- Report Index

- Beyond the 'Takaichi Trade':

- Economic Trends

-

2026.01

Beyond the 'Takaichi Trade':

Why Japan's Fiscal Expansion Has Proven More Restrained Than Expected

Takuya Hoshino

- Executive Summary

-

- The Takaichi administration's first budget cycle has revealed that "responsible proactive fiscal policy" is not the unconstrained fiscal expansion many had feared. An analysis of three key fiscal events—the FY2025 supplementary budget, FY2026 tax reform, and FY2026 initial budget—shows that while the supplementary budget displayed expansionary tendencies, subsequent tax reforms and the initial budget were notably restrained. Rising interest rates emerged as a de facto brake, with bond markets exerting a disciplinary influence.

- Key findings include: (1) The general account primary balance is projected to turn positive on an initial budget basis for the first time in 28 years; (2) Combined initial and supplementary budget bond issuance continues its gradual decline (from ¥42.1 trillion in FY2024 to ¥40.3 trillion in FY2025); (3) The ¥7.1 trillion increase in the FY2026 budget is largely mechanical—approximately 70% stems from debt service costs and local allocation tax grants linked to rising rates and tax revenues.

- The upcoming "Basic Policy 2026" (Honebuto) in June will be pivotal, potentially redefining Japan's fiscal consolidation targets. Three major changes are anticipated: a shift from the primary balance target toward multi-year frameworks; elevation of the debt-to-GDP ratio stabilization goal; and possible introduction of a "golden rule" separating growth investments from current expenditures.

- Additional focal points include the launch of Japan's version of DOGE to review tax expenditures and subsidies for resource reallocation, and measures to address the chronic expansion of supplementary budgets. The administration's fiscal stance appears to be converging toward a pragmatic approach emphasizing: (1) sensitivity to interest rate pressures; (2) fiscal policy as growth strategy; and (3) a transition from supplementary budget reliance to initial budget emphasis—focusing on qualitative rather than quantitative fiscal improvement.

We welcome press inquiries and interviews. Please contact us at hoshino@dlri.co.jp.

Introduction: Testing "Responsible Proactive Fiscal Policy"

Since the Takaichi administration's inception, markets and experts have persistently expressed concerns about fiscal discipline loosening under its "responsible proactive fiscal policy" banner. During the LDP presidential election, Prime Minister Takaichi indicated that the primary balance (PB) target had constrained growth investments, openly signaling her intent for aggressive fiscal management. Against this backdrop, the budget formulation at year-end 2025—the first under her administration—attracted considerable attention as a litmus test for the practical implementation of this policy.

Three key fiscal events materialized at year-end: (1) the FY2025 supplementary budget, (2) the FY2026 tax reform outline, and (3) the FY2026 initial budget. In sum, the feared one-sided expansion did not materialize—overall, the expansionary fiscal stance has diminished in scale. While the supplementary budget showed proactive tendencies, the subsequent tax reforms and initial budget were generally moderate. What stood out instead was the significant impact of rising interest rates as a check on fiscal management. A pattern emerged whereby the bond market effectively imposed constraints on fiscal expansion.

This article analyzes these three fiscal events to clarify this point, then examines the key issues for the "Basic Policy 2026" (Honebuto), which will be the focal point of economic policy in 2026. The Basic Policy, formally titled the "Basic Policy on Economic and Fiscal Management and Reform," is decided by the Cabinet around June each year and has been formulated annually since 2001. It outlines the fundamental approach and priority areas for budget formulation, serving as a guideline for subsequent budget requests, budget formulation, and tax reforms. This year's Basic Policy may represent a critical juncture, potentially including revisions to fiscal consolidation targets.

