- Report Index

- Japan Economic Outlook (June 2025)

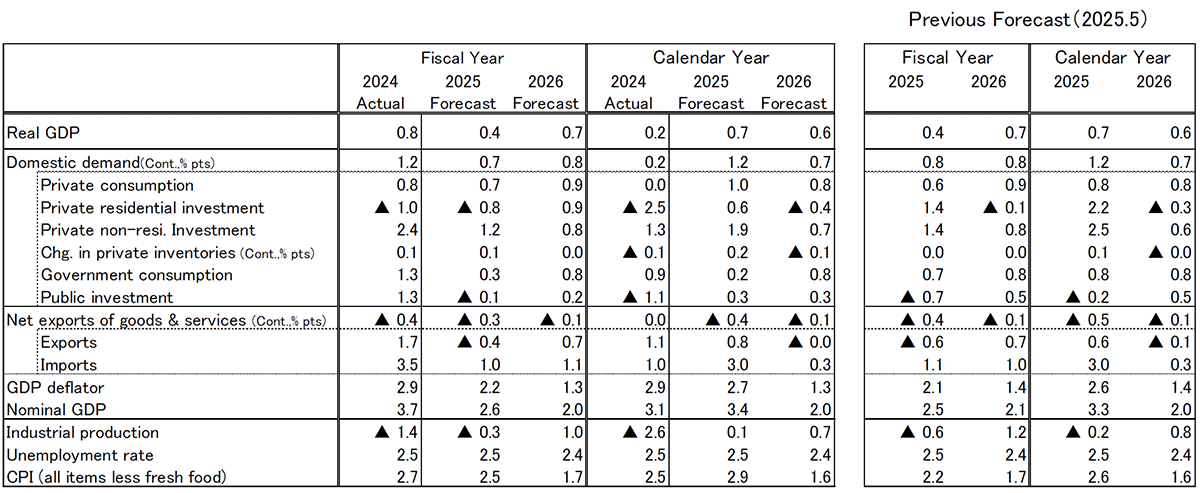

We expect the Japanese economy to grow by +0.4% in FY2025 and +0.7% in FY2026. On a calendar-year basis, real GDP growth is projected at +0.7% in 2025 and +0.6% in 2026. The economic outlook remains unchanged from the projections made in May.

Our assumptions regarding U.S. tariffs on Japan are as follows: reciprocal tariffs are set at 10%, while item-specific tariffs—such as those on automobiles—are set at 25%. We assume that, as a result of future negotiations, the additional reciprocal tariffs will be withdrawn. However, since automobile tariffs are a particular priority for Japan, it is considered unlikely that these will be lowered, and item-specific tariffs are therefore assumed to remain at 25%.

