- Report Index

- World Economic Outlook (May 2026)

- Economic Trends

-

2026.05

World Economic Outlook (May 2026)

Yoshiki Shinke, Seiji Katsurahata, Osamu Tanaka, Toru Nishihama

1. Japan Economy

Current state of the economy: Japan’s economy remained resilient before the full impact of escalating Iran-related tensions

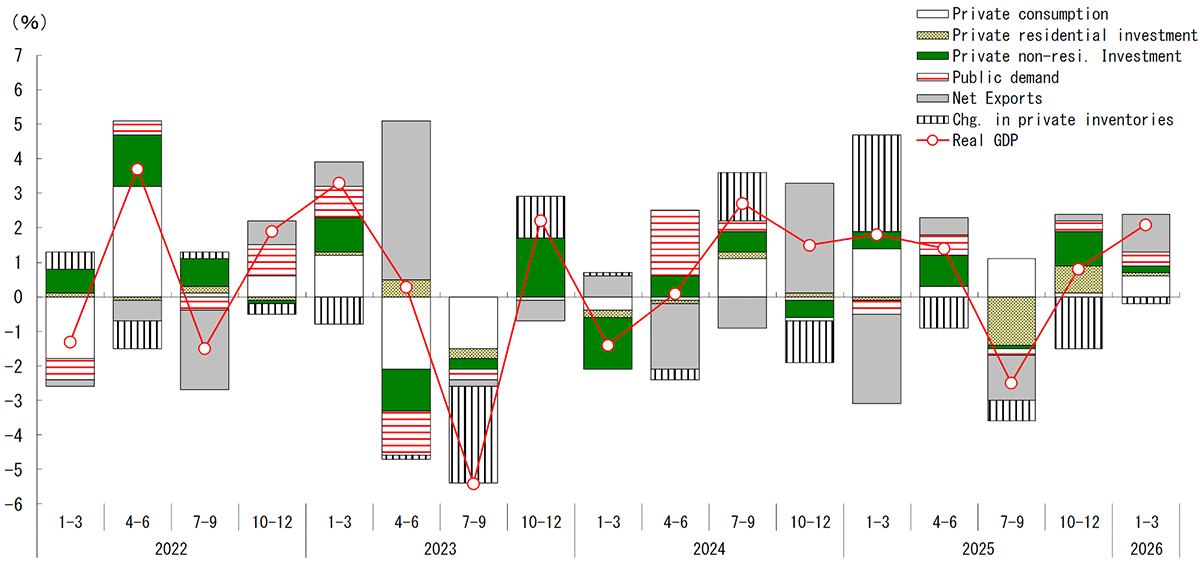

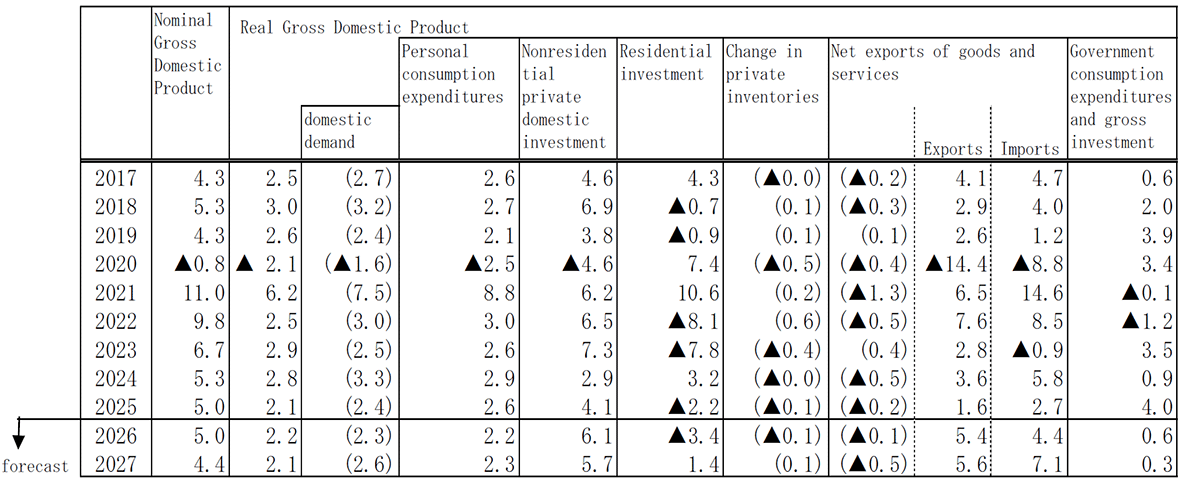

Real GDP (Quarter-on-Quarter Annualized Rate, Contribution)

Source: Cabinet Office.

Real GDP growth in Q1 2026 (January–March, first preliminary estimate) came in at +2.1% on a quarter-on-quarter annualized basis (+0.5% quarter-on-quarter), marking the second consecutive quarter of positive growth. Domestic demand remained resilient, with private consumption rising +0.3% quarter-on-quarter and business investment increasing by the same +0.3%, while housing investment and public investment also posted gains. Private consumption was supported by a moderation in inflation, reflecting slower growth in food prices and the impact of government subsidies for electricity and gas charges, which helped real wages turn positive. On the external side, exports rose strongly by +1.7% quarter-on-quarter, supported by an increase in exports to Asia and a recovery in automobile exports to the United States, thereby pushing up overall growth. In this way, both domestic and external demand remained firm, resulting in growth above the potential growth rate. Overall, the data suggest that Japan’s economy had maintained a moderate recovery trend before the adverse effects of escalating Iran-related tensions became full-fledged.

