- Report Index

- Japan Economic Outlook (December 2025)

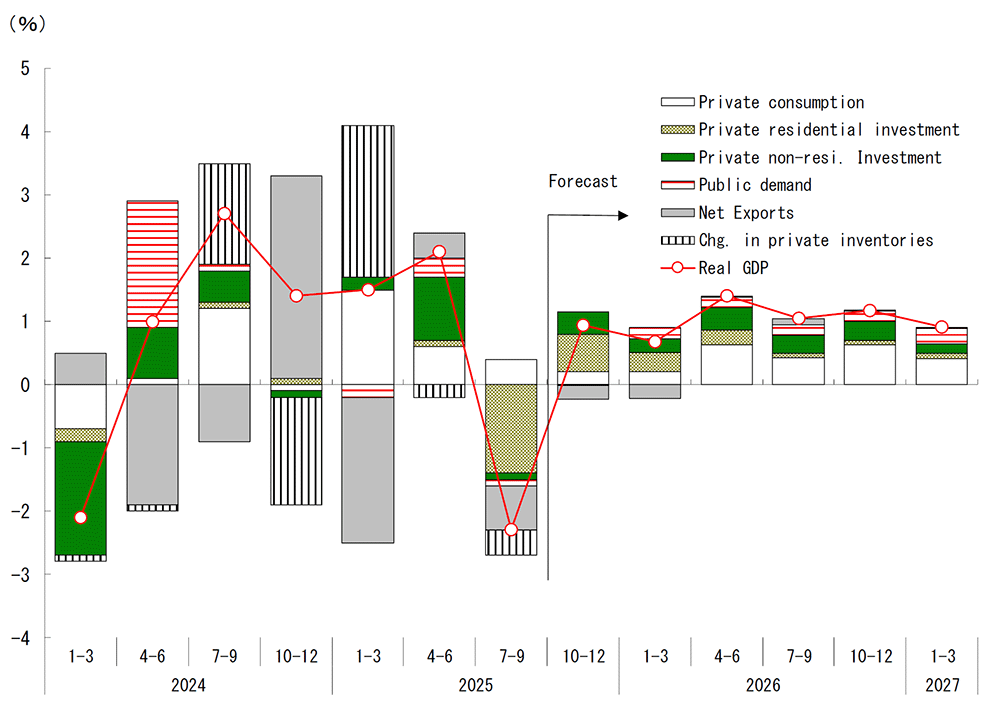

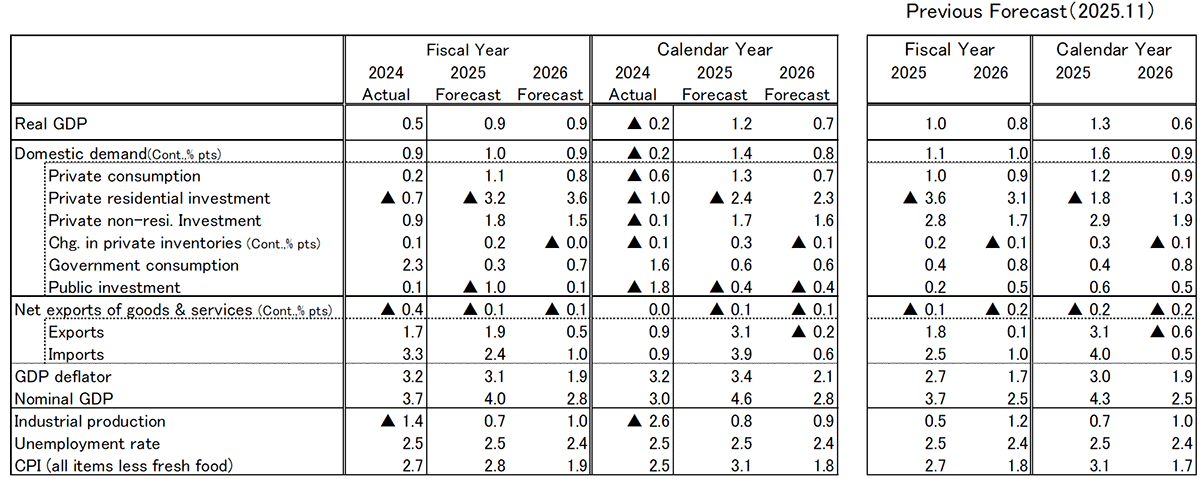

Real GDP growth is projected at +0.9% for FY2025 (November 2025 forecast: +1.0%) and +0.9% for FY2026 (previously +0.8%). On a calendar-year basis, growth is projected at +1.2% in 2025 (previously +1.3%) and +0.7% in 2026 (previously +0.6%). The slight downward revision for FY2025 mainly reflects the weaker second preliminary estimate for Q3; however, our overall forward-looking assessment remains broadly unchanged.