The Supplementary Budget Expansion That Changed Bond Market Sentiment

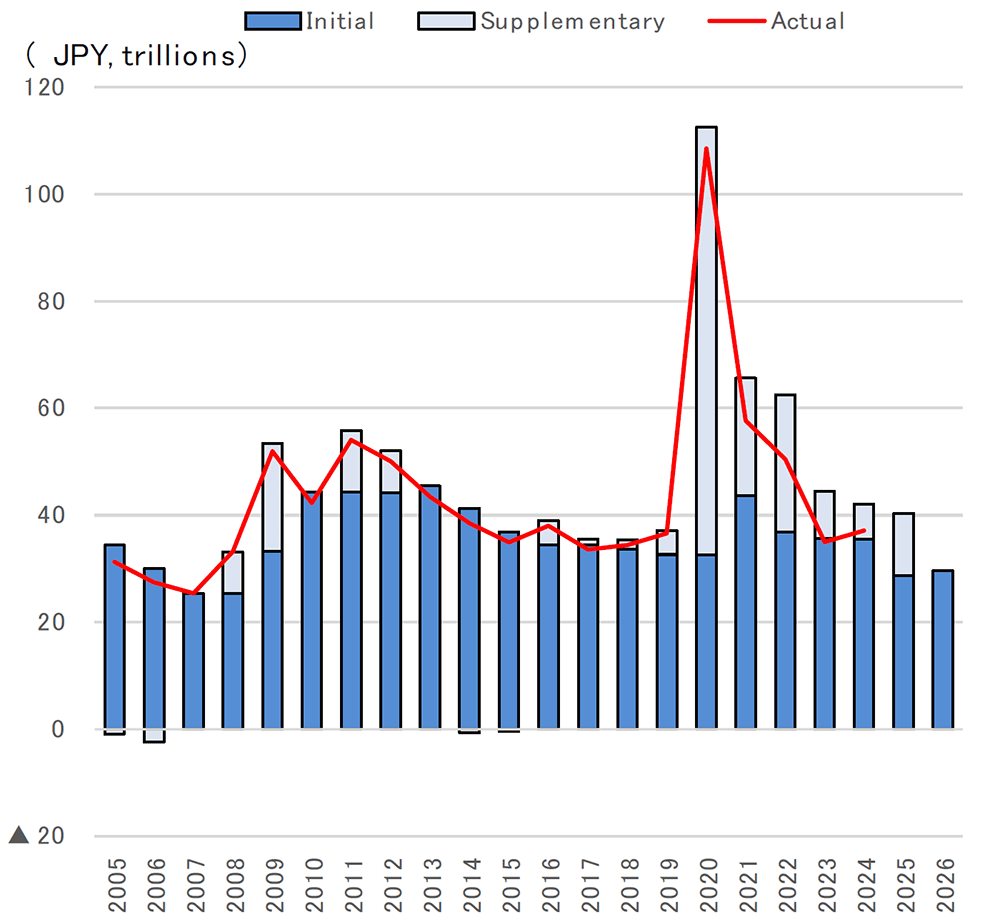

Among the series of budget events, the FY2025 supplementary budget was where expansionary fiscal tendencies were most pronounced. Reports indicate that approximately ¥4 trillion was added to the initial Ministry of Finance draft at Prime Minister Takaichi's behest (the final scale reached ¥18.3 trillion, up from an original ¥14 trillion). New government bond issuance for the FY2025 supplementary budget rose to ¥11.7 trillion from ¥6.7 trillion in the previous year.

The supplementary budget included strategic investments in 17 priority areas emphasized by the Prime Minister, along with additional household support measures. A total of ¥6.4 trillion was allocated to creating and expanding funds for multi-year investments, including the shipbuilding revitalization fund, space development fund, and generic pharmaceutical manufacturing infrastructure fund. Additionally, ¥2.9 trillion was allocated for inflation countermeasures and ¥3.0 trillion for disaster prevention, mitigation, and national resilience. The content emphasized two axes: public-private integrated investment and inflation countermeasures.

The supplementary budget expansion reportedly led by Prime Minister Takaichi was indeed an expansionary fiscal move. However, the government emphasized that total new bond issuance combining initial and supplementary budgets remained below the previous year's level (from ¥42.1 trillion in FY2024 to ¥40.3 trillion in FY2025), demonstrating consideration for fiscal discipline. Nevertheless, despite this consideration, long-term interest rates gained upward momentum from mid-November when the scale expansion was reported.

The government's explanation itself was not unreasonable. In fact, combined initial and supplementary budget bond issuance has maintained a gradual declining trend. Rather than reacting to the increase in bond issuance per se, markets appear to have responded to the budget formulation process itself—specifically, the perception that Prime Minister Takaichi had prominently advocated for proactive fiscal policies and demonstrably influenced budget outcomes.

Tax Reform and Initial Budget Settle on Moderate Content

The intensifying upward pressure on interest rates significantly influenced subsequent tax reform and initial budget formulation. As a result, both settled on content with diminished expansionary fiscal characteristics.