With regard to the worsening situation in Iran, exports to the Middle East fell sharply in March, while consumer sentiment also deteriorated. However, the impact on Q1 growth was limited. This likely reflects the fact that the effects began to emerge only in March, meaning that their impact was diluted when viewed on a quarterly average basis, and that the adverse effects had not yet become full-fledged as of March.

Economic outlook: Downward pressure to intensify in the near term, but the recovery trend is expected to be maintained

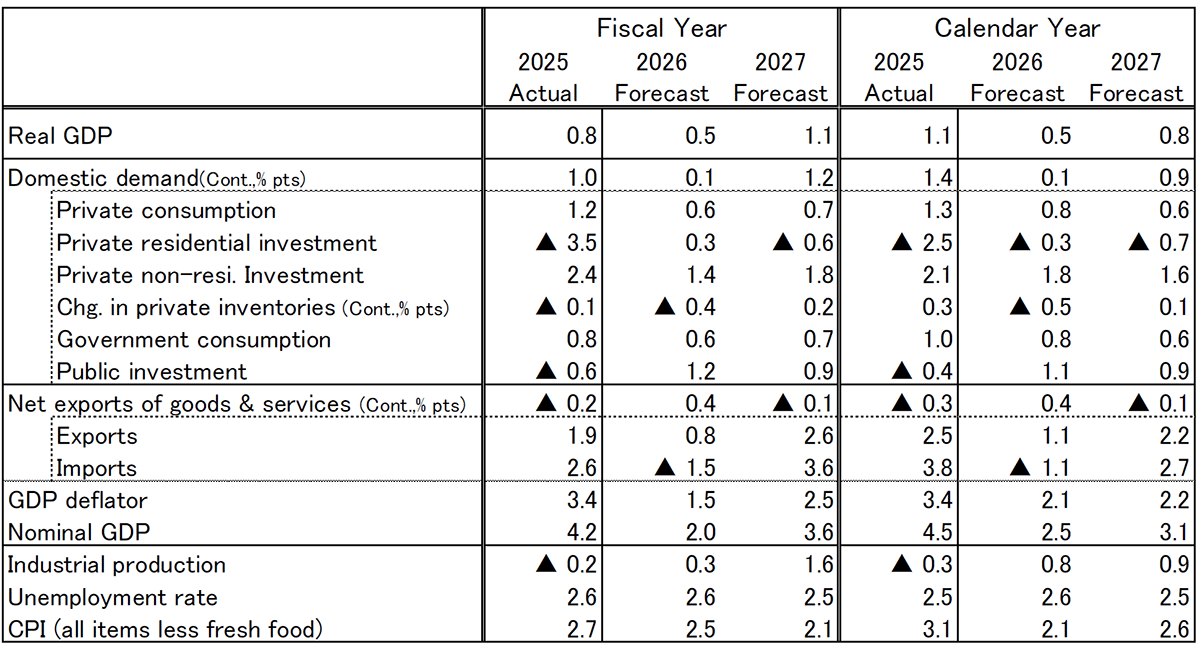

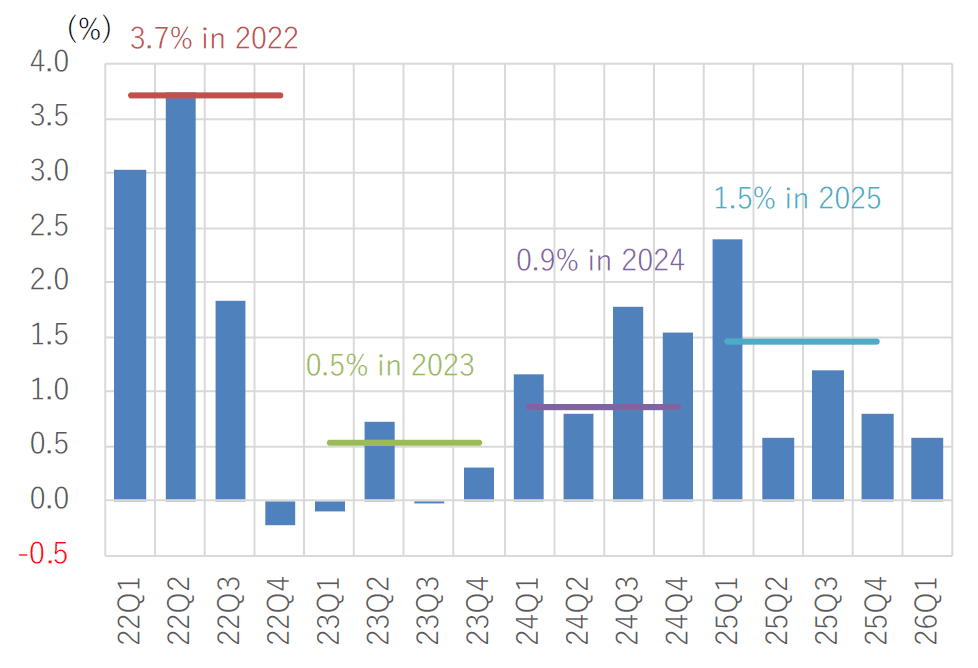

Japan’s Economic Outlook (Yearly)

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office, Ministry of Economy, Trade and Industry, Ministry of Internal Affairs and Communications.

Looking ahead, downward pressure on the economy is likely to intensify as the effects of worsening Iran-related tensions become more pronounced. The primary concern is the adverse impact of supply uncertainty and sourcing difficulties. In periods of supply uncertainty, firms tend to secure and build up inventories earlier than usual in order to maintain business continuity, which may further tighten supply-demand conditions. Recently, sourcing difficulties, delivery delays, and order restrictions have begun to emerge in petrochemical products and construction materials. Going forward, these developments could constrain economic activity in the form of production and shipment delays, as well as delays or interruptions in construction work. Exports are also likely to face downward pressure. Exports to the Middle East are expected to remain weak for the time being, while supply constraints could weigh on production activity both in Japan and abroad. Against this backdrop, real GDP growth in Q2 2026 (April–June) is forecast to turn slightly negative, at –0.3% annualized quarter-on-quarter.

