- Report Index

- International Comparison of Fiscal Outlooks for G7 Countries

- Economic Trends

-

2026.05

International Comparison of Fiscal Outlooks for G7 Countries

~ Implications for Japan's Fiscal Policy Based on the IMF Report ~

Toshihiro Nagahama

- Executive Summary

-

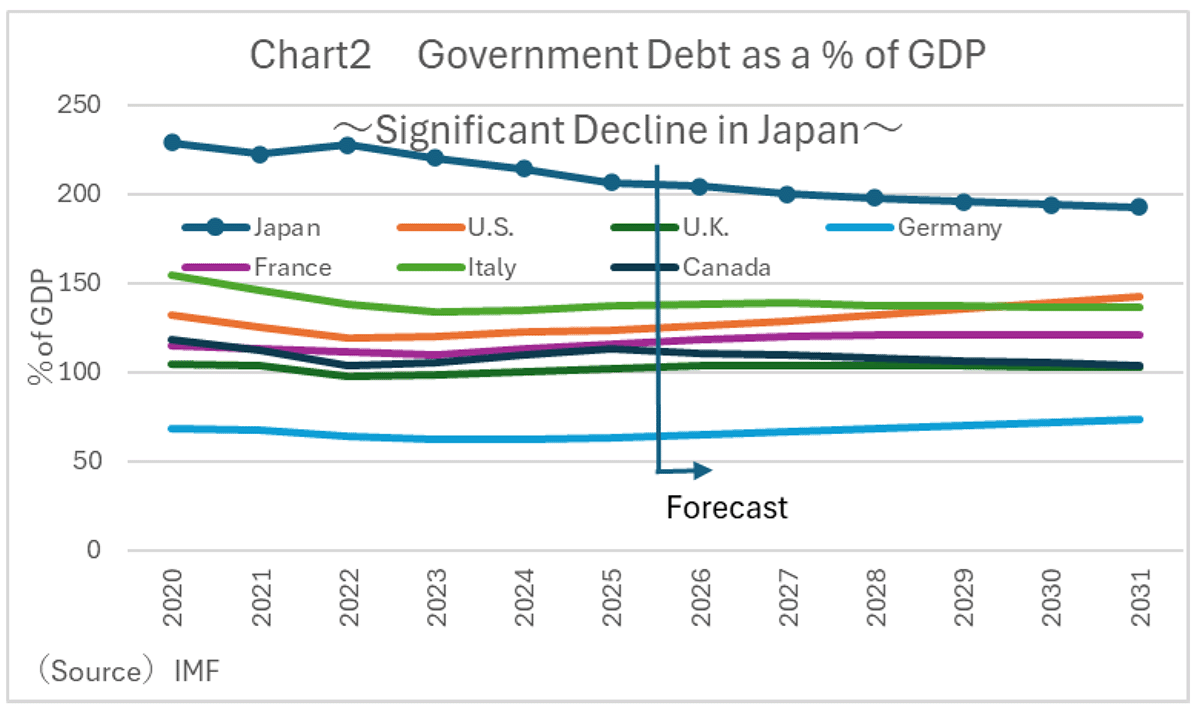

- According to the IMF's April 2026 report, G7 fiscal conditions are becoming polarized amidst high global public debt and rising structural spending (interest payments, defense, etc.). The United States faces a serious situation with massive deficits despite near full employment; its debt-to-GDP ratio is projected to reach 142% by 2031. Conversely, Japan is expected to show the most improvement, with debt dynamics turning positive due to inflation and nominal growth; its ratio is projected to fall by 14 points by 2031. In Europe, the UK is improving through tax hikes, while Germany’s debt ratio is expected to rise due to fiscal rule reforms prioritizing investment.

- While Japan enjoys "tailwinds" from growth and inflation, it faces new risks. Positive factors include nominal growth and increased tax revenue aiding debt reduction. However, concerns remain regarding rising interest payment burdens due to higher government bond yields and the expansion of social security costs caused by an aging population.

- The IMF analysis provides both "theoretical reinforcement" and a "warning on discipline" for the Takaichi administration’s policies. Alignment: The policy of prioritizing the "Debt-to-GDP ratio" aligns with the IMF's focus on nominal growth. "Strategic Investment" in AI and science overlaps with IMF-recommended productivity measures. Challenges: Given rising interest costs, the IMF demands the rebuilding of "fiscal buffers" for future shocks and recommends a "gradual fiscal adjustment" involving the streamlining of existing expenditures while the output gap is positive.

1. Introduction

In the global economy of 2025, public debt trends have not improved, and conflicts in the Middle East have created new fiscal pressures. G7 countries share challenges such as high debt levels, rising interest burdens, and structural spending increases for aging populations and defense. However, the IMF's Fiscal Monitor released last month reveals that situations and responses vary significantly by country. This report compares the fiscal outlooks for G7 nations presented in that monitor.