First, regarding tax reform, the minimum taxable income for the long-debated "income wall" issue was set at ¥1.78 million. While this matched the level sought by the Democratic Party for the People (DPP), the final package differs significantly from their original demands. Although the minimum taxable income reached ¥1.78 million, the basic deduction increase through special measures was limited to those earning ¥6.65 million or less annually, and the resident tax basic deduction was excluded from the scope. As a result, the macro-level tax cut scale was significantly reduced from the original proposal—the tax reduction from deduction increases in FY2025 and FY2026 totaled approximately ¥1.8 trillion, a far cry from the nearly ¥8 trillion originally sought by the DPP.

Additionally, deduction amounts will be indexed to consumer prices over the long term. The Democratic Party for the People had sought indexation to the higher minimum wage growth rate, but this also settled on moderate content.

Prioritization among special tax measures also progressed. The wage increase promotion tax system for large enterprises will be abolished at the end of March 2026, and for mid-sized enterprises, requirements will be tightened before abolition at the end of March 2027. The judgment was that wage increases have become established to a certain degree, indicating that incentive tax systems have largely fulfilled their role. Corporate taxation overall is shifting toward increased burdens.

The subsequently cabinet-approved FY2026 initial budget reached a record ¥122.3 trillion in total expenditure. Compared to the FY2025 initial budget, this represents an increase of ¥7.1 trillion, larger than in typical years. However, analyzing the factors behind this increase reveals aspects difficult to attribute to a "proactive fiscal stance." Of the ¥7.1 trillion increase, debt service costs account for ¥3.1 trillion and local allocation tax grants for ¥2.0 trillion—these two items alone comprise approximately 70% of the increase.

Debt service costs increased due to rising interest rates, while local allocation tax reflects a mechanism linked to national tax revenue growth. While increased interest payments are not without concern, these were at least not intentionally expanded by the Takaichi administration.

Regarding the ¥2.0 trillion increase in general expenditure, the breakdown includes natural growth in social security costs due to aging (¥0.6 trillion), inflation-linked increases in medical and nursing care fees (¥0.3 trillion), defense spending increases (¥0.3 trillion), and education subsidization (¥0.4 trillion). Considering that inflation indexation for medical and nursing care fees was already specified in the Basic Policy decided under the Ishiba administration, all these follow past established policies rather than being independently implemented by the Takaichi administration. Inflation indexation for administered prices is a measure also implemented in other countries and is difficult to characterize as expansionary. Independent expansionary fiscal characteristics are virtually absent.

