- Report Index

- Japan Economic Outlook (February 2026)

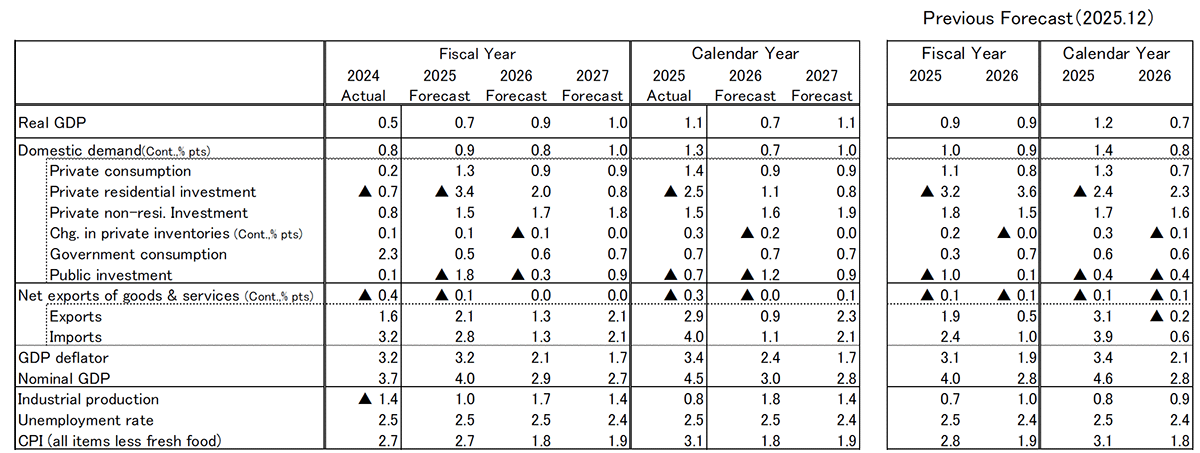

Real GDP growth is projected at +0.7% in FY2025 (December forecast: +0.9%), +0.9% in FY2026 (unchanged), and +1.0% in FY2027. On a calendar-year basis, growth is expected at +0.7% in 2026 and +1.1% in 2027.

The downward revision to FY2025 reflects weaker-than-expected growth in Q4 2025 (October–December) relative to our previous projection. Our overall assessment of the outlook remains unchanged. A gradual recovery is anticipated, supported by a rebound in overseas economies and improving real incomes as inflation moderates.

A potential cut in the consumption tax on food has not been incorporated into the forecast, as key details—including whether it will be implemented, its timing, and its financing—remain unclear.

