- Report Index

- The Global Economy and Japan at a Crossroads

- Economic Trends

-

2026.06

The Global Economy and Japan at a Crossroads

Turning Crisis into Growth via "Responsible Proactive Fiscal Policy"

Toshihiro Nagahama

- Executive Summary

-

- Geopolitical Risks and Energy Pressures: Currently, escalating tensions in the Middle East surrounding Iran and the ongoing risk of a blockade in the Strait of Hormuz are keeping energy prices elevated, thereby reigniting global inflationary pressures. While Japan’s crude oil dependence has decreased compared to past historical levels, its structural dependence on the Middle East remains high. Consequently, there is an urgent need for "resilience investments" in supply chains to prepare for worst-case scenarios.

- Monetary Policy Normalization (FRB & BOJ): In the United States, market attention is intensely focused on the post-Powell policy direction following the appointment of Governor Warsh. With the U.S. economy aiming for a soft landing against the backdrop of a resilient labor market, the incoming chair faces a delicate balance between curbing inflation and preventing economic overheating. Under sustained high oil prices ($90–$100 range), the FRB is unlikely to ease its tight stance easily; a renewed spike in oil prices poses a stagflation risk. Conversely, the Bank of Japan (BOJ) faces the challenge of managing quantitative tightening (QT) ahead of its upcoming mid-term evaluation. Since premature tightening risks destabilizing the JGB market and exacerbating yen depreciation (potentially locking the currency into the 160s range), the BOJ must engage in meticulous market dialogue and pursue cautious, data-driven stewardship.

- The Essence of the Takaichi Administration's "Responsible Proactive Fiscal Policy": This policy

framework is fundamentally distinct from indiscriminate spending or conventional fiscal austerity. It

represents a growth-oriented fiscal strategy that shifts away from a rigid obsession with reducing

absolute debt volume, aiming instead to stabilize and lower the debt-to-GDP ratio. Capitalizing on a

"bonus period" where nominal GDP growth exceeds long-term interest rates due to inflation, the

government seeks to orchestrate a virtuous cycle of investment and growth. This will be achieved through

public-private partnerships focusing on 17 priority investment areas, such as AI, quantum technology,

and Green Transformation (GX). To preserve market confidence and demonstrate fiscal discipline, three

immediate challenges must be addressed:

- Rigorous cost-benefit analyses and viability checks for all investment projects.

- A phased transition to a "refundable tax credit" system to shore up the disposable income of low-to-middle-income households.

- A clear articulation of fiscal targets and a debt-to-GDP reduction path in the upcoming "Basic Policy on Economic and Fiscal Management and Reform" (Honebute no Hoshin).

- Conclusion: For the Japanese economy to fully break free from its long-standing deflationary mindset, it is imperative for the government and the central bank to align, articulate their risk assessments, maintain honest and transparent dialogue with financial markets, and resolutely execute bold, long-term growth investments.

1. Introduction: Demanding a "Proactive" Vision Amid a Polycrisis

The global economy is currently navigating a vortex of profound uncertainty. Geopolitical risks in the Middle East, particularly involving Iran, carry the perpetual threat of a prolonged blockade of the Strait of Hormuz. This situation exerts supply-side inflationary pressures on the global economy by keeping energy prices high. Elevated oil prices have reignited global inflation, forcing central banks into an exceptionally difficult balancing act between maintaining price stability and supporting economic growth.