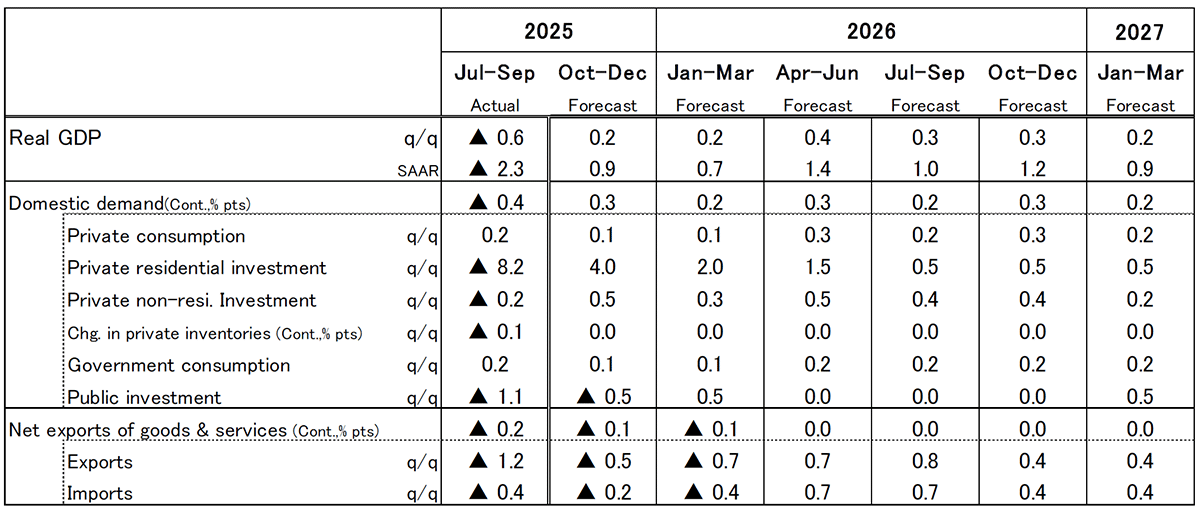

Japan’s real GDP growth in Q3 FY2025 (July–September) recorded an annualized quarter-on-quarter decline of –2.3%, marking negative growth. The contraction was driven largely by a sharp plunge in residential investment, which fell in reaction to front-loaded demand ahead of regulatory revisions, while exports also declined. The drop in residential investment is likely to be temporary, and the decline in exports partly reflects a payback following strong gains in Q2. Therefore, the weakness in Q3 does not warrant undue pessimism. Averaging recent positive quarters still indicates an upward trend in economic activity. Despite tariff hikes in the United States, the sharp stall in Japan’s exports that had initially been feared has been avoided, and no movements directly pointing to a broader loss of economic momentum are evident at present.

That said, uncertainties surrounding the export outlook persist. Although the U.S. economy remains resilient, it is showing signs of gradual deceleration. As tariff pass-through continues and labor market conditions soften, downward pressure on personal consumption, —particularly among lower-income households,—is expected to increase. GDP growth in Q4 is projected to return to positive territory, supported by a recovery in residential investment and rising capital expenditure, but subdued exports will prevent the economy from fully offsetting the Q3 downturn. In the absence of a strong growth driver, Japan’s economy is expected to achieve only a modest recovery in the second half of FY2025.

In FY2026, economic activity is expected to recover gradually. Two key factors—the stabilization of the U.S. economy and the bottoming out of real wages—will support Japan’s recovery. In the United States, while the negative effects of tariff hikes will persist, the impact of interest rate cuts implemented in 2024–25 will increasingly support the real economy in 2026 with a lag. In addition, the implementation of the Trump tax cuts will help underpin domestic demand. Although the tariff shock will continue to weigh on lower-income households, the U.S. economy is expected to move toward stabilization. Japanese exports to the United States are likewise projected to gradually bottom out. As the deterioration in corporate earnings comes to a halt, firms are expected to resume more forward-looking investment behavior.

Another positive factor is the stabilization of real wages. Wage negotiations in spring 2026 are expected to deliver average wage increases of 5.20% (Ministry of Health, Labor and Welfare basis), marking the third consecutive year of wage growth in the 5% range. Contributing factors include: (1) intensifying labor shortages, (2) persistent historically high inflation and the need to offset declines in real wages, and (3) strong corporate profits. As cost-push pressures ease and inflation moderates, real wages are expected to move out of negative territory, helping stabilize private consumption.

Major risk factors include (1) persistent yen depreciation and upside risks to inflation, (2) deterioration in Japan–China relations, and (3) developments in the U.S. stock market. Regarding (1), while inflation is expected to decelerate, further yen depreciation could reignite firms’ willingness to raise prices, keeping inflation elevated and potentially restraining domestic demand through renewed downward pressure on real wages. Regarding (2), prolonged self-restraint on travel from China to Japan would dampen inbound demand, and further escalation—such as boycotts of Japanese products or reduced trade with Japanese firms—could amplify the negative impact. Regarding (3), U.S. equity markets have remained strong on the back of robust expectations for AI-related demand, but concerns about overheating are rising. A decline in such expectations could trigger market adjustments. Given that wealth effects among high-income households have played a significant role in supporting U.S. economic resilience, stock market trends warrant careful monitoring.

Forecast of Real GDP

(Quarter-on-Quarter Annualized Rate, Contribution)

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office.

Japan's Economic Outlook (Yearly)

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office, Ministry of Economy, Trade and Industry, Ministry of Internal Affairs and Communications.

Japan's Economic Outlook (Quarterly)

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office.

Disclaimer:

This report has been prepared for general information purposes only and is not intended to solicit investment. It is based on information that, at the time of preparation, was deemed credible by Daiichi Life Research Institute, but it accepts no responsibility for its accuracy or completeness. Forecasts are subject to change without notice. In addition, the information provided may not always be consistent with the investment policies, etc. of Daiichi Life or its affiliates.