Although the economy is expected to stagnate in the near term, there is no need to conclude that the recovery scenario itself has collapsed. At present, concerns over declining imports and reduced supply availability are being compounded by firms’ efforts to secure inventories in anticipation of future supply shortages, which in turn is contributing to distribution bottlenecks and sourcing difficulties. If the outlook for supply normalization becomes clearer as the situation surrounding the closure of the Strait of Hormuz moves toward resolution, the view that existing inventories and alternative sourcing can cover near-term needs should become more widespread. Supply uncertainty and related disruptions would then likely subside. While the impact on prices and the drag on the economy are likely to persist for some time, they should remain within a manageable range, given buffers such as the high level of corporate profits. In this case, the decline in Q2 would be temporary, and growth would likely return to positive territory from Q3 2026 onward.

On the other hand, the possibility cannot be ruled out that negotiations between the United States and Iran will fail to reach an agreement and that no progress will be made toward resolving the closure of the Strait of Hormuz. In that case, the limits of relying on inventories and alternative sourcing would become increasingly apparent, and anxiety would intensify further. If firms accelerate efforts to secure inventories, disruptions could spread further and upward pressure on prices would likely strengthen. Production activity and construction work could remain depressed for a prolonged period, while exports could face larger downside pressure. If such a situation materializes, the economy could enter a recession.

2. US Economy

Current Economic Conditions: Resilience Defying High Oil Prices Amid Resurging Inflationary Pressures

Currently, the reconstruction of foreign relations based on the Trump administration's “America First” doctrine is progressing rapidly in the United States. With the tightening of tariff measures, heightened military posturing, and strict crackdowns on illegal immigration ongoing, both domestic and international geopolitical and policy uncertainties remain at an extremely high level. However, underlying economic activity maintains its resilience, driven by a rapid expansion in IT investment, particularly in AI-related sectors, while inflation has begun to climb once again.

The real GDP growth rate of the U.S. for the first quarter of 2026 (advance estimate) reaccelerated to an annualized rate of 2.0%, up from 0.5% in the fourth quarter of 2025, propelled by IT-related investments. This momentum has shown no signs of waning moving into the second quarter. The ISM Manufacturing PMI for April came in at 52.7 (unchanged from March), remaining above the 50 mark separating expansion from contraction for the fourth consecutive month, indicating that the expansionary trend in the U.S. manufacturing sector is being sustained. Meanwhile, the ISM Services PMI remained elevated at 53.6 (down slightly from March's 54.0), confirming that the services sector continues to expand robustly on the back of resilient domestic demand.

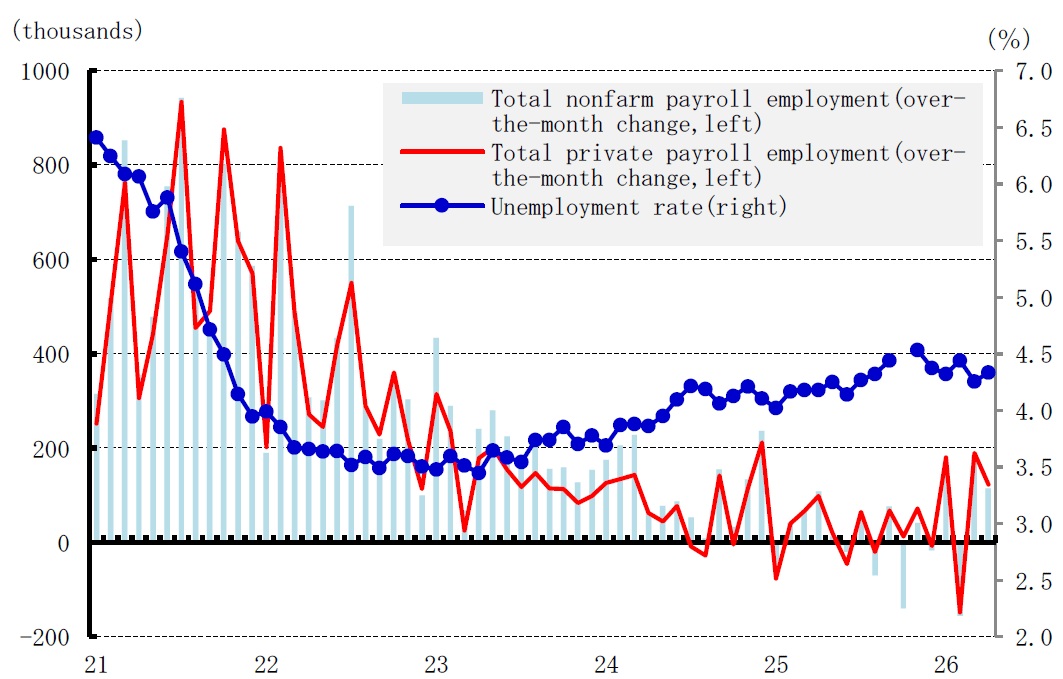

The labor market is also regaining its strength. In April, U.S. nonfarm payrolls increased by 115,000 (down from 185,000 in March), while private payrolls expanded by 123,000 (down from 190,000 in March), sustaining a solid upward trajectory. Under these conditions, the unemployment rate for April held steady at 4.3%, remaining near a relatively low level.

US labor situation

Source: US Department of Labor.