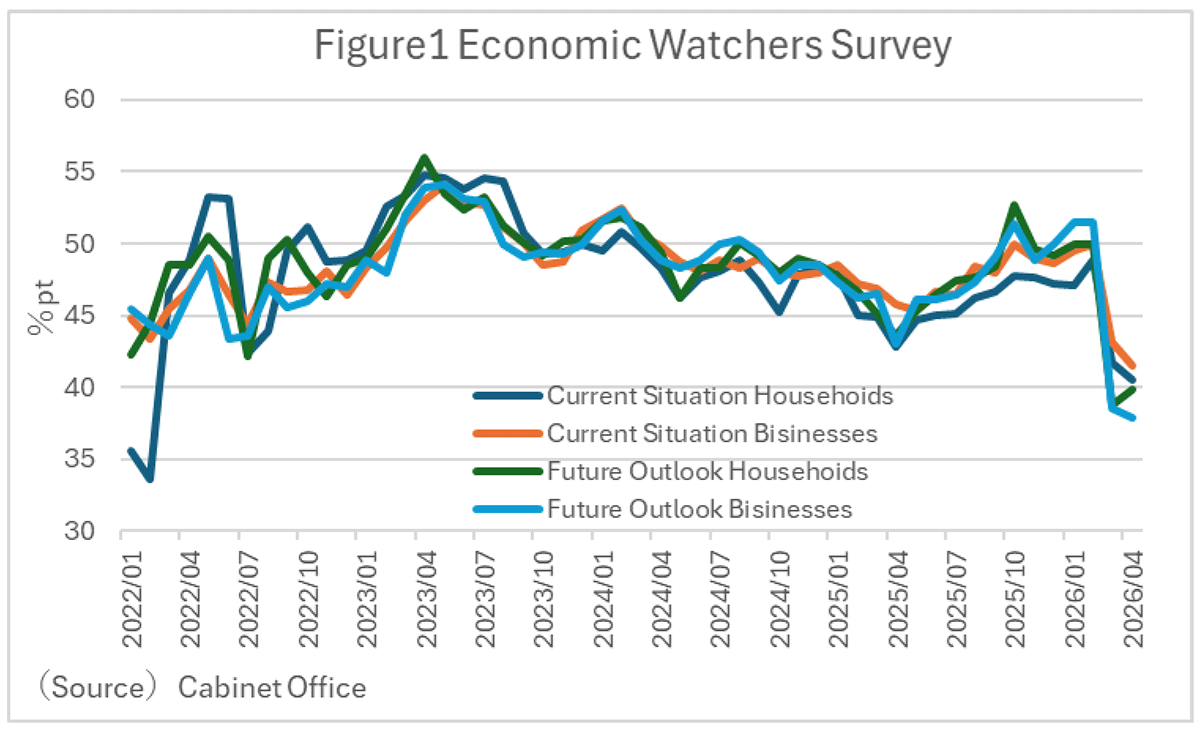

Amid these global headwinds, the Japanese economy maintains a trajectory of moderate recovery. However, consumer sentiment among households is softening, and corporate caution regarding the outlook is intensifying (Figure 1). Japan now stands at a critical juncture in its macroeconomic management, balanced between the BOJ’s ongoing search for an orderly normalization of monetary policy and the Takaichi administration’s execution of its signature "Responsible Proactive Fiscal Policy."

Accordingly, this paper evaluates the outlook for the global economy and explores the policy challenges facing the Takaichi administration. It outlines a strategic roadmap for Japan to secure a sustainable growth path within this highly complex environment.