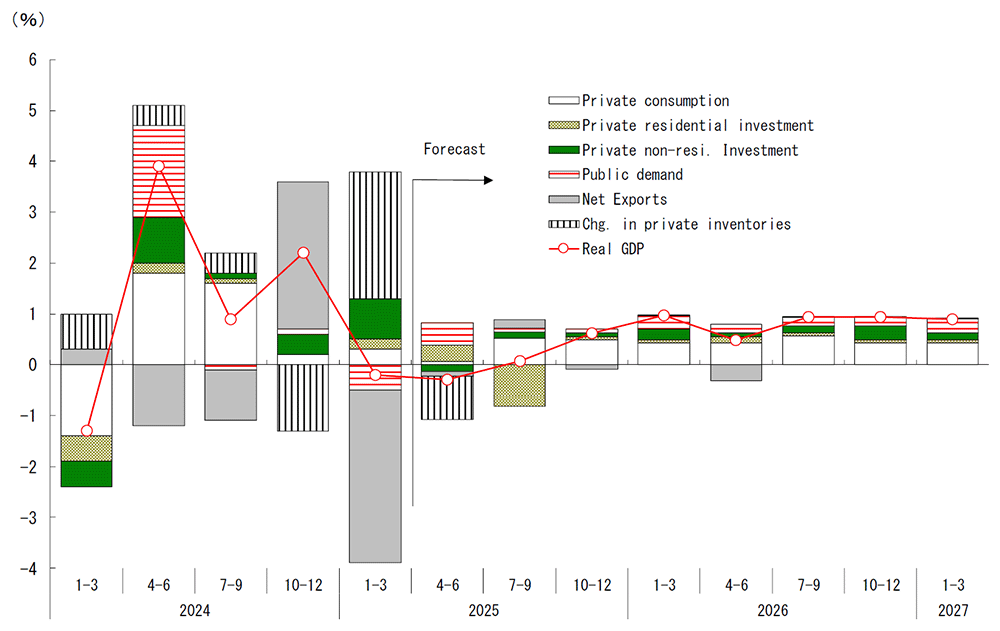

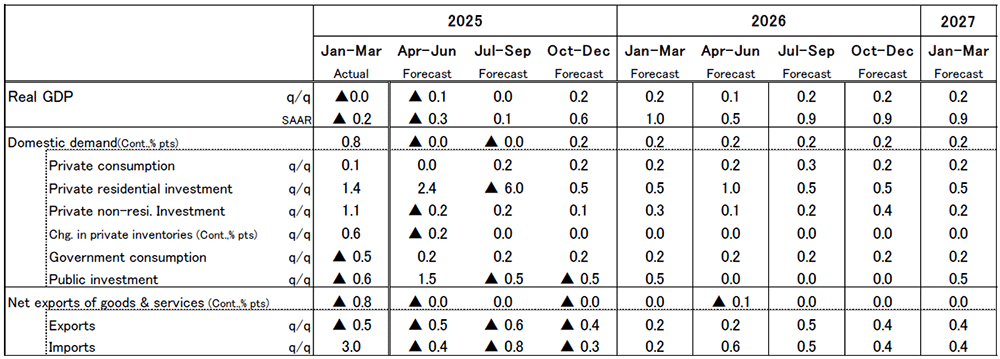

The real GDP growth rate for Q1 2025 declined by −0.2% quarter-on-quarter on an annualized basis, marking the first negative growth in four quarters. In addition to weaker exports, personal consumption remained almost flat for the second consecutive quarter, highlighting a lack of momentum in both domestic and external demand. This indicates that Japan’s economy was already lacking a growth driver, even before the full implementation of the Trump tariffs.

In 2Q 2025, the negative impact of the Trump tariffs is expected to become apparent, and the economy is expected to experience two consecutive quarters of negative growth. Although the additional reciprocal tariffs have been temporarily suspended, the basic tariff rate of 10% remains in place, and item-specific tariffs—such as the 25% rate on automobiles—are being maintained. In addition to the likely decline in exports to the U.S., particularly automobiles, exports to countries other than the United States are also expected to remain weak in light of the anticipated slowdown in the global economy. Furthermore, with the rapid and frequent changes in the tariff environment, uncertainty about the outlook has increased significantly, which is likely to result in restrained capital investment both domestically and overseas. In addition, real wages are expected to continue declining in 2Q, mainly due to rising prices, and consumer sentiment is deteriorating. As a result, personal consumption is likely to remain subdued following the stagnation observed in 1Q.

For FY2025, we forecast real GDP growth at +0.4%, and for CY2025 at +0.7%. However, excluding the statistical carryover effect, growth for FY2025 is expected to be just +0.1%, and for CY2025, −0.1%, meaning both are likely to be essentially flat. Owing to the impact of Trump’s tariffs, the Japanese economy is expected to stagnate and remain below its potential growth rate in 2025. While a sharp recession is not our main scenario, a downturn cannot be ruled out depending on the extent of downward pressure from the tariff situation.

Amid pronounced downward pressure on the economy, one of the few supporting factors is the anticipated deceleration of inflation. While inflation will remain high in the near term, the upward pressure on costs is expected to gradually lighten due to falling crude oil prices and a stabilization of the yen. Government measures to mitigate rising prices should also help curb inflation. As prices moderate, real wages are projected to turn positive from autumn 2025 onwards. Consequently, personal consumption is expected to increase moderately, and we anticipate that the Japanese economy will narrowly avoid slipping into recession.

The economy is expected to recover moderately in FY2026. In the United States, the Federal Reserve is expected to resume interest rate cuts in the second half of 2025 to counter the economic slowdown and a weakening labor market, which will, with a lag, help support growth in 2026. Tax cuts should also provide a boost to the U.S. economy. As U.S. economic conditions stabilize, Japanese exports are expected to rebound, helping to halt the deterioration in corporate earnings. For the 2026 spring wage negotiations, wage growth is expected to slow substantially compared with 2025, reflecting weaker earnings in FY2025 and slower inflation. However, structural factors such as persistent labor shortages are likely to result in some degree of wage growth. With inflation projected to remain below +2%, real wages are expected to maintain a moderate upward trajectory.

Forecast of Real GDP (Quarter-on-Quarter Annualized Rate, Contribution)

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office

Japan's Economic Outlook (Yearly)

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office, Ministry of Economy, Trade and Industry, Ministry of Internal Affairs and

Communications.

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office, Ministry of Economy, Trade and Industry, Ministry of Internal Affairs and

Communications.

Japan's Economic Outlook (Quarterly)

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office

Original in Japanese:

https://www.dlri.co.jp/report/macro/465711.html

Disclaimer:

This report has been prepared for general information purposes only and is not intended to solicit investment. It is based on information that, at the time of preparation, was deemed credible by Dai-ichi Life Research Institute, but it accepts no responsibility for its accuracy or completeness. Forecasts are subject to change without notice. In addition, the information provided may not always be consistent with the investment policies, etc. of Dai-ichi Life or its affiliates.