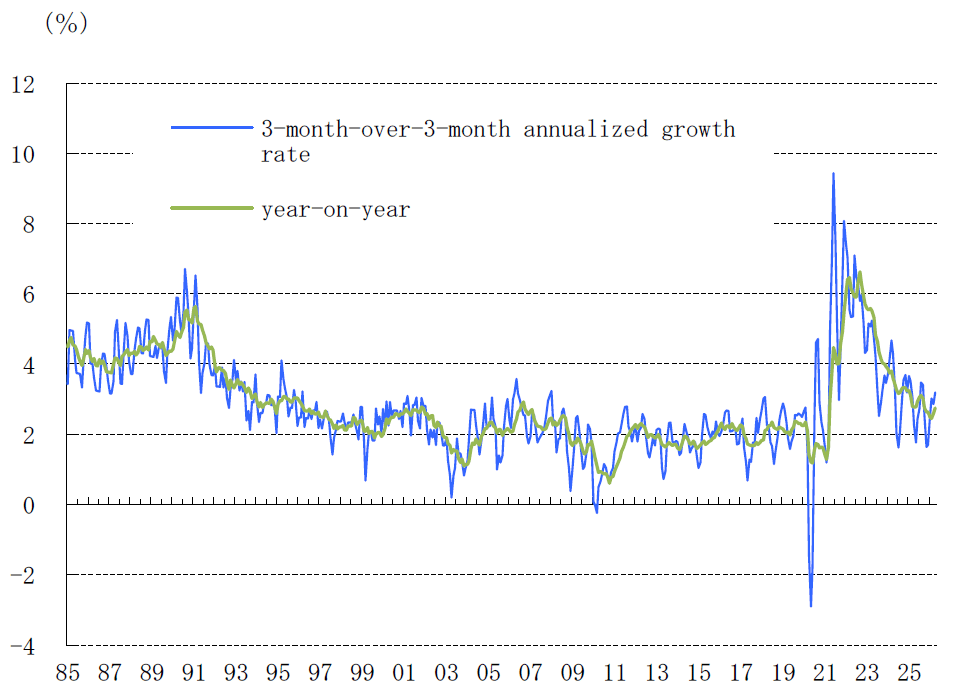

US core CPI

Source: US Department of Labor.

On the other hand, the resilience of the economy and intensifying tensions in the Middle East are amplifying inflationary pressures. In April, headline CPI inflation accelerated to 3.8% year-on-year (up from 3.3% in March). By component, food prices rose by 3.2% (up from 2.7% in March), with energy prices spiking 17.9% (up from 12.5% in March), largely driven by surges in gasoline (28.4%) and fuel oil (54.3%). Core CPI, which reflects the underlying trend of inflation, also rose to 2.8% (up from March's 2.6%), signaling a resurgence of inflationary pressures.

Against this backdrop, at the FOMC meeting held on April 28 and 29, 2026, the Fed decided to keep the target range for the federal funds rate unchanged at 3.50%–3.75%. While the hold marked the third consecutive meeting and was in line with market expectations, the decision saw 8 votes in favor and 4 dissents, resulting in the largest split since October 1992. While Fed Governor Milan dissented in favor of a 25-basis-point rate cut, three regional Fed presidents—Hammack, Kashkari, and Logan—agreed with the hold but opposed retaining an easing bias in the statement, clearly signaling a hawkish stance focused on heightened vigilance against inflation.

Economic Outlook: 2026 Real GDP Growth Projected to Sustain 2% Pace

Looking ahead, the U.S. economy is expected to follow a pattern where the downward pressure from tariff policies is offset and driven upward by aggressive fiscal policies. Following the Supreme Court ruling in February 2026, which declared tariffs under the IEEPA (International Emergency Economic Powers Act) illegal, the administration shifted to Section 122 of the Trade Act (a universal 10% additional tariff). As a result, the effective tariff rate for 2026 is projected to fall to approximately 7.1%, down from 14.9% to 15.2% in 2025 (and 2.4% in 2024). Consequently, the drag on real GDP growth is estimated to be contained at 0.1–0.2 percentage points, compared to a drag of about 0.5 percentage points in 2025.

Conversely, the budget reconciliation act known as the “OBBBA” (One Big Beautiful Bill Act), enacted on July 4, 2025, will provide a strong tailwind for economic growth. This legislation extends key provisions of the 2017 Tax Cuts and Jobs Act (TCJA) and introduces new tax relief measures, while incorporating spending adjustments such as cuts to social safety net programs and increased expenditures for defense and border security. Although some measures commenced in 2025, the tax relief effects are projected to peak in 2026, boosting real household incomes and supporting the expansion of personal consumption. Furthermore, capital expenditure is expected to expand owing to investment tax incentives. Together, these factors are anticipated to lift real GDP by approximately 0.4–0.8 percentage points.

For the full year of 2026, the U.S. economy is forecast to maintain solid growth, supported by the normalization of government operations and the positive impact of these tax cuts. Personal consumption, despite being affected by rising prices, is expected to remain firm, bolstered by wealth effects from rising stock and real estate prices, as well as an increase in disposable income due to tax cuts. Capital expenditure growth is also poised to accelerate, driven by the tax benefits, expanding IT demand, reduced uncertainty from progressing trade agreements, and an increase in direct investment. Additionally, an expansion in exports of agricultural products and energy is anticipated following trade agreements.

