- Report Index

- Japan Economic Outlook (March 2026)

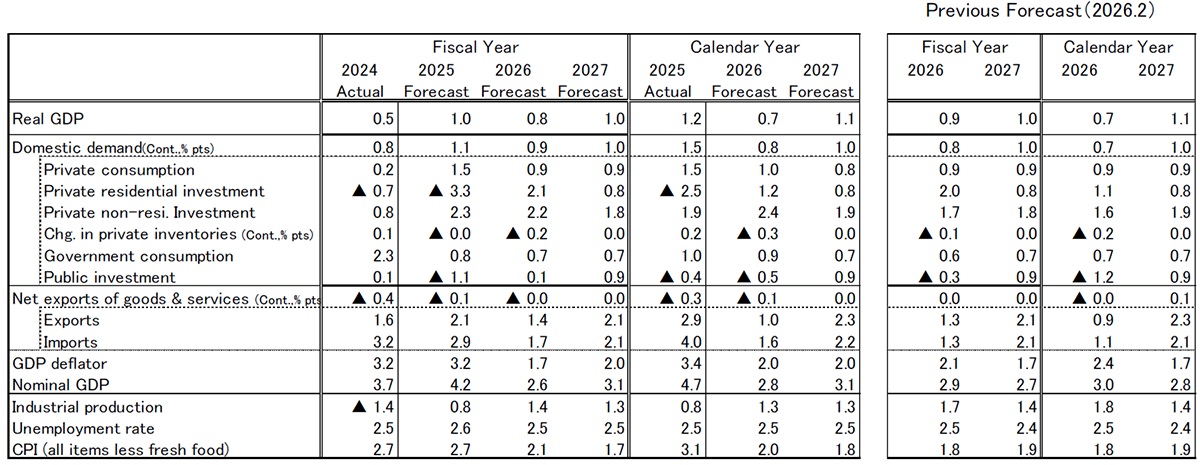

Real GDP growth is projected at +1.0% in FY2025 (February forecast: +0.7%), +0.8% in FY2026 (previously +0.9%), and +1.0% in FY2027 (unchanged at +1.0%). On a calendar-year basis, growth is expected to reach +0.7% in 2026 (unchanged) and +1.1% in 2027 (unchanged). The upward revision to the FY2025 forecast reflects stronger-than-expected growth in the second preliminary estimate for Q4 2025 (October–December). By contrast, the FY2026 forecast has been revised slightly downward to reflect the recent sharp rise in crude oil prices associated with deteriorating conditions in Iran. That said, the forecast does not assume a prolonged escalation of tensions in Iran. While oil prices are expected to remain elevated in the near term, they are assumed to gradually stabilize thereafter. In addition, a possible reduction in the consumption tax rate on food products is not incorporated into the outlook, as details remain unclear at present regarding whether it will be implemented, when it would take effect, and how it would be financed.