2. Endless Geopolitical Risks and Rebuilding "Resilience"

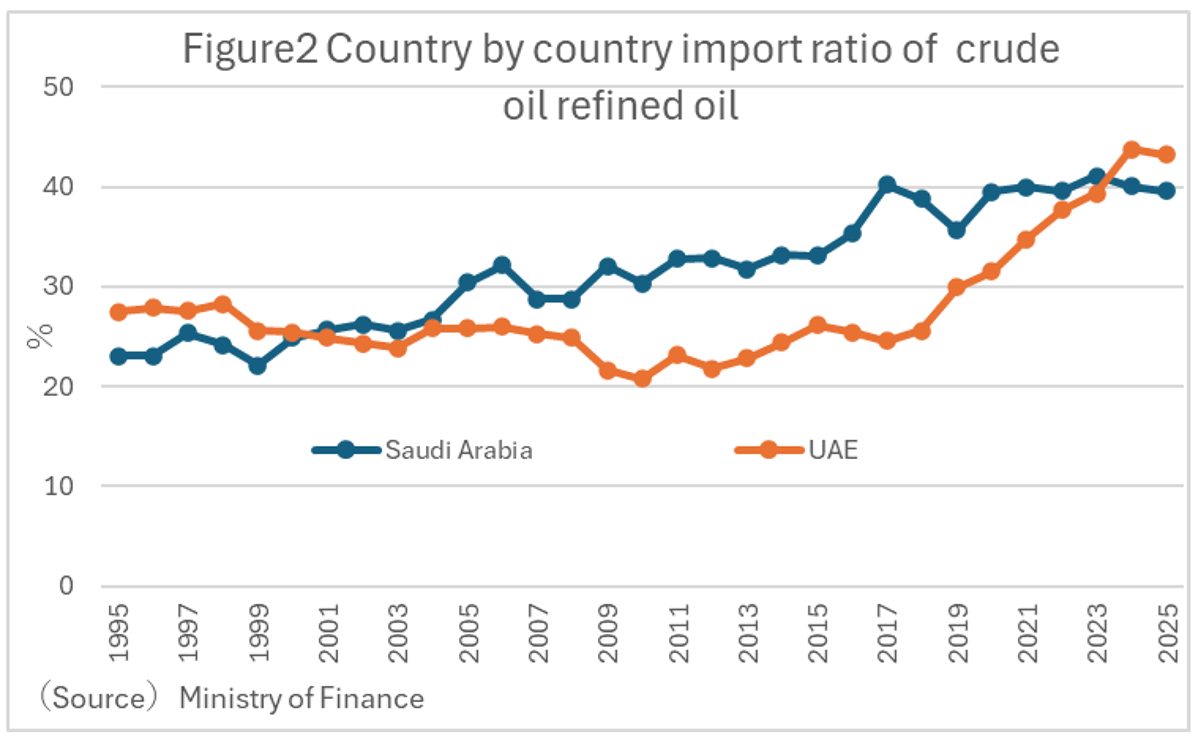

The prolonged elevation of energy prices triggered by the situation in Iran is no longer merely a temporary cost-push factor; it is actively accelerating the fragmentation of global supply chains. Compared to the oil shocks of the 1970s, the Japanese economy has structurally reduced its crude oil consumption, ostensibly improving its macroeconomic resilience. Nevertheless, Japan’s structural reliance on the Middle East for crude oil imports remains stubbornly high, leaving the nation undeniably vulnerable to supply disruptions (Figure 2).

Crucially, policy makers must not merely lament these deteriorating external conditions as unavoidable headwinds. Instead, they should treat them as a catalyst to accelerate structural economic transformation. Operating under the assumption of long-term Middle East instability, Japan must rapidly elevate energy-efficiency technologies and prioritize "crisis-management investments"—encompassing comprehensive energy security—as a matter of national strategy. Rather than depending on highly volatile expectations for peace negotiations, reinforcing supply chain resilience based on worst-case contingencies represents the only true path to national economic security.

3. Normalization of Monetary Policy: The Dynamic Between the BOJ and the FRB

Monetary policy shifts in both Japan and the United States remain the focal point for Japanese investors. In the U.S., market interest centers squarely on the post-Powell monetary framework under incoming FRB Chair Kevin Warsh.

The new leadership at the FRB must navigate a traditional dual mandate (maximum employment and price stability) that is heavily complicated by cost-push inflation stemming from high oil prices. With crude oil trading at elevated levels, the FRB cannot afford to prematurely relax its restrictive stance. Should oil prices resume an upward trajectory, the U.S. economy faces a tangible threat of stagflation. Furthermore, the incoming chair faces the structural responsibility of "updating" traditional policy frameworks, including optimizing the pace of balance sheet reduction (Quantitative Tightening) and potentially redefining core inflation metrics. Financial markets, while engaging in safe-haven dollar buying, are increasingly pricing in the risk that the FRB may struggle to fully suppress these persistent inflationary pressures.