Based on these factors, the U.S. economy is highly likely to maintain a pace exceeding its potential growth rate, expanding at a solid 2.2% for the full year of 2026. Regarding the labor market, while the unemployment rate is expected to remain stable below 4.5%, nonfarm payroll gains are projected to moderate to around 90,000 per month, indicating a continuation of gradual employment growth. On the inflation front, although housing-related costs are expected to keep declining, overall inflation is highly likely to experience a gentle upward trajectory going forward as rising crude oil prices and the impact of tariffs gradually pass through to downstream sectors. In an environment where such resilient growth coexists with persistent inflation, the Fed is expected to maintain an extremely cautious stance regarding interest rate cuts throughout 2026.

US economic outlook (YoY, %)

Note: Forecasts are by the Daiichi Life Research Institute.

Source: US Department of Commerce.

3. Euroarea Economy

Current State of the Economy: The Impact of Rising Commodity Prices Begins to Emerge

In the eurozone, whilst economic stagnation persists in core countries such as Germany, which has fallen into a structural recession, and France, which faces fiscal instability, a moderate economic expansion continues, supported by high growth in former debt-stricken countries such as Spain, Ireland, Portugal and Greece. Real gross domestic product (GDP) in the eurozone remained at a sluggish growth rate of less than 1% in 2023 and 2024, but by 2025, having weathered the impact of US tariff hikes, growth accelerated to 1.5%, in line with potential growth. Although the economy has continued to expand at a moderate pace into 2026, soaring commodity prices caused by the escalating situation in Iran have become a new downward pressure on the European economy. Europe is not particularly dependent on crude oil, petroleum products and natural gas from the Middle East, and has not faced a shortage of energy resources even following the closure of the Strait of Hormuz. However, as many European countries rely on imports of energy resources from outside the region, rising resource prices are inevitably pushing up inflation and weighing on the economy.

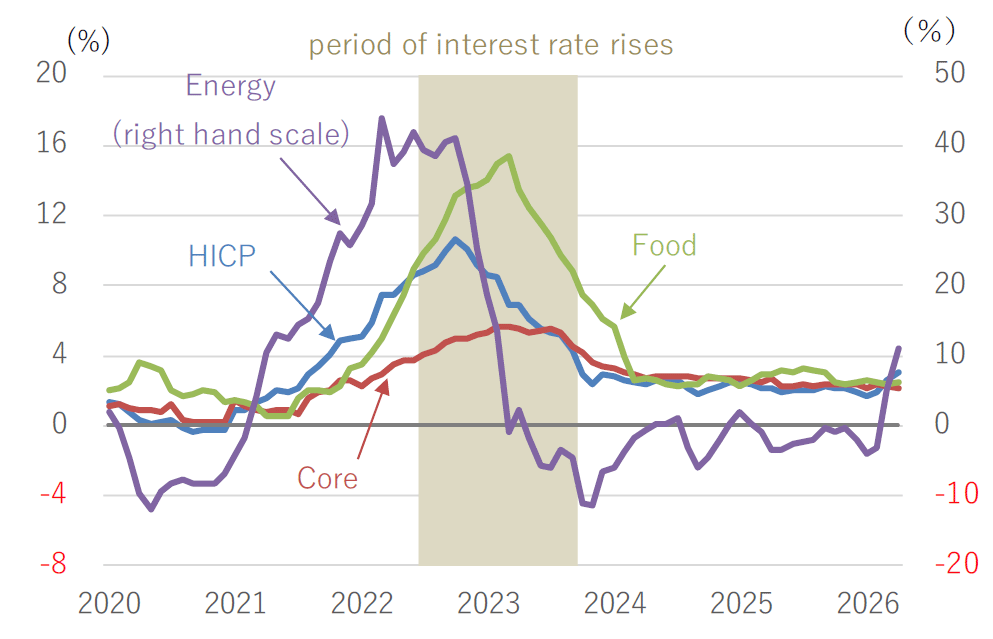

The adverse effects of the situation in Iran are beginning to manifest in some monthly indicators. The rate of consumer price inflation in the eurozone, which had slowed to around 2%, the level considered to ensure medium-term price stability, accelerated to +2.6% in March and +3.0% in April following a renewed surge in energy prices. With crude oil prices remaining high, the impact is expected to spread to non-energy prices in the coming months, and the rate of inflation is forecast to accelerate further. Rising fuel and electricity costs, driven by higher commodity prices, along with price increases for everyday goods, are leading to a deterioration in household sentiment. Business sentiment is cooling rapidly, particularly in the service sector, where a decline in demand is anticipated due to rising prices. Long-term interest rates across Europe are rising, driven by the view that accelerating inflation will necessitate policy rate hikes, as well as the need for fiscal support for households and businesses. Financial conditions are also tightening, with banks adopting a stricter lending stance.

The European Central Bank (ECB) kept its policy interest rates unchanged at its April Governing Council meeting, citing high uncertainty surrounding the situation in Iran, the fact that the impact of soaring commodity prices has not yet been fully confirmed by data, the leeway to wait before raising rates given the neutral stance of current policy, and the fact that the tightening of financial conditions is already having an effect equivalent to a rate hike. It considers the six weeks leading up to the next Governing Council meeting to be an appropriate timeframe for reassessing developments in the Middle East, their impact on the inflation outlook, and the appropriate monetary policy response, thereby signalling the start of interest rate rises in June.

Euroarea Real GDP Growth (SAAR)

Source: Eurostat, Daiichi Life Research Institute.

Euroarea Harmonised Index of Consumer Price (YoY)

Note: Core inflation excludes energy, food, alcohol and tobacco.

Source: Eurostat, Daiichi Life Research Institute.

Economic Outlook: Fiscal Expansion Provides a Buffer, Averting a Recession

Looking ahead, as the full impact of rising commodity prices takes hold, upward pressure on prices and downward pressure on the economy in the eurozone are expected to intensify throughout 2026. However, compared to the surge in energy prices following Russia’s invasion of Ukraine in 2022, whilst crude oil prices have risen to similar levels, the increase in natural gas prices has been limited. Electricity prices in Europe are highly correlated with gas prices. Compared to 2022, when the inflation rate temporarily exceeded 10 per cent, the upward pressure on prices is expected to remain modest.