2. Overview and Outlook of Key Indicators

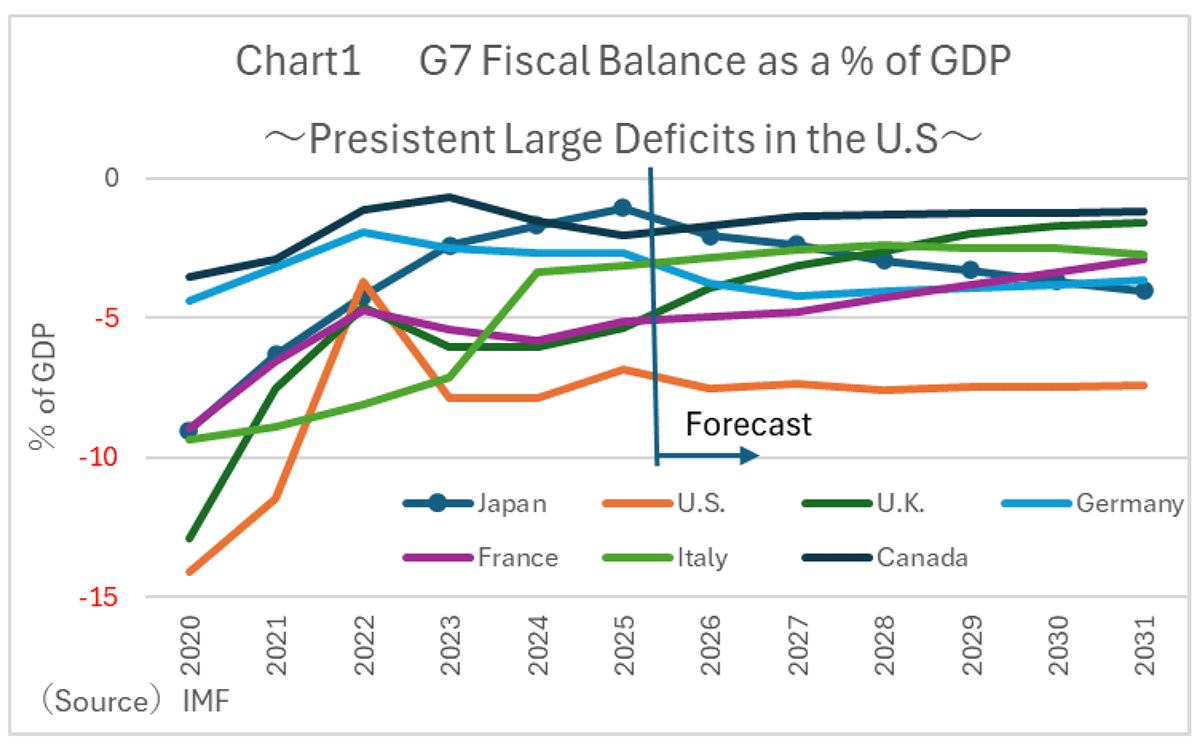

Across advanced economies, the 2025 fiscal deficit remained roughly flat at 2.4% of GDP (excluding the US), but public debt levels remain above pre-pandemic levels.

- United States: The outlook is extremely severe. Despite near full employment, the US carries a massive deficit of 7–8% of GDP with no concrete consolidation plan. Debt is projected to rise from 124% in 2025 to 142% by 2031 (Charts 1 & 2).

- Japan: Debt dynamics are improving, supported by rising inflation and robust tax revenue. The debt ratio is expected to decrease by 10–14 percentage points by 2031.

- Europe: The UK recorded significant improvement, with its deficit shrinking from 12.9% (2020) to 5.4% (2025) due to tax increases and the end of energy subsidies. Germany has shifted from its conservative stance; fiscal rule reforms to fund public investment and defense are expected to push its debt-to-GDP ratio from 63% in 2025 to approximately 74% by 2031.

3. Japan's Current Status and Debt Dynamics

Notably, Japan’s fiscal situation is showing signs of improvement. Higher inflation, steady GDP growth, and a narrowing primary balance deficit are contributing to better debt dynamics. Supported by strong nominal growth, Japan’s debt-to-GDP ratio is projected to drop by about 14 percentage points by 2031.

However, the IMF points to several structural risks:

- Rising Yields: Japanese government bond yields have reached high levels, posing a risk of spillover to other countries.

- Interest Burden: Increased interest payments are beginning to strain the budget.

- Structural Pressure: The expansion of social security spending due to the aging population remains a heavy long-term burden.

4. IMF Policy Recommendations and Implications for the Takaichi Administration

The IMF suggests that Japan must implement measures to balance stable growth with fiscal sustainability:

- Rebuilding Fiscal Buffers: Prioritizing the creation of fiscal room to prepare for future shocks.

- Gradual Fiscal Adjustment: Leveraging the current positive GDP gap and stable inflation to put debt on a definitive downward path.

- Theoretical Alignment: The Takaichi administration’s core goal of "stably lowering the debt-to-GDP ratio" is consistent with the IMF’s analysis of utilizing nominal growth to reduce debt ratios. The focus on "revenue growth through economic growth rather than tax hikes" is supported by this data.

- Strategic Investment: The administration’s focus on "strategic investment to enhance supply capacity" (Sanaenomics) overlaps with the IMF’s view that spending on next-generation technology (AI) and innovation is essential for productivity and long-term growth.

Conclusion: While the IMF report reinforces the logic of growth-oriented fiscal management, it also serves as a warning. With record-high bond yields and rising interest costs, the IMF strongly urges Japan not to miss this "golden opportunity"—where the supply-demand gap is positive—to perform gradual adjustments and rebuild fiscal buffers.

Disclaimer:

This report has been prepared for general information purposes only and is not intended to solicit investment. It is based on information that, at the time of preparation, was deemed credible by Daiichi Life Research Institute, but it accepts no responsibility for its accuracy or completeness. Forecasts are subject to change without notice. In addition, the information provided may not always be consistent with the investment policies, etc. of Daiichi Life or its affiliates.