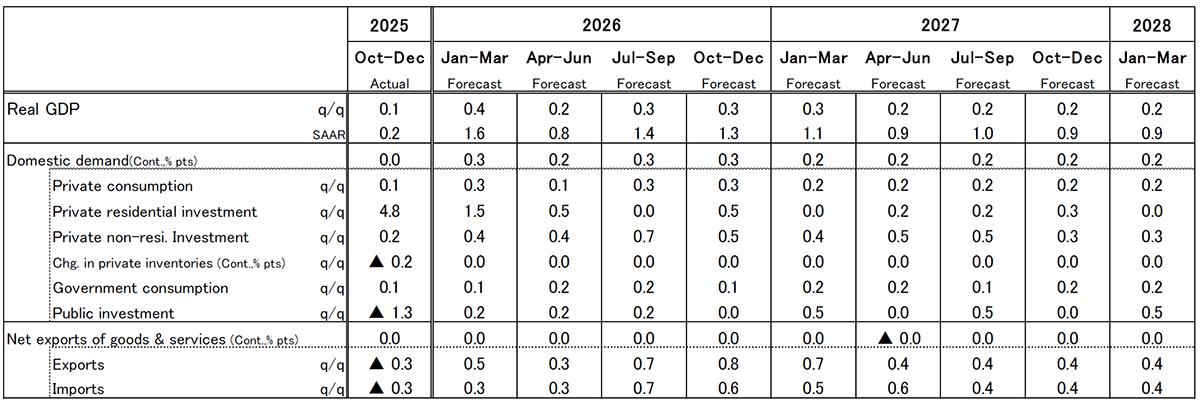

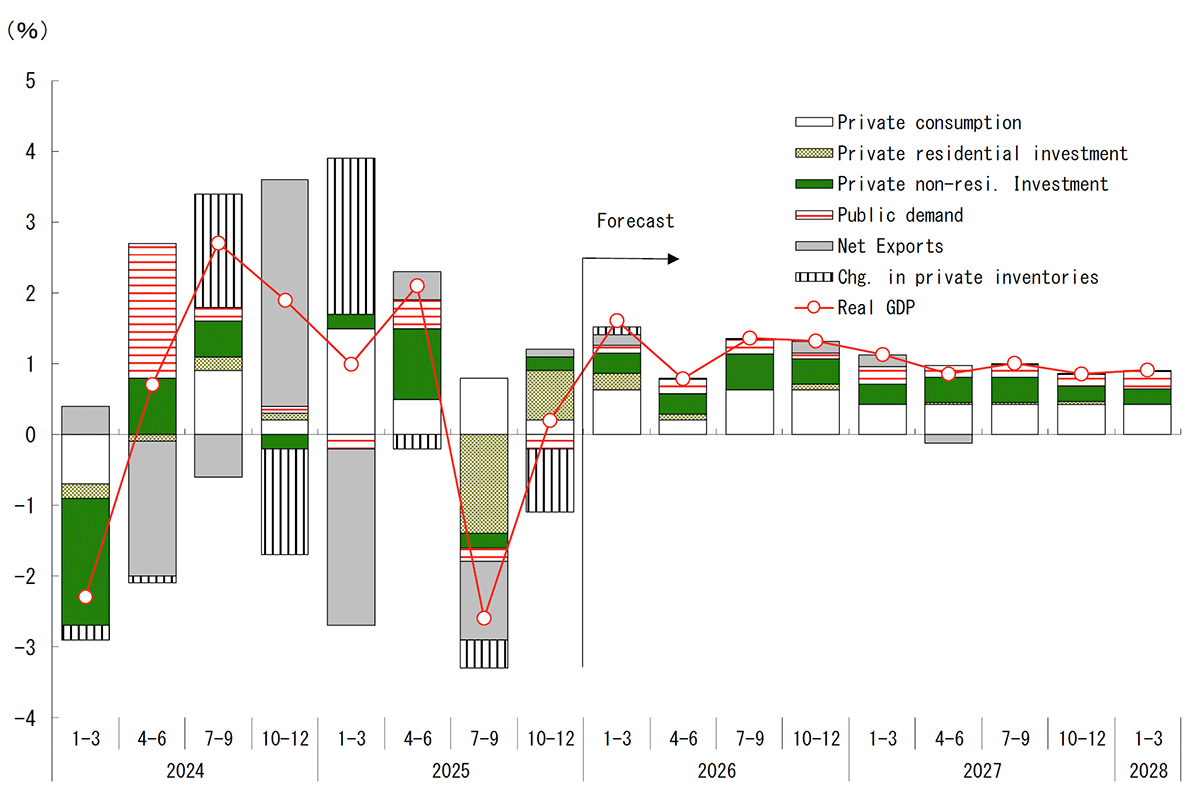

Real GDP growth in Q4 2025 (October–December) turned positive at an annualized +0.2% quarter-on-quarter, following a sharp contraction of –2.6% in Q3. However, the rebound was modest relative to the magnitude of the prior decline. Final demand excluding inventories rose at an annualized +1.1% (Q3: –2.2%), suggesting that underlying conditions were somewhat firmer than the headline figure implies. Nevertheless, Japan’s economy in the second half of 2025 fell short of expectations.

By component, only residential investment—rebounding from a steep prior-quarter decline—made a clear positive contribution. Private consumption, business fixed investment, and exports were broadly flat. Although the recovery phase technically continues, the absence of a clear growth driver has left the economy lacking strong momentum.

For Q1 2026 (January–March), we project annualized growth of +1.6% quarter-on-quarter. A gradual pickup in exports is expected amid continued strength in the U.S. economy, while moderating inflation is likely to allow real wages to bottom out, thereby providing additional support to domestic demand.

Throughout 2025, wage growth lagged inflation, resulting in sustained declines in real wages. However, policy measures—including the abolition of the former provisional gasoline tax rate and the resumption of electricity and gas subsidies—are likely to push CPI inflation below +2% year-on-year in Q1 2026. As a result, real wages are expected to return to positive territory, easing pressure on household incomes and helping to stabilize private consumption.

