, +1.0% in 2025. The forecast for fiscal year 2024 has been slightly revised upwards, but this is due to revisions of past figures and does not indicate a change in the outlook going forward.

The real GDP growth rate for 3Q 2024 was up by +1.2% q/q annualized. The growth was driven by a substantial increase in private consumption, but this high increase is not sustainable, as it is largely due to the impact of the tax cuts implemented mainly in June and July, which boosted disposable income significantly. In addition, net exports and business fixed investment have declined. Although the economy is picking up, the recovery is moderate only.

The economy is expected to pick up in the second half of FY2024, but the pace of recovery is likely to remain moderate. A positive sign is that real wages are beginning to stabilize, which should gradually improve household income conditions.

However, the suppression of real purchasing power due to rising prices will continue to constrain consumption. In addition, consumer sentiment remains stagnant and given that real wages have declined for over two years, resulting in lower wage levels, a significant portion of the increase in income may go into savings. The extent of consumption recovery is expected to be limited in the near term, partly due to the fading impact of the temporary boost from the tax reduction from Q4 2024.

Additionally, external demand is expected to see only a modest increase as the global economy remains sluggish. The economy will recover moderately in the future but will not show signs of acceleration due to the lack of a strong driving force. On an annual basis (2024 calendar year), we expect a slight negative growth rate of -0.2%.

In FY2025, the sense of economic recovery is expected to gradually strengthen toward the latter half of the fiscal year. For the 2025 spring wage negotiations, we project a wage increase rate of 4.8%, with a base salary increase of 3%. The 2024 spring negotiations achieved a historic wage increase of 5.33%. Factors such as severe labor shortages, continued high prices, and solid corporate performance suggest that the 2025 spring negotiations will also result in high wage increases.

In the first half of FY 2025, real wage growth is likely to remain minimal due to persistently high inflation rates. However, as the cost-push inflationary pressures weaken, real wage growth is expected to gradually expand in the latter half of FY2025. Consequently, private consumption is also projected to gradually increase.

Business fixed investment is likely to continue on an increasing trend, including investment to address labor shortages, digital-related investment, research and development (R&D) investment related to growth areas and decarbonization, and investment associated with strengthening supply chains.

Furthermore, as the effects of monetary easing take effect, the global economy is expected to recover, leading to an increase in exports. Consequently, the overall economy is likely to improve gradually.

We forecast that core CPI will reach +2.6% for FY2024 and +2.1% for FY2025. The decision to reduce gasoline subsidies and the faster-than-expected increase in food prices have led to an upward revision of the outlook.

Due to the lingering effects of increased import costs from yen depreciation, core CPI is expected to remain high, at +2.5-3.0% year-on-year until the spring of 2025. However, the cost-push pressure from rising import prices is expected to gradually weaken. While the increased labor costs will lead to price pass-throughs, putting upward pressure on service prices, the growth in the prices of goods is anticipated to slow. As a result, core CPI is expected to gradually decelerate. We predict that in the latter half of fiscal year 2025, the core CPI will fall below +2% year-on-year.

Forecast of Real GDP (Quarter-on-Quarter Annualized Rate, Contribution)

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office

Japan's Economic Outlook (Yearly)

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office, Ministry of Economy, Trade and Industry, Ministry of Internal Affairs and Communications

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office, Ministry of Economy, Trade and Industry, Ministry of Internal Affairs and Communications

Japan's Economic Outlook (Quarterly)

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office

Original in Japanese:

https://www.dlri.co.jp/report/macro/396361.html

Disclaimer:

This report has been prepared for general information purposes only and is not intended to solicit investment. It is based on information that, at the time of preparation, was deemed credible by Daiichi Life Research Institute, but it accepts no responsibility for its accuracy or completeness. Forecasts are subject to change without notice. In addition, the information provided may not always be consistent with the investment policies, etc. of Daiichi Life or its affiliates.