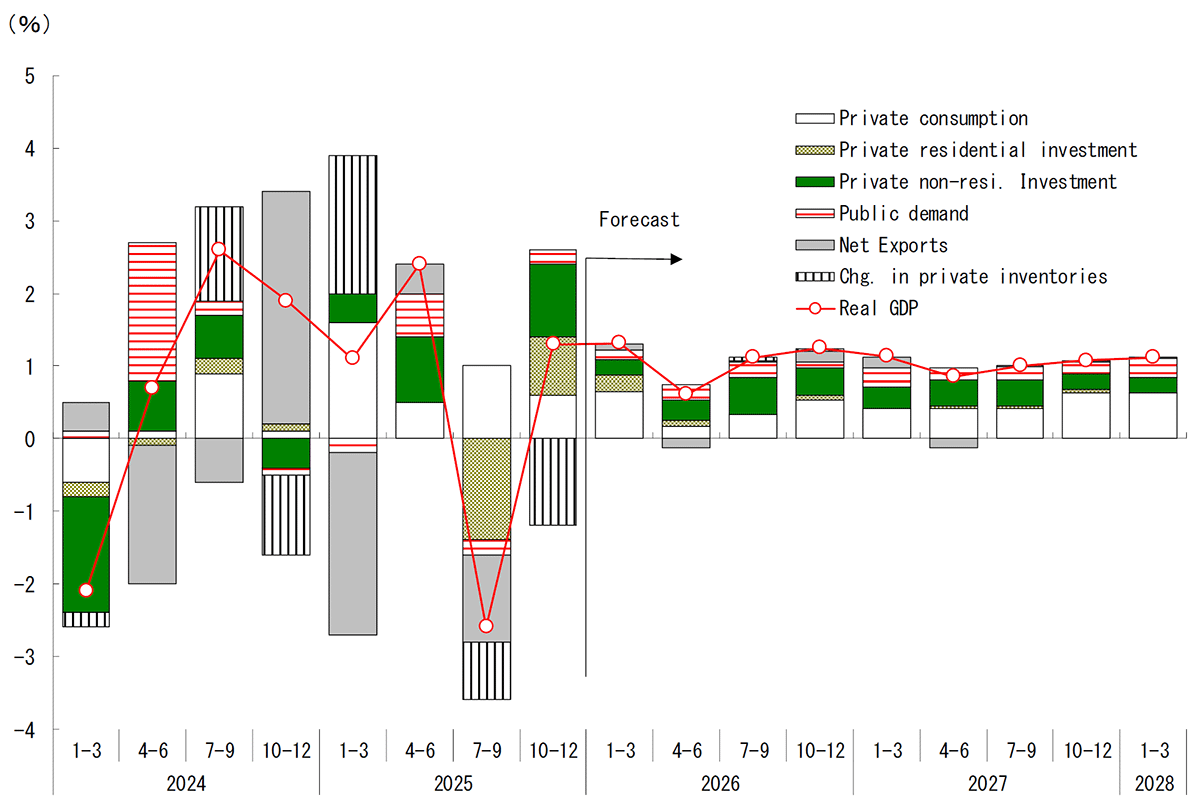

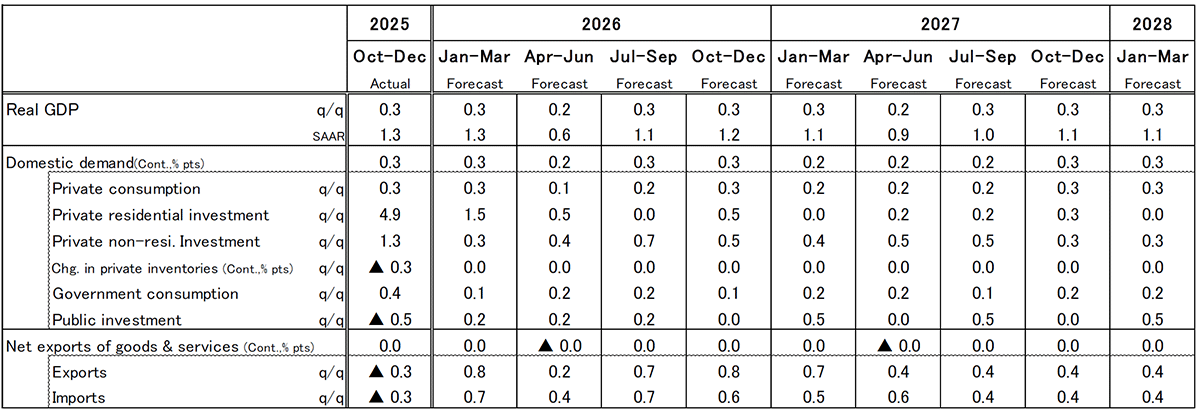

Real GDP growth in Q4 2025 (October–December) was revised upward to +1.3% on a quarter-on-quarter annualized basis, from +0.2% in the first preliminary estimate. The upward revision was relatively large, and the composition of growth also improved from the initial estimate, with stronger contributions from private domestic demand such as business investment and private consumption. The results can therefore be regarded as broadly favorable. Moreover, final demand excluding inventory effects rose +2.6% annualized quarter-on-quarter, indicating stronger underlying momentum than suggested by the headline figure. This more than offset the contraction in Q3 (–1.8% annualized). Taken together, the data suggest that Japan’s economy continues to move along a path of moderate recovery.