We expect the economy to continue a gradual recovery in FY2026. Solid U.S. economic performance and an improvement in real household income are expected to underpin growth.

In the United States, interest rate cuts implemented during 2024–25 are likely to support real economic activity in 2026 with a lag. In addition, the implementation of the Trump tax cuts should help underpin domestic demand, while the negative impact of tariffs is expected to have peaked. Whereas policy measures acted as a drag on the U.S. economy in 2025, they are likely to become a tailwind in 2026. Robust demand related to generative AI is also expected to persist, increasing the likelihood of continued U.S. economic strength.

Although the ongoing slowdown in China remains a concern, the global economy as a whole is expected to recover gradually, supporting moderate growth in Japanese exports. The recovery in exports, together with resilient corporate earnings, should encourage business fixed investment. Additional drivers—including digitalization, labor-saving investment, and research and development spending—are also expected to contribute positively to growth.

Another supportive factor is the recovery in real wages. In the 2026 spring wage negotiations, we forecast wage increases of 5.45% (Ministry of Health, Labour and Welfare basis; 5.52% in 2025), marking the third consecutive year of gains in the 5% range.

Momentum for wage increases remains firm amid intensifying labor shortages, growing recognition among both labor and management of the need to restore real wages after a prolonged period of high inflation, and corporate profitability remaining at elevated levels, supported by effective price pass-through and the smaller-than-expected impact of tariffs. As cost-push pressures recede and inflation moderates, real wages in FY2026 are likely to remain modestly positive. Policy measures—including expanded tuition-free high school education, free elementary school lunches, and a higher income threshold for secondary earners—are also expected to support household income.

Given that elevated inflation has eroded households’ purchasing power and constrained the pace of recovery, the anticipated improvement in real income in FY2026 represents a welcome development and should contribute to stabilizing private consumption.

Core CPI (excluding fresh food) is projected to rise +2.7% in FY2025, +1.8% in FY2026, and +1.9% in FY2027. While further food price increases remain likely, the pace is expected to moderate compared with the previous year, partly reflecting base effects from previously high inflation.

In addition to the abolition of the provisional gasoline tax rate, expanded electricity and gas subsidies are likely to push core CPI below +2% year-on-year in Q1 2026. In FY2026, rising service prices will exert upward pressure, but easing cost-push food inflation and policy-driven price reductions—such as expanded tuition-free high school education and free school lunches—are likely to keep core CPI slightly below +2%.

The main risks to the outlook stem from renewed yen depreciation and upside inflation pressures, a deterioration in Japan–China relations, and developments in U.S. equity markets. Although the yen has recently appreciated somewhat from earlier levels, renewed depreciation could encourage firms to accelerate price pass-through. Unlike in the past, companies are now less hesitant to raise prices, and April—the start of the fiscal year—warrants particular attention. If food price deceleration proves slower than expected, real wage gains in FY2026 may fail to materialize.

Beyond the potential decline in inbound demand, disruptions to rare earth supplies represent a more critical risk. While short-term adjustments through inventory drawdowns and alternative sourcing may be feasible, prolonged restrictions on imports from China could significantly disrupt domestic production.

U.S. equity markets remain buoyant on strong expectations for AI-related demand, though concerns about overheating are mounting. A shift in sentiment could trigger a meaningful correction. Given the important role of wealth effects among high-income households in sustaining U.S. economic resilience, close monitoring of equity market developments is warranted.

Japan’s Economic Outlook (Yearly)

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office, Ministry of Economy, Trade and Industry, Ministry of Internal Affairs and Communications.

Japan’s Economic Outlook (Quarterly)

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office.

Forecast of Real GDP

(Quarter-on-Quarter Annualized Rate, Contribution)

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office.

Disclaimer:

This report has been prepared for general information purposes only and is not intended to solicit investment. It is based on information that, at the time of preparation, was deemed credible by Daiichi Life Research Institute, but it accepts no responsibility for its accuracy or completeness. Forecasts are subject to change without notice. In addition, the information provided may not always be consistent with the investment policies, etc. of Daiichi Life or its affiliates.