- Report Index

- Japan Economic Outlook (February 2025)

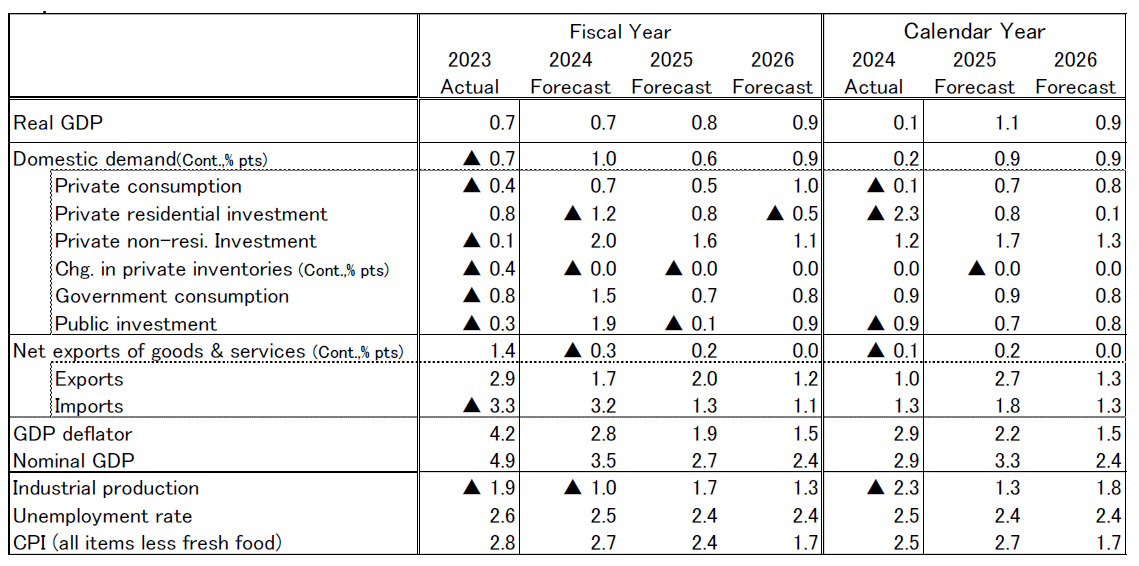

We expect the Japanese economy to grow at +0.7% year-on-year (YoY) in FY2024, +0.8% in FY2025, and +0.9% in FY2026. On a calendar-year basis, real GDP growth is projected to be +1.1% in 2025 and +0.9% in 2026.

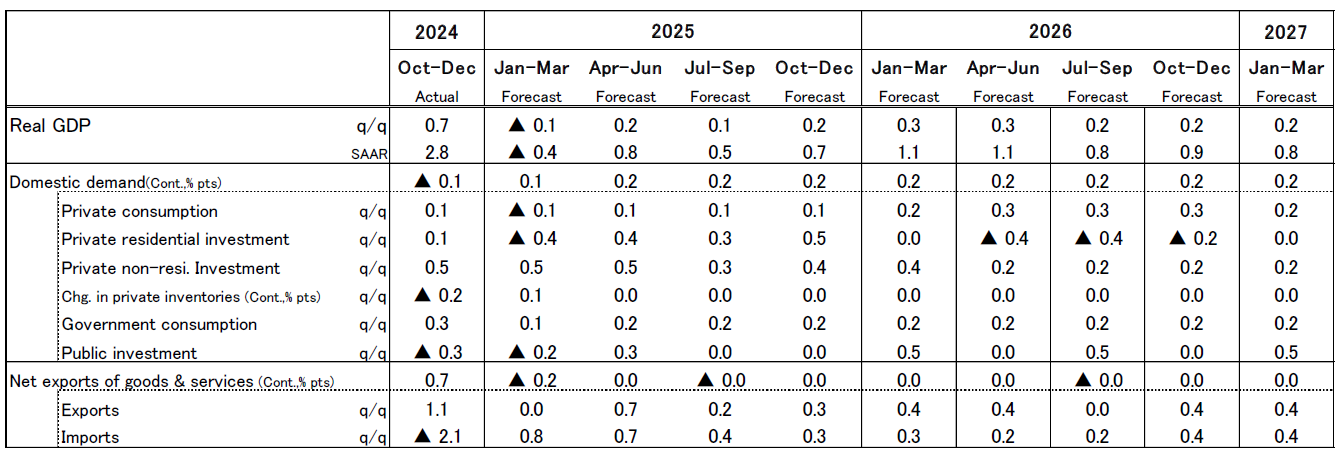

The real GDP growth rate for Q4 2024 showed a high growth of +2.8% on an annualized quarter-on-quarter basis. However, strong GDP results were largely driven by a decrease in imports, while domestic demand, including personal consumption, has stalled. Therefore, these figures should be interpreted with caution. Although the headline figures appear strong, the economy remains in a modest recovery.