Although a deterioration in households’ real purchasing power and corporate earnings due to inflation is unavoidable, the effects of Germany’s historic shift in fiscal policy and increased defence spending across European countries are set to take full effect. Furthermore, the strong economic performance of Spain and Ireland, supported by immigration inflows and the activities of multinational corporations, the provision of financial support to EU member states through the European Recovery Fund and the European Rearmament Plan, the expansion of renewable energy investment within the EU to mitigate risks from instability in the Middle East and soaring resource prices, increased investment in AI and labour-saving technologies, and the expansion of defence-related investment to reduce dependence on US defence capabilities, are all expected to underpin the economy. Furthermore, although new financial support through the European Recovery Fund is set to end at the end of 2026, the positive effects on the economy are expected to persist beyond 2027. This is because the results of the structural reforms required to receive the funds will become apparent, and it will take time for the financial resources provided to be channelled into expanded investment and other areas.

Although the eurozone’s growth rate is expected to fall back below 1% in 2026 due to the deteriorating situation in Iran, we anticipate a return to growth in the low 1% range in 2027, once the upward pressure on prices has subsided. Should the situation in Iran deteriorate further or a blockade of the Strait of Hormuz become protracted, leading to a more significant rise in commodity prices, supply chain disruptions and a broader impact on the global economy, the risk of a recession or prolonged stagnation would increase.

Wary of rising inflationary pressures caused by soaring commodity prices, we expect the ECB to raise interest rates by 0.25 percentage points in both June and September 2026. Whereas the 2022 rate-hiking cycle began with negative interest rates and was a response to historically high inflation exceeding 10 per cent, the current cycle is starting from a neutral rate of 2 per cent, and with inflation remaining limited, it is highly likely that rate hikes will be modest. We anticipate that, once the rise in commodity prices has levelled off and inflationary pressures have subsided, the ECB will shift to cutting rates in 2027, returning the policy rate to the neutral rate level.

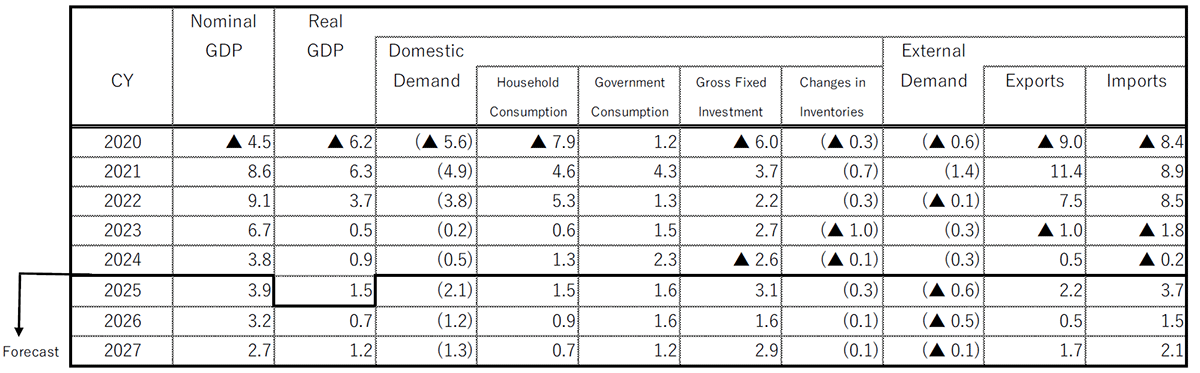

Outlook of the Euroarea Economy (YoY, %)

Note: Figures in brackets are contributions to real GDP growth. No breakdown is available for 2025 at the time of publication.

Source: Daiichi Life Research Institute.

4. China and Emerging Asian Economies

Current State of the Economy: Solid external demand supports near-term growth, while escalating tensions in the Middle East cloud the outlook

At the National People’s Congress (NPC) held in March 2026, the Chinese authorities announced a plan to lower the country’s 2026 economic growth target to “4.5–5.0%.” Behind this decision lies concern that the full-scale implementation of Trump-era tariffs will weigh on external demand through their adverse impact on the global economy. In addition, prolonged weakness in the property sector and employment uncertainty, particularly among younger workers, continue to weigh on domestic demand, leaving downside pressures on the economy piled up both domestically and externally.

Nevertheless, China’s real GDP growth accelerated to +5.0% (y-o-y) in the January–March quarter from +4.5% in the previous quarter, marking the first time in three quarters that growth exceeded 5%. On a quarter-on-quarter annualized basis, growth also accelerated to +5.3% from +4.9%, representing the strongest expansion in five quarters. Overall, the Chinese economy made a favorable start to 2026.

One factor behind this resilience is that the Chinese authorities, anticipating further deterioration in U.S.-China relations, have actively expanded exports to countries and regions outside the U.S. Exports to emerging economies such as those in Africa, Asia, and Latin America have remained particularly robust, while exports to Europe have also stayed firm. In addition, exports to the U.S. have recently shown signs of recovery. On the other hand, domestic demand components such as private consumption and investment remain relatively weak, suggesting that the economy has become even more dependent on external demand in the near term.

Many emerging Asian economies are structurally highly dependent on external demand, and countries with relatively high export exposure to the U.S. were initially expected to suffer significantly from “Trump tariffs”. However, U.S. tariff rates imposed on these economies have remained broadly similar, preventing tariff differentials from materially affecting export competitiveness.