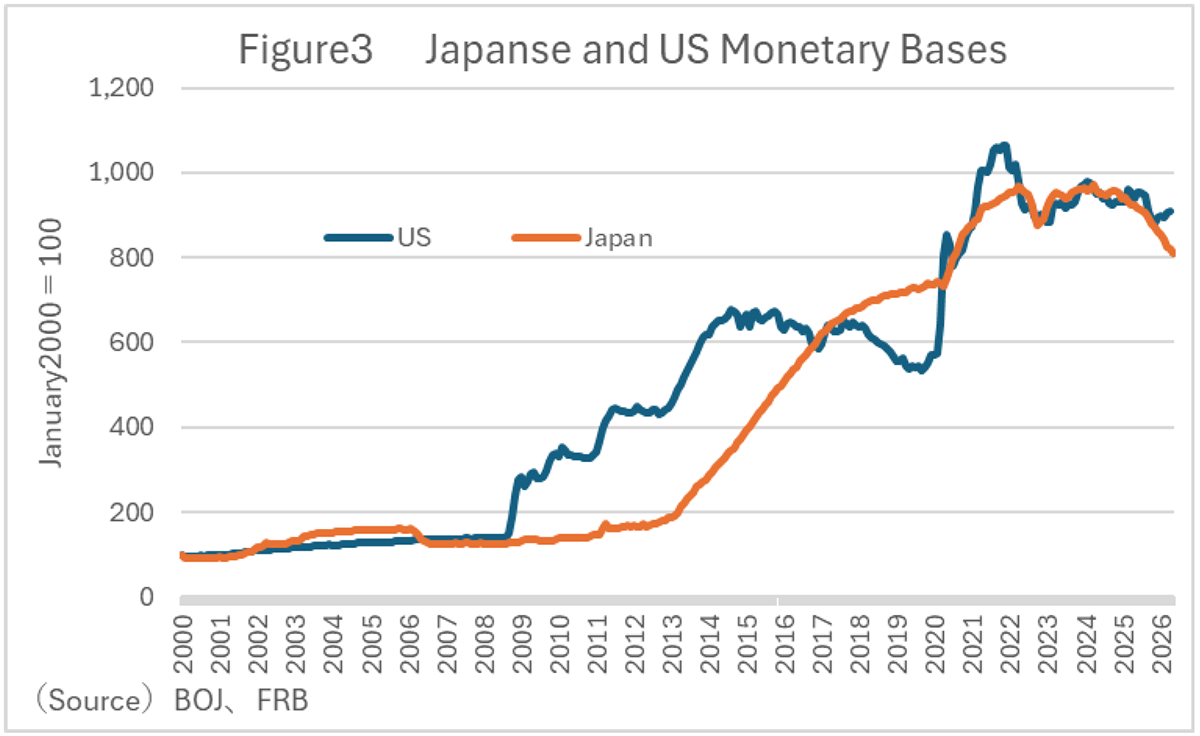

Concurrently, the Bank of Japan faces a critical test at its upcoming monetary policy decision meeting, where it may be forced to recalibrate its quantitative tightening roadmap (Figure 3). While an interim evaluation of QT will meticulously analyze impacts on government bond supply and demand, the operational reality remains severe. Some market participants argue that premature or aggressive quantitative tightening by the BOJ risks destabilizing the JGB market, thereby providing fresh speculative ammunition for yen-selling.

A weakening yen drives up import prices, directly worsening the cost-of-living burden on households. Compounded by rising energy costs from the gridlock in the Strait of Hormuz, the BOJ faces a stark dilemma: raise interest rates aggressively to counteract yen depreciation, or curtail its quantitative tightening plans to stabilize the domestic bond market. If the BOJ’s mid-term evaluation minimizes the risks to the bond market, speculative yen-selling driven by fears of fixed-income instability could accelerate, pushing the currency into a prolonged stay in the 160s range.

The primary risk here lies in the severe side effects of a "premature normalization." Amid heightened geopolitical volatility, aggressive rate hikes risk overcooling the real economy. The BOJ must maintain a cautious, data-dependent posture while simultaneously deepening its communication with market participants to clearly articulate its long-term tapering roadmap. Uncertainty is the catalyst for market volatility; providing a transparent, logically rigorous rationale for policy decisions is the only effective mechanism for stabilizing market expectations.

4. The Takaichi Administration's Economic Policy: The True Intent of "Responsible Proactive Fiscal Policy"

Against this turbulent international backdrop, domestic economic policy under the Takaichi administration is entering its implementation phase. The central pillar of this agenda is "Responsible Proactive Fiscal Policy." While some critics express concern that this framework could amplify inflation or erode fiscal discipline, it is vital to foster an accurate, structurally grounded understanding of its true intent.

