- Report Index

- Multidimensional Analysis of Japan's Government Debt

- Economic Trends

-

2026.04

Multidimensional Analysis of Japan's Government Debt

~Trends in Debt-to-GDP, Interest-to-GDP, and Debt-to-Equity Ratios~

Toshihiro Nagahama

- Executive Summary

-

- Based on the Berk and van Binsbergen (2026)1 paper, this report re-evaluates the fiscal debate in Japan, which has historically been biased toward primary balances based on the conventional Debt-to-GDP ratio. While Japan’s debt-to-GDP ratio has quadrupled over the past 40 years to over 200%—a level that stands out globally—it has been pointed out that the theoretical justification for using this as the sole criterion is insufficient and somewhat arbitrary.

- Following the recommendations of the aforementioned paper, this evaluation uses three axes: the "Debt-to-GDP ratio," the "Interest-to-GDP ratio" (indicating the burden of interest expenses), and the "Debt-to-Equity Market Capitalization ratio" (as a proxy for national wealth). This multidimensional approach reveals that Japan presents entirely different profiles depending on the metric used:

- Debt Level: While debt remains high, relative low-interest rates have kept the interest burden relative to GDP more suppressed than in other G7 nations.

- Asset Value: The debt ratio compared to equity market capitalization—which reflects growth expectations—is not at the explosive levels seen in the debt-to-GDP ratio; instead, it trends near or below levels seen in countries like Germany.

- Sustainability: The fact that Japan has not defaulted despite a debt-to-GDP ratio exceeding 200% suggests that the other two indicators may more accurately reflect the nation's debt-bearing capacity.

- Moving forward, it is urgent to build a more sophisticated "Japan Model" that includes a "comprehensive definition of national wealth" (including real estate and private capital) and analyses on a "net debt basis" that account for net foreign assets.

Note: The author would like to thank Professor Masazumi Wakatabe of the Faculty of Political Science and Economics at Waseda University for his valuable comments. All remaining errors are the responsibility of the author.

1. Introduction

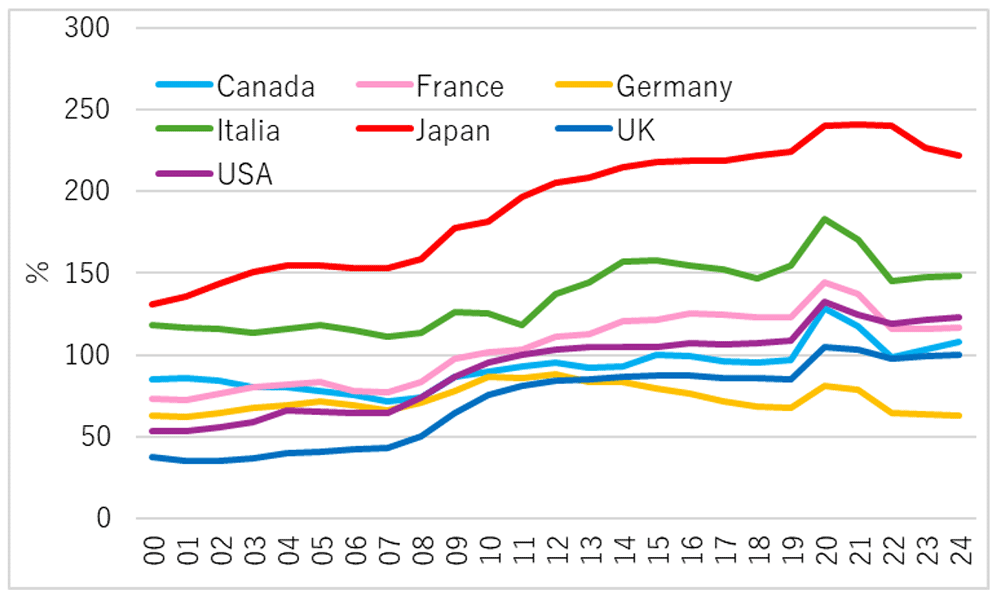

In recent macroeconomic and policy discussions, Japan's government debt has primarily been discussed through the lens of the primary balance based on the Debt-to-GDP ratio. As shown in Figure 1, this ratio has quadrupled over 40 years, reaching a level exceeding 200%, leading to persistent pessimism regarding Japan's fiscal sustainability.