Moreover, strong global investment related to AI (artificial intelligence) has boosted exports of semiconductors and other electronic components, thereby supporting overall exports. As a result, external demand has continued to underpin economic activity, particularly in economies heavily dependent on exports.

On the other hand, emerging Asian economies are geographically close to the Middle East and rely heavily on the region for imports of crude oil, natural gas, and chemical fertilizer. Therefore, escalating tensions in the Middle East and related supply concerns are having a direct impact on these economies. In particular, countries with limited crude oil reserves have increasingly been forced to curb demand through measures such as reducing energy-related subsidies, leading to higher prices. This has intensified inflationary pressures and heightened concerns about adverse effects on a wide range of economic activities.

Furthermore, in financial markets, concerns over worsening external balances and rising inflation, due to higher oil prices, and the trend of buying USD in times of crisis, have intensified depreciation pressures on regional currencies. This, in turn, has raised concerns that imported inflation could further accelerate inflation.

Although many emerging Asian economies showed resilience during the January–March quarter, inflationary pressures have already become visible in recent months, while currency depreciation pressures in financial markets have also intensified. As a result, central banks in emerging Asian economies are increasingly being forced to tighten monetary policy. Consequently, uncertainty over the economic outlook is rising rapidly, especially in economies that are structurally more dependent on domestic demand, where inflationary pressures and monetary tightening are beginning to coexist.

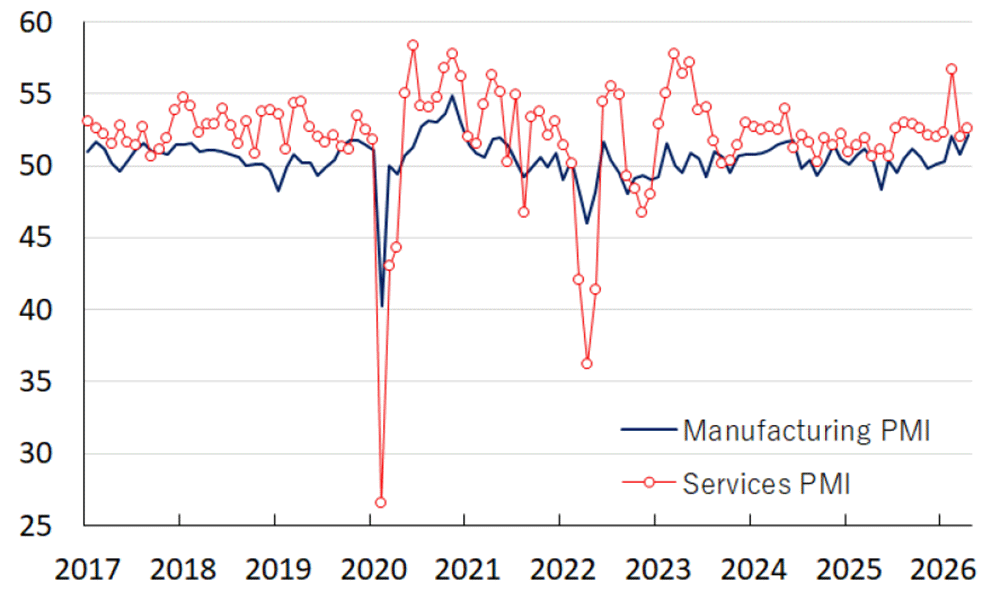

RatingDog China Mfg. and Services PMI

Source: S&P Global.

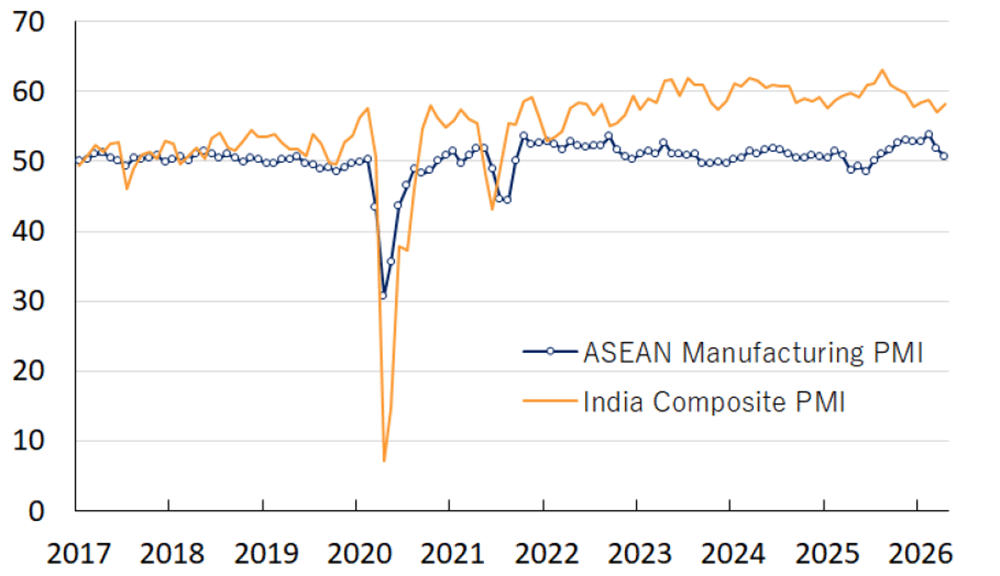

S&P India Comp. PMI and ASEAN Mfg. PMI

Source: S&P Global.

Economic Outlook: Economic developments likely to remain heavily influenced by the trajectory of escalating tensions in the Middle East

The U.S.-China summit held in May is widely viewed as having produced outcomes that fell significantly short of financial market expectations, as agreements on trade and investment were effectively postponed. Nevertheless, a further escalation of U.S.-China tensions has been avoided, and if future negotiations on trade and investment lead to a stronger recovery in bilateral trade, external demand could provide additional support for the Chinese economy.