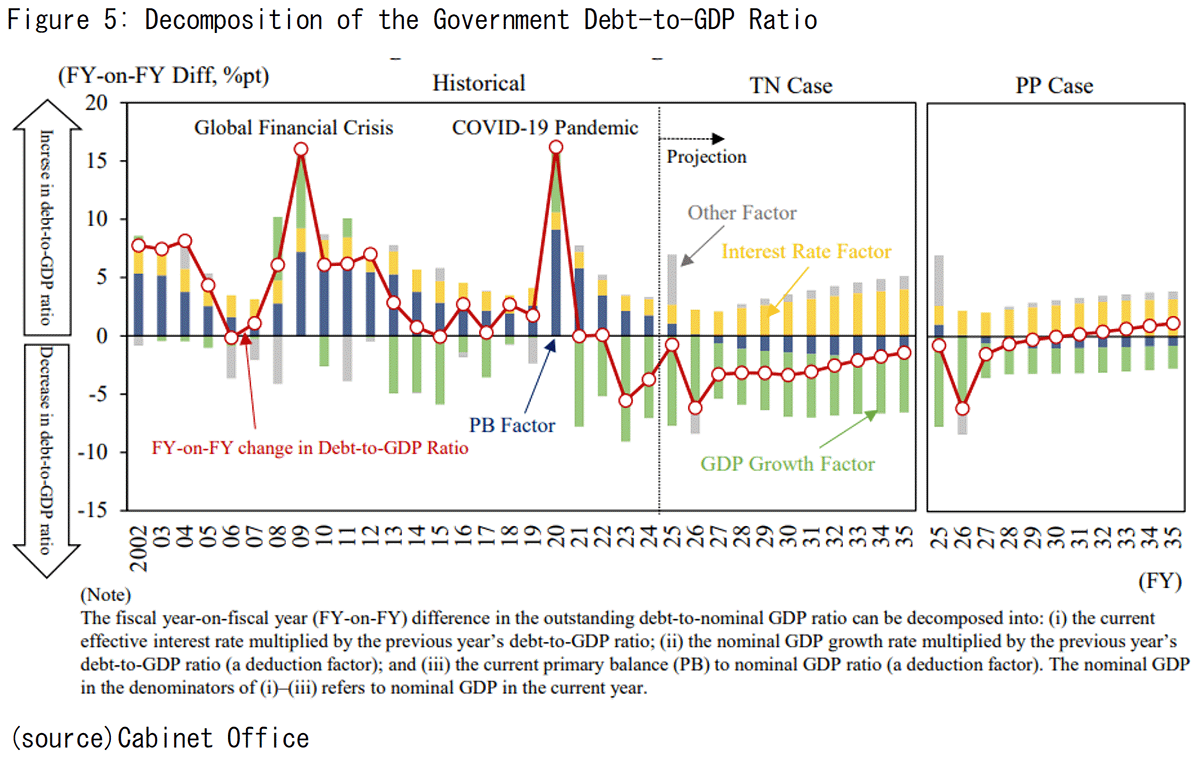

Responsible proactive fiscal policy is entirely distinct from indiscriminate populist spending. It represents a growth-oriented fiscal philosophy that deliberately abandons the traditional, austerity-driven preoccupation with the absolute nominal value of public debt. Instead, it focuses on systematically stabilizing and reducing the government debt-to-GDP ratio.

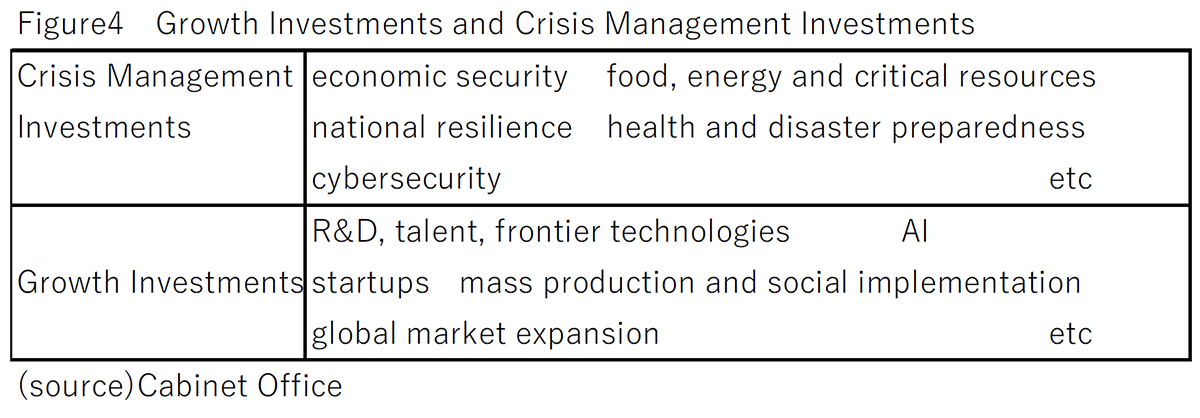

As Japan enters a structural inflationary phase, nominal GDP growth is systematically outperforming long-term nominal interest rates. By strategically leveraging this economic "bonus period" to funnel concentrated investments into sectors that enhance long-term potential growth, the government can expand the future tax base, thereby strengthening long-term fiscal sustainability. The administration's 17 priority investment fields form the core of this strategy. Specifically, by deploying public-private investment vehicles into high-yielding, high-innovation sectors such as artificial intelligence, quantum technology, and Green Transformation (GX), the policy aims to induce widespread private-sector innovation (Figure 4). This dynamic is indispensable for generating a "virtuous cycle of investment and growth" capable of outpacing inflation and cementing sustainable increases in real wages.