However, as Berk and van Binsbergen (2026) point out, the theoretical justification for treating the debt-to-GDP ratio as the sole determinant is insufficient. This report compares three debt indicators to evaluate Japan’s debt situation from a multidimensional perspective.

Figure 1: Debt-to-GDP Ratio

Source: IMF

2. Significance and Background of the Berk and van Binsbergen Paper

The objective of this paper is to analyze the differences between multiple metrics used to measure government debt ratios and to suggest directions for future research. The authors highlight three representative indicators:

- Debt-to-GDP Ratio: Currently at historical highs.

- Debt-to-Equity Ratio: Shows stability or a downward trend over the last 25 years.

- Interest Burden Ratio: Also shows stability or a downward trend.

The paper argues that relying solely on the debt-to-GDP ratio—without considering fluctuations in stock prices or growth rates—can lead to erroneous judgments regarding long-term fiscal sustainability. Furthermore, it suggests that evaluating optimal government debt levels requires an understanding of the role of debt in the economy, drawing on corporate finance theories like the Modigliani-Miller theorem.

3. The Three Indicators Used for Analysis

This analysis utilizes the following three metrics:

- Debt-to-GDP Ratio: The most common indicator, calculated by dividing debt by annual GDP (See Figure 1).

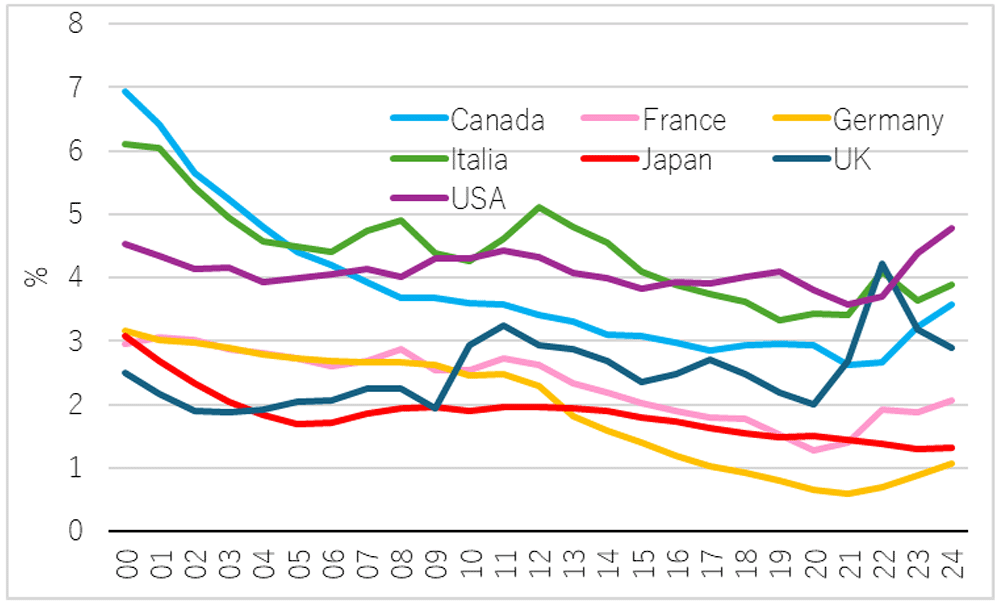

- Interest-to-GDP Ratio: Annual interest expenses divided by GDP (Figure 2).