For Q1 2026 (January–March), real GDP growth is projected at +1.3% annualized quarter-on-quarter. Exports are expected to recover gradually amid continued resilience in the U.S. economy, while real wages have already begun to turn positive as inflation moderates, providing additional support to economic activity. Until recently, wage growth had failed to keep pace with rising prices, resulting in sustained declines in real wages. However, the slowdown in food price inflation, combined with policy measures such as the abolition of the provisional gasoline tax rate and the resumption of electricity and gas subsidies, is expected to push CPI inflation below +2% year-on-year in Q1, allowing real wages to remain in positive territory. The easing of downward pressure on household income should help underpin private consumption.

The economy is expected to recover gradually in FY2026. Two factors are likely to support Japan’s economy: the continued strength of the U.S. economy and an improvement in real household income. In the United States, the effects of interest rate cuts implemented during 2024–2025 are expected to support real economic activity in 2026 with a lag. In addition, the implementation of the Trump tax cuts will bolster domestic demand, while the negative effects of tariffs are likely to have peaked. Whereas tariff hikes and other policy measures weighed on the U.S. economy in 2025, policy factors in 2026 are expected to support growth. Demand related to generative AI is also projected to remain robust, suggesting that the U.S. economy will likely continue to perform well in 2026. Although the ongoing slowdown in China remains a source of concern, the global economy as a whole is expected to recover, supporting a gradual increase in Japanese exports. The recovery in exports should also lead to improved corporate earnings. Together with structural drivers such as investment in digitalization, labor-saving technologies, and research and development, business investment is likely to act as another engine of economic growth.

Another positive factor is the recovery in real household income. In the 2026 spring wage negotiations, wage increases are projected at 5.45% (Ministry of Health, Labour and Welfare basis; 5.52% in 2025), marking the third consecutive year of wage gains exceeding 5%. Several factors are contributing to this momentum. Labor shortages are becoming increasingly severe, necessitating wage increases to secure workers. At the same time, both labor and management have become more conscious of the prolonged decline in real wages amid historically high inflation, strengthening their commitment to improving real wages in the 2026 negotiations. In addition, the negative effects of the Trump tariffs have so far been smaller than initially expected, and progress in passing on higher costs to prices has helped maintain corporate profits at elevated levels. Against this backdrop, wage-hike momentum remains strong in 2026. As the sharp rise in food prices—which significantly pushed up inflation in FY2025—runs its course, the pace of inflation is expected to moderate, increasing the likelihood that real wages will stabilize in FY2026. Policy measures such as the expansion of tuition-free high school education, the introduction of free school lunches at elementary schools, and the raising of the income threshold that previously discouraged second earners from increasing their working hours are also expected to support household income. As rising prices have eroded households’ real purchasing power and constrained the pace of economic recovery, the anticipated improvement in real income in FY2026 represents welcome news and should contribute to stabilizing private consumption.

The main risk factor is a prolonged surge in crude oil prices. In this forecast, the deterioration in the situation in Iran is assumed to ease relatively soon, limiting the economic impact. However, if tensions were to persist and crude oil prices remain elevated, the resulting increase in energy costs would exert significant upward pressure on inflation and become a major drag on economic activity. Given that Japan relies on imports for nearly all of its energy resources, the impact of higher oil prices would be particularly substantial. If crude oil prices were to remain around $100 per barrel for an extended period, real wages in FY2026 could once again turn negative. As the stabilization of real wages—supported by moderating inflation—is expected to be a key pillar supporting the economy in FY2026, a prolonged rise in oil prices would significantly restrain the pace of economic recovery.

Japan's Economic Outlook (Yearly)

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office, Ministry of Economy, Trade and Industry, Ministry of Internal Affairs and Communications, and Cabinet Office.

Forecast of Real GDP (Quarter-on-Quarter Annualized Rate, Contribution)

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office.

Japan’s Economic Outlook (Quarterly)

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office.

Disclaimer:

This report has been prepared for general information purposes only and is not intended to solicit investment. It is based on information that, at the time of preparation, was deemed credible by Daiichi Life Research Institute, but it accepts no responsibility for its accuracy or completeness. Forecasts are subject to change without notice. In addition, the information provided may not always be consistent with the investment policies, etc. of Daiichi Life or its affiliates.