5. Securing the Confidence of Financial Markets

Executing a proactive fiscal policy requires sophisticated and continuous dialogue with financial markets. Institutional investors closely monitor whether government outlays represent uncoordinated structural spending or a strategic, return-maximizing allocation targeted at unlocking future economic growth.

To anchor market trust, the administration must fulfill three non-negotiable institutional requirements:

Rigorous Investment Governance: The government must establish stringent, independent mechanisms to evaluate the cost-benefit performance and economic viability of all subsidies and public investment projects.

Transition to Refundable Tax Credits: Implementing a phased transition to refundable tax credits can effectively shore up the disposable income of low-to-middle-income cohorts without introducing distortionary tax burdens, thereby stabilizing the aggregate consumption base.

Absolute Clarity on Fiscal Targets: The administration must explicitly anchor its fiscal framework around the debt-to-GDP ratio, clearly delineate spending priorities, and repeatedly reinforce its commitment to long-term fiscal discipline through transparent communication.

By addressing these core pillars, the Takaichi administration can successfully translate political momentum into a powerful engine of macroeconomic growth, provided it continuously articulates a clear, compelling national vision explaining exactly why these strategic investments are necessary today.

6. Turning Crisis into an Opportunity for Transformation

The contemporary global economy is shaped by a highly complex convergence of the situation in Ukraine, instability in the Middle East, and historic turning points in central bank policy. The overarching paradigm is clear: geopolitics is dictating economic realities. Given the opaque trajectory of Middle Eastern diplomacy, governments cannot afford to rely on optimistic assumptions; they must manage risk based on worst-case scenarios, such as a multi-year disruption in the Strait of Hormuz.

While these shifts present a formidable trial for Japan, they also represent a historic opportunity. As the country sheds its decades-long deflationary mindset and restores nominal growth, these external shocks serve as a critical test for fully escaping the paradigm of "contracting equilibrium."

To navigate this transition, three immediate policy priorities require urgent attention:

Advanced Low-Income Support: Moving beyond static debates over consumption tax rates, the government must build an efficient, targeted, and sustainable safety net against inflation, including an accelerated transition toward refundable tax credits.

Visualization of Fiscal Discipline: In the upcoming "Basic Policy on Economic and Fiscal Management and Reform," the government must present a concrete, mathematically viable trajectory for stabilizing and reducing the debt-to-GDP ratio to satisfy global bond investors.

Agile Energy Policy Management: In response to heightened crude oil volatility, Japan must complement the tactical deployment of strategic energy reserves with structural policy measures designed to bring forward its long-term energy-mix transition.

Ultimately, "Responsible Proactive Fiscal Policy" must function as a concrete, strategic playbook rather than a political slogan. It must create a resilient domestic demand base capable of insulated growth amid geopolitical shocks, structurally lifting Japan’s potential growth rate while aligning with shifting global economic currents.

As the FRB transitions to a new regime under Warsh, the BOJ carefully calibrates the timing of its rate hikes, and the Takaichi administration balances growth with fiscal discipline, the universal prerequisite for success remains a transparent, institutional dialogue with financial markets. As citizens contend with the tangible pressures of inflation and energy insecurity, the state and the central bank must clearly communicate their collective risk assessments and operational strategies. Articulating and executing this strategy transparently is the only viable mechanism for anchoring long-term inflation expectations and maintaining global market confidence.

In an environment of normalized monetary policy—a world characterized by positive structural interest rates—the capacity to fundamentally upgrade the nation's economic productivity is paramount. Japan must abandon its defensive macroeconomic posture and decisively commit to bold, long-term strategic investments.

Disclaimer:

This report has been prepared for general information purposes only and is not intended to solicit investment. It is based on information that, at the time of preparation, was deemed credible by Daiichi Life Research Institute, but it accepts no responsibility for its accuracy or completeness. Forecasts are subject to change without notice. In addition, the information provided may not always be consistent with the investment policies, etc. of Daiichi Life or its affiliates.