Figure 2: Interest-to-GDP Ratio

Source: IMF

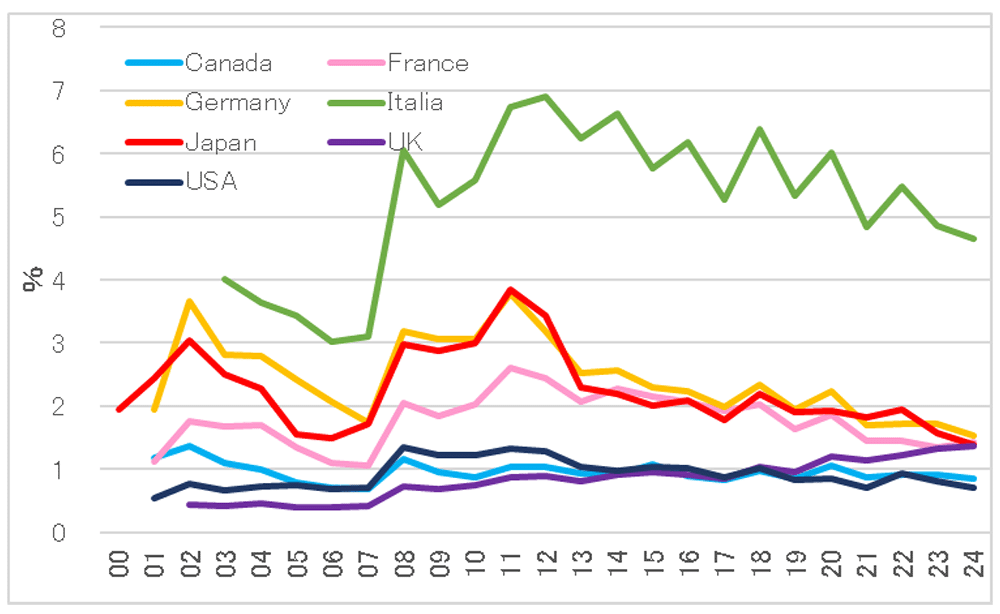

- Debt-to-Equity Market Capitalization Ratio: Debt divided by total equity market capitalization, used as an indirect proxy for the country's economic status (Figure 3).

Figure 3: Debt-to-Equity Market Capitalization Ratio

Source: IMF

4. Comparison of Analytical Results in Japan

International G7 data shows a significant divergence between these indicators in the Japanese context.

- High Debt-to-GDP: While this ratio remains over 200% as of 2024, leading some to view the situation as "critical," other metrics tell a different story.

- Suppressed Interest Burden: Like other G7 nations, Japan’s interest-to-GDP ratio remains suppressed due to historical low-interest rates, despite the increase in total debt.

- Market-Based Evaluation: From a corporate finance perspective, growth expectations are reflected in market capitalization. Japan's debt-to-equity ratio is not at an "explosive" level; it is trending near or below historical averages.

The most critical observation is that Japan shows no signs of default despite its 200%+ debt-to-GDP ratio. This suggests that the interest-to-GDP or debt-to-equity ratios may more accurately reflect Japan's actual debt-paying capacity.

5. Conclusion and Future Outlook

This analysis demonstrates that the pessimistic scenario painted by the "Debt-to-GDP ratio" is not necessarily replicated when using other metrics.

Japanese fiscal sustainability discussions have relied too heavily on a single indicator with an unstable theoretical foundation. Before falling into easy "fiscal crisis" narratives, there is an urgent need to develop indicators based on a robust theoretical framework that merges macroeconomics with corporate finance.

Future refinements to the "Japan Model" could include:

- Expanding the definition of wealth: Including real estate and private capital.

- Net Debt Analysis: Factoring in government-owned assets and net foreign assets.

1Jonathan B. Berk and Jules H. van Binsbergen (2026), 「WHY CARE ABOUT DEBT-TO-GDP?」 NBER Working Paper Series.

Disclaimer:

This report has been prepared for general information purposes only and is not intended to solicit investment. It is based on information that, at the time of preparation, was deemed credible by Daiichi Life Research Institute, but it accepts no responsibility for its accuracy or completeness. Forecasts are subject to change without notice. In addition, the information provided may not always be consistent with the investment policies, etc. of Daiichi Life or its affiliates.