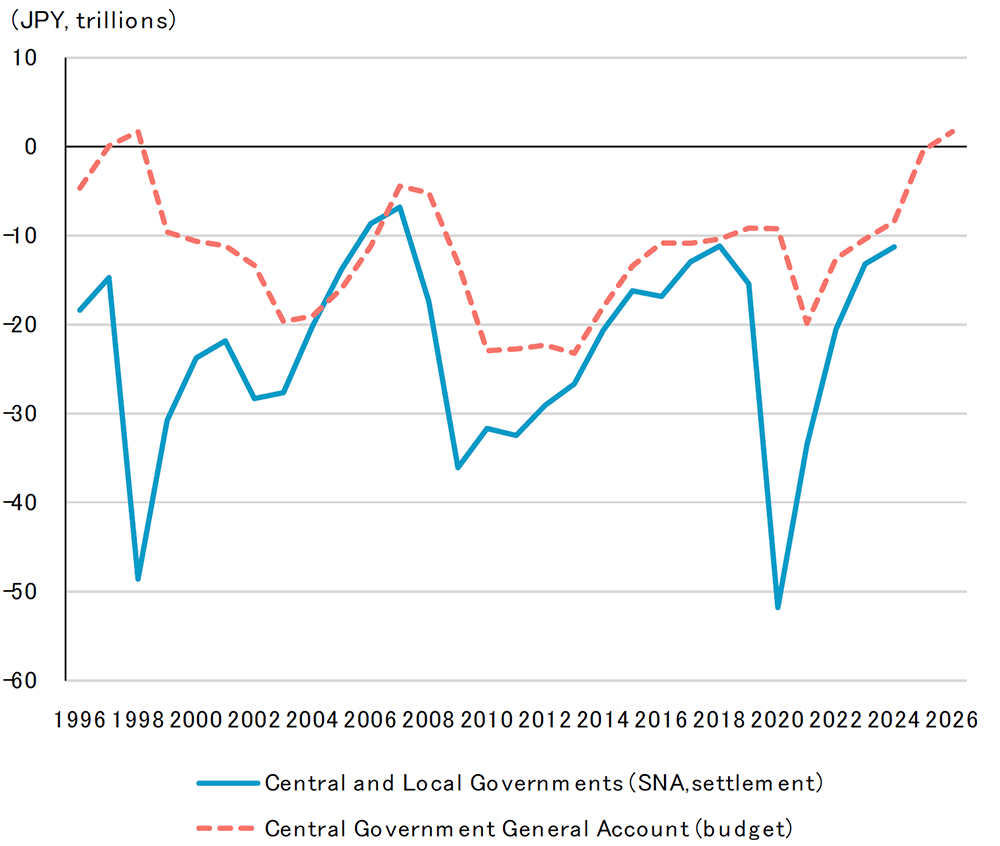

Notably, the general account primary balance is expected to turn positive on an initial budget basis for the first time in 28 years. This reflects robust projected tax revenue of ¥83.7 trillion while expenditure growth was contained. The government's target is based on SNA (System of National Accounts) for combined national and local governments on a settlement basis. Whether this achieves surplus depends on actual budget execution, but reaching a stage where surplus can be projected at the budget phase confirms that fiscal deficits are steadily shrinking.

Figure 1. Primary Balance by Different Measures

Source: MOF, CAO, Dai-Ichi Life Research Institute.

Figure 2. New Government Bond Issuance: Initial, Supplementary, and Actual

Source: MOF, CAO, Dai-Ichi Life Research Institute.

Focus of the 2026 Basic Policy: How Will Fiscal Targets Change?

The central focus of economic and fiscal policy in 2026 is the "Basic Policy 2026" to be formulated around June. The most watched aspect is the review of fiscal consolidation targets. The government has long set "PB surplus" as its target, but the Takaichi administration holds that this target has hindered growth investments. The Basic Policy will discuss the "next stage" of this target.

Three major directions for fiscal target changes are anticipated. First is revision of the PB target itself. Prime Minister Takaichi has advocated "multi-year" targets in the Diet and elsewhere. Changing from the conventional "surplus in a specific single fiscal year" format to something like a cumulative surplus over multiple years would enable more flexible fiscal management accounting for economic fluctuations. Additionally, given rising interest rates, arguments from fiscal hawks may strengthen for emphasizing the fiscal balance including interest payments rather than PB alone. In any case, the positioning of "PB surplus," long the standard criterion, is likely to evolve.

Second is elevation of the debt-to-GDP ratio stabilization target. This approach shifts the focus from single-year flows (the balance) to stock (outstanding debt) relative to GDP, inverting the traditional hierarchy that prioritizes flow targets over stock targets. If nominal growth rates exceed interest rates, the debt ratio can decline even with a small PB deficit, making it easier to reconcile with growth investments. However, achievement assessment becomes more susceptible to economic fluctuations (GDP), and whether this would gain market confidence remains uncertain.

Third is introduction of a "golden rule" approach that treats growth investments separately. Under this concept, balance is maintained for current expenditures while permitting limited government bond issuance for investment expenditures that contribute to future growth. This aligns most closely with the Takaichi administration's philosophy of "smart fiscal expansion," but determining what qualifies as "investment" could introduce arbitrariness. Drawing lines—is defense spending investment or current expenditure? What about education expenditure?—tends to be contentious. While Japan has frameworks distinguishing construction bonds from deficit-financing bonds, eligible items center on physical infrastructure and capital contributions, making it difficult to include intangible assets. This approach may not fully suit current economic structures.

Japan's Version of DOGE Goes Live

Another point of attention is Japan's version of DOGE (Office for Review of Special Tax Measures and Subsidies). The Takaichi administration has established this organization within the Cabinet Secretariat, indicating it will be fully operational from the FY2027 budget. The Basic Policy is expected to present specific operational guidelines and criteria for selecting review targets.

Crucially, this initiative's core purpose is not merely expenditure reduction or fiscal consolidation, but rather the scrutiny of special tax measures and subsidies that have persisted without adequate verification of their effectiveness, with the aim of reallocating resources to areas that genuinely contribute to growth. In other words, it aims to reform the "quality" rather than the "quantity" of fiscal policy.