In the first half of 2025, effective depreciation of RMB improved China’s export competitiveness and consequently contributed to a substantial increase in exports. However, from the second half of the year, concerns have grown that the effective appreciation of the RMB may weaken export competitiveness. Therefore, looking ahead, the People’s Bank of China (PBOC) may attempt to guide effective depreciation the RMB under the banner of strengthening “counter-cyclical and cross-cyclical adjustments.”

Meanwhile, although the property market has shown signs of stabilization in some major cities, there are few signs of a bottoming-out in other regional cities, and negative wealth effects continue to weigh on private consumption. In addition, rising commodity prices, particularly crude oil prices driven by escalating tensions in the Middle East, have exposed Chinese companies to increasing inflationary pressures. However, with uncertainty surrounding consumer demand persisting, companies are struggling to pass higher costs on to final product prices, leaving them caught in a difficult dilemma.

Looking ahead, China’s economy is expected to continue to be driven primarily by the supply side, while demand—particularly domestic demand—remains sluggish, resulting in an increasingly “K-shaped” recovery marked by persistent imbalances.

Easing U.S.-China tensions could serve as a tailwind for emerging Asian economies, which are structurally more dependent on external demand. Moreover, following a U.S. Supreme Court ruling that Trump tariffs were unconstitutional, Trump tariffs have effectively been reduced, lowering barriers to exports to the U.S. As a result, the external environment surrounding emerging Asian economies has improved.

On the other hand, rising prices for crude oil and other energy resources stemming from escalating tensions in the Middle East are dealing a direct blow to emerging Asian economies that depend heavily on energy imports from the region. Many countries have kept fuel prices down through subsidies but worsening fiscal conditions and concerns over insufficient reserves have forced governments to reduce subsidies and curb demand, adversely affecting a broad range of economic activity.

Furthermore, in addition to mounting inflationary pressures, concerns over deteriorating external balances have triggered capital outflows and currency depreciation, heightening the risk of imported inflation. Under these circumstances, some central banks have been forced to tighten monetary policy in order to stabilize prices and currencies.

Consequently, emerging Asian economies with relatively high dependence on domestic demand face an accumulation of factors weighing on economic activity. At present, the outlook for tensions in the Middle East remains highly uncertain. These tensions are already acting as a drag on emerging Asian economies through higher crude oil and fertilizer prices, while the risk of further escalation cannot be ruled out. Moreover, a contraction in trade activities related to the Middle East is also likely to weigh on the economies of countries with relatively high export exposure to the region.

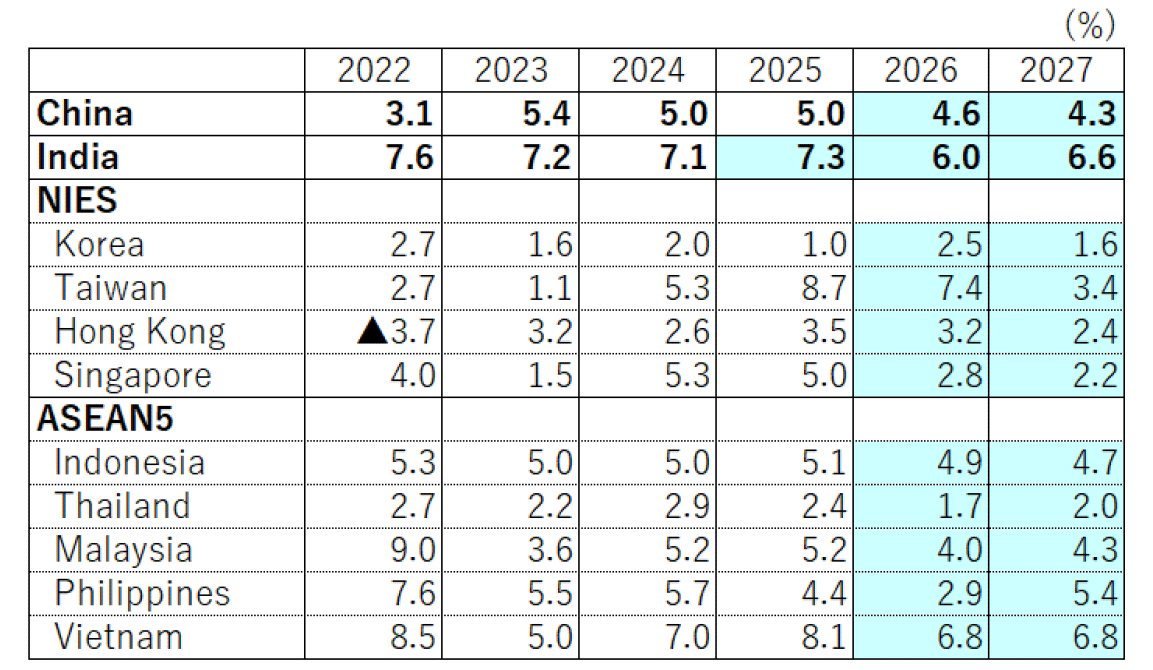

Economic Growth Rates in China, India, NIES, and ASEAN5 Countries

Source: CEIC data. The light blue areas indicate our forecasts. For India, data are based on the fiscal year (From April to March).

Disclaimer:

This report has been prepared for general information purposes only and is not intended to solicit investment. It is based on information that, at the time of preparation, was deemed credible by Daiichi Life Research Institute, but it accepts no responsibility for its accuracy or completeness. Forecasts are subject to change without notice. In addition, the information provided may not always be consistent with the investment policies, etc. of Daiichi Life or its affiliates.