This high growth is not sustainable, and real GDP is expected to turn to slight negative growth in 1Q 2025. A major concern is the stagnation of personal consumption due to rising prices. Food prices have been reaccelerating, leading to a prolonged period of high inflation. Although real wages turned positive in 4Q 2024 due to increased winter bonuses, they are likely to turn negative again in 1Q 2025 as the bonus effect fades. The rise in food prices, which are closely related to daily life, is also a concern due to its significant adverse impact on consumer sentiment. Furthermore, with a sense of stagnation remaining in overseas economies, export growth will remain modest, and a rebound in imports is expected. Therefore, contrary to Q4 2024, external demand will likely act as a drag on the growth rate.

Even in Q2 2025 and beyond, rising prices would continue to suppress household purchasing power. We forecast the wage increase rate in the 2025 spring wage negotiations to be 5.3%, with base pay increases at 3.5%. Factors such as a strong sense of labor shortage, consideration for high prices, and solid corporate performance suggest that high wage increases, nearly on par with 2024 (5.33%), are likely to be achieved in the 2025 spring wage negotiations. However, this may still not be enough for wage growth to clearly exceed the rate of price increases. The timing for real wages to turn stably positive is likely to be delayed until the end of 2025, when the rate of price increases is expected to slow down. As a result, the degree of recovery in consumption would be restrained and will only see a slight increase.

Another concern is the potential for President Trump's economic policies to weigh down the global economy. While the positive effects expected from tax cuts are mainly projected for 2026 and beyond, the negative impacts of tariff hikes and retaliatory measures are likely to outweigh them in 2025. The adverse effects on the Chinese economy are particularly significant, which will exert downward pressure on exports from Japan. Furthermore, the reduced predictability of policies has increased uncertainty about the future, which could lead to companies worldwide holding back on investments, thereby depressing Japan's capital goods exports, which account for a large share of its exports. While the Japanese economy is likely to recover moderately in 2025, it is not expected to gain significant momentum due to the lack of strong drivers in both domestic and external demand.

The sense of economic recovery will likely strengthen gradually in 2026. While real wages are expected to remain near zero in 2025 due to persistently high inflation rates, the increase in real wages is likely to expand moderately in 2026 as cost-push inflationary pressures weaken. This situation is expected to lead to a gradual increase in personal consumption. As for business fixed investment, in addition to the recovery in the manufacturing sector, there will be upward pressure from research and development (R&D) investment, decarbonization-related investment, and digital and labor-saving investment, leading to a continued recovery. With the downward pressure on domestic demand weakening due to the slowdown in inflation, the economy is likely to improve moderately.

We forecast that core CPI will reach +2.7% for FY2024, +2.4% for FY2025, and +1.7% for FY2026. Core CPI is expected to remain high, at +2.5-2.9% year-on-year until the fall of 2025, due to the lingering impact of rising import costs. This will likely put downward pressure on personal consumption through reduced real purchasing power. However, the cost-push pressure from rising import prices is expected to gradually weaken. While the increased labor costs would lead to price pass-throughs, putting upward pressure on service prices, the growth in the prices of goods is anticipated to slow. As a result, core CPI is expected to gradually decelerate. We predict that core CPI will fall below +2% year-on-year in 2026.

Japan's Economic Outlook (Yearly)

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office, Ministry of Economy, Trade and Industry, Ministry of Internal Affairs and Communications

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office, Ministry of Economy, Trade and Industry, Ministry of Internal Affairs and Communications

Japan's Economic Outlook (Quarterly)

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office

Forecast of Real GDP (Quarter-on-Quarter Annualized Rate, Contribution)

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office

Note: Forecasts are by the Dai-ichi Life Research Institute.

Source: Cabinet Office

Original in Japanese:

https://www.dlri.co.jp/report/macro/417773.html

Disclaimer:

This report has been prepared for general information purposes only and is not intended to solicit investment. It is based on information that, at the time of preparation, was deemed credible by Daiichi Life Research Institute, but it accepts no responsibility for its accuracy or completeness. Forecasts are subject to change without notice. In addition, the information provided may not always be consistent with the investment policies, etc. of Daiichi Life or its affiliates.