The particular focus will be on reviewing funds (kikin). Since the COVID-19 pandemic, funds were successively created and expanded as vehicles for economic measures, causing balances to swell. Funds are originally mechanisms enabling flexible multi-year spending beyond single-fiscal-year constraints, but in practice, execution status is often opaque, with many cases where money stagnates and becomes a "hidden budget." The Board of Audit has repeatedly flagged these issues. The current supplementary budget also allocated ¥6.4 trillion to funds, making appropriate management and execution a key future challenge. Attention will focus on how specifically the Basic Policy addresses this.

How to Achieve "From Supplementary to Initial"

The Council on Economic and Fiscal Policy has identified the "routinization and expansion of supplementary budgets" as problematic, proposing a review of role allocation between initial and supplementary budgets. While this issue may seem minor, it is important from the perspective of fiscal management transparency.

Originally, supplementary budgets are intended for emergencies arising mid-fiscal year or for responding to unforeseeable economic fluctuations. However, in recent years, supplementary budgets have become a "second initial budget," compiled routinely every fiscal year.

Structural factors underlie this phenomenon. Under the PB target, the government has emphasized balance in the initial budget, establishing "ceilings (expenditure guidelines)" constraining expenditure growth within the range of aging-related costs. However, this framework inadequately incorporated inflation, functioning as excessive expenditure restraint under inflationary conditions. Consequently, items that should have been in the initial budget were shifted to supplementary budgets, creating a distorted structure of "strict initial" and "lenient supplementary" budgets.

Under this structure, ministries find it easier to secure funding for new measures through supplementary budgets, while fiscal authorities tend to be more lenient toward ostensibly "one-time" supplementary items. Politicians also benefit from being able to "announce economic measures every year." As a result, an equilibrium has formed between "the Ministry of Finance not wanting to increase initial budgets" and "politicians wanting to showcase economic measures."

However, under this system, expenditures that should be increased cannot be addressed in a timely manner, and shifting them to supplementary budgets reduces fiscal policy predictability. What is needed should be in the initial budget, not supplementary—the shift "from supplementary to initial" is being questioned anew. Continuous expenditures should originally be addressed in initial budgets, with supplementary budgets limited to truly urgent spending. If this reform is realized, fiscal management transparency and predictability would be significantly improved.

The Basic Policy will focus on whether constraints will be imposed on supplementary budgets. Fiscal authorities are wary that "from supplementary to initial" might become "supplementary and initial," ultimately expanding total expenditure. Possible constraint approaches include both quantity (scale) and quality (urgency), and depending on their effectiveness, such measures could also affect bond markets.

"Responsible Proactive Fiscal Policy" Toward Qualitative Improvement

As described above, the first budget formulation since the Takaichi administration's inauguration showed strengthened expansionary fiscal characteristics in the supplementary budget, but subsequent tax reform and the initial budget settled on moderate content following rising interest rates. New government bond issuance is also gradually shrinking, and the content cannot be characterized as excessive fiscal expansion.

Fiscal expansion itself generates upward pressure on interest rates by tightening macro supply-demand conditions and raising inflation expectations. This is not an exaggerated concern about fiscal collapse, but strengthening upward pressure on interest rates is not desirable for the administration given the negative impacts on private capital investment and government interest payments. Bond markets are expected to continue serving as a restraint against fiscal scale expansion.

Considering the above, the Takaichi administration's "responsible proactive fiscal policy" is not the unconstrained fiscal expansion that has been feared, but rather appears to be settling into a pragmatic line pursuing qualitative fiscal improvement while being mindful of the interest rate environment. Specifically, this approach appears to be converging on three elements: (1) consideration for upward pressure on interest rates; (2) utilization of fiscal policy as growth strategy; and (3) a transition from supplementary budget reliance to initial budget emphasis.

This year's Basic Policy will provide an opportunity to define the specific content of "responsibility" and "proactive" in "responsible proactive fiscal policy." How will fiscal consolidation targets be redesigned? What and how much will Japan's DOGE review? How will supplementary budgets be disciplined? The answers to these questions will illuminate the essence of the Takaichi administration's economic policy and are likely to influence markets as well.

Disclaimer:

This report has been prepared for general information purposes only and is not intended to solicit investment. It is based on information that, at the time of preparation, was deemed credible by Daiichi Life Research Institute, but it accepts no responsibility for its accuracy or completeness. Forecasts are subject to change without notice. In addition, the information provided may not always be consistent with the investment policies, etc. of Daiichi